Singapore’s inflation may have eased slightly in November 2022, but the Monetary Authority of Singapore (MAS) warned of prolonged pain likely to linger. Risk factors pile up to the nation’s financial vulnerability in the corporate, banking, and housing sectors.

MAS stated, “Amid weakening external demand, the Singapore economy is projected to slow to a below-trend pace in 2023.” It added that “Inflation is expected to remain elevated, underpinned by a strong labor market and continued pass-through from high imported inflation.”

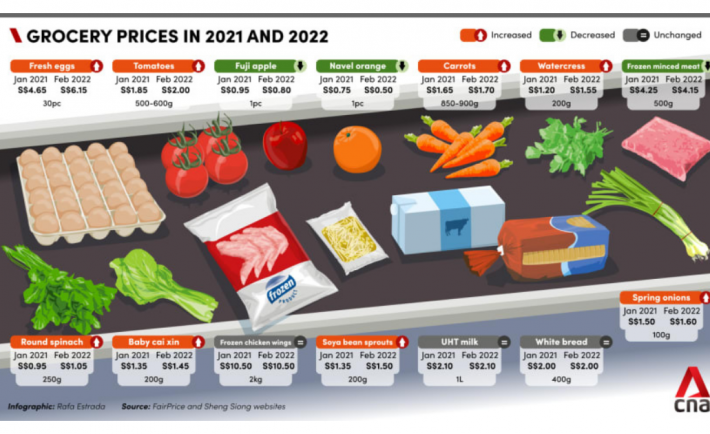

In 2022, the following items were heavily affected by inflation.

#1: GAS AND CAR REPAIRS

Fuel costs skyrocketed in 2022. It saw huge increases in the months of February, March, May, June, October, and November. Moreover, its increased fuel costs spilled over to January 2023. This high fuel costs were driven by the rising global oil and gas prices that were exacerbated by the war in Ukraine. Apart from fuel prices, repair costs definitely took a toll since early 2022.

#2: DELIVERY FEES

Delivery costs increased many companies and restaurants, hammered by inflation and higher fuel rates, passed those costs to consumers. Do you need to cut the costs of online delivery to your budget this 2023?

#3: CLEANING SUPPLIES

The pandemic led us to stay inside our homes more. With the increased demand and effects of inflation, household items became more expensive. Prices of garbage bags, aluminum foil, batteries, and cleaning supplies rose.

Image Credits: pixabay.com

Despite the price hikes, 2022 also saw some unexpected price drops. For instance, television prices sank globally in hopes of lightening their inventory. Major appliances also decreased in price. Used cars also saw a drop in prices. Apart from these observations, clothing retailers have also enticed the consumers with their continuous promotions.

Not to mention, households in Singapore can welcome the new year with lower electricity bills. The tariff for the first quarter of 2023 will decrease by 2.7 per cent. From January 1 to March 31, the electricity tariff before GST will drop from 29.74 cents to 28.95 cents per kilowatt-hour (kWh), said SP Group. This will take effect even as the new goods and services tax (GST) of 8 per cent kicks in.

You may have noticed prices going up for the everyday items you buy. This is because we are now experiencing inflation.

For folks who have been following the news, you would have come across the revelation that core inflation in Singapore has reached its highest level in more than 13 years in May 2022, driven mostly by increased food and utility prices. While some people may be struggling to get by, there are ways to thrive during times of inflation; you just need to know what they are.

In this post, we will share with you tips on how to thrive during times of inflation.

What is inflation?

Inflation is an economic term that refers to rising prices of goods and services in a country. This can be caused by a variety of reasons, such as an increase in the money supply or an increase or decrease in the value of the currency. If you’re feeling the effects of inflation, don’t worry – you’re not alone. Keep reading for tips on how to thrive, not just survive, during these challenging times.

How can you thrive during inflation?

There are a few key ways to thrive during inflation.

Get the best value for your money. Compare prices before you buy and avoid purchasing things on impulse. If you can’t afford something, wait until you can.

Use your money in the most efficient way possible. Make a budget and stick to it, even if it means making some sacrifices. Try to save money wherever you can, and invest in things that will hold their value over time, like gold.

Diversify your income. If all of your eggs are in one basket, you’re going to be in trouble if that basket starts to wobble. Spread your money out into different investments, and always have a backup plan in case of emergencies.

What are some things to avoid during inflation?

Image Credits: todayonline.com

There are a few things you should avoid doing during inflation to make the best of the situation. For one, don’t overspend. Just because prices are going up doesn’t mean you have to buy everything that’s in sight. Try to be mindful of your budget and only buy what you need.

Also, avoid taking on additional debt. When prices are rising, it’s easy to get swept up in the hype and go into debt buying things you don’t need. But remember that you will be paying back that debt with inflated dollars, so it’s important to stay away from high-interest loans and credit cards.

Finally, avoid hoarding. It can be tempting to stock up on things when you know they’re going to become more expensive soon, but this can do more harm than good. Not only will you end up spending more money in the short term, but you will also be sacrificing storage space at home.

What should you do if your income doesn’t keep up with inflation?

If your income doesn’t keep up with inflation, you’re not alone. So what can you do to make ends meet? Here are a few tips:

Ask for a raise at work or find a new job that pays more.

Live within your means and don’t succumb to social media pressure.

Review your expenses and see where you can make adjustments. Maybe you don’t need that expensive subscription anymore or you can start cooking at home more often.

You may be feeling the effects of inflation in your everyday life. Prices for utilities, groceries, and transportation continue to go up, and it sometimes feels like there’s nothing you can do about it. But don’t worry, the tips we’ve put together in this article will help you thrive during these tough times. Hopefully, you will be able to manage your expenses better and make the most of your money. So what are you waiting for? Start putting these suggestions into action today!

Inflation is a sign of a healthy economy as it shows that the country’s wealth is growing. During inflation, you will experience periods of price surge. This is the perfect time to be more conscious of your spending. Do not worry! Inflation rates will eventually taper after several months. When this happens, your wallets can have the sigh of relief!

Ultimately, here are some strategies that you can employ to beat the inflation.

LET YOUR MONEY WORK FOR YOU

Let’s face it! To outpace inflation, having a high-interest savings account or long-term time deposit is not enough. Consider sparing some of your money to investment options that are safe to grow in spite of inflation. I am referring to asset classes such as mutual funds or pooled investments. Nowadays, many financial institutions in Singapore offer mutual funds at friendly rates. Read this article to learn more.

SLASH YOUR TRANSPORT COSTS

The Singapore government has declared this year as the Year of Climate Action. Take a page out of this initiative by getting on board with the public transport. You will not only save money by taking the bus or the MRT, but you will also minimize the carbon footprints.

Image Credits: pixabay.com

People who own cars spend around S$2,600 per year on petrol. Not to mention, there are other accompanying costs of car ownership such as parking and road tax. Taking public transport could diminish your costs significantly! Use your extra money to combat the price surge due to inflation.

CULTIVATE YOUR EMERGENCY FUND

An emergency fund is an account for funds set aside in case of events brewing from personal financial dilemma (e.g., loss of a job or having critical illness). When inflation rates elevates, your emergency fund becomes an added cushion to cover the sudden increase in the prices of goods.

It will keep you secured until you can adjust your budget. Experts recommend that you build an emergency fund covering your expenses for at least six months. If you have a family, then covering nine months’ worth of expenses would be a better target.

HUNT FOR GROCERY DEALS

A major chunk of our expenses is allocated to food. Whether you like it or not, inflation affects all goods differently. For instance, the cost of food rose faster than the general rate of inflation between September and October 2017. This price hike held across all types of food, from dairy products to vegetables.

Image Credits: pixabay.com

To get the best prices on food, you may use price comparison websites (e.g., diffmarts.com) or use online coupons. Spot the latest deals to bring down the cost of your basket!

Many Singaporeans look to their CPF to provide for retirement. As the General Election draws close however, some critics have panned the retirement scheme, saying it no longer suffices. Have a look at some of the realities of the CPF, and decide for yourself:

What is the CPF?

The Central Provident Fund (CPF) is a mandatory savings scheme for Singaporeans. This fund is used to provide for a range of crucial financial needs, such as healthcare, retirement, and home ownership.

Your CPF is automatically deducted from your wages, and your employer is also required to pay a portion into your CPF. Compulsory CPF contributions are as follows:

Age

Your contribution

Your employer’s contribution

Up to 50 years old

20% of monthly income

17% of monthly income

From 51 to 55 years old

19% of monthly income

16% of monthly income

From 56 to 60 years old

13% of monthly income

12% of monthly income

From 61 to 65 years old

7.5% of monthly income

8.5% of monthly income

Above 65

5% of monthly income

7.5% of monthly income

Your CPF is divided into an Ordinary Account (OA), a Special Account (SA), and your Medisave account. The interest rates for these accounts (as of 2015) are:

OA – 3.5% per annum

SA – 5% per annum

Medisave – 5% per annum

You do have the option to invest your CPF money in other schemes, based on an approved list. However, the returns are not guaranteed, and the government will not replace any losses you incur. You can see further details on allowable investments here.

Once you reach the age of 55, you will be able to withdraw all the money except for a required Minimum Sum. The Minimum Sum is placed in a Retirement Account (RA). From the age of 65, savings in your RA are disbursed to you in monthly payouts, which should ideally last till you are 90.

The Minimum Sum (as of 2015) is S$155,000. From the age of 65, this should provide monthly payouts of around S$1,200.

Is the CPF Alone Enough to Retire On?

The answer for most Singaporeans is “yes, but…” Here are some of the factors you need to consider:

Your CPF depletes very quickly when used to pay for your flat

The CPF rate barely keeps pace with inflation

A lot depends on how comfortable you want your retirement to be

1. Your CPF Depletes Very Quickly When Used to Pay for Your Home

Buying a home is one of the ways Singaporeans use their CPF. When you take out a HDB concessionary loan, the entirety of the down payment can come from your CPF*.

(*This does not apply to private bank loans, in which only 15% of the down payment can be made with CPF.)

CPF can also be used to pay for certain fees, such as the legal paperwork for the purchase. Mortgage repayments can be taken from your CPF rather than your bank account.

But this means that, if you use too much of your CPF money purchasing a house, there is a real possibility of it running out.

If you use HDB loans, the interest rate is 0.1% above the prevailing CPF rate (3.6% at present). If you use a private bank loan, the rate fluctuates according to an index, such as SIBOR or SOR. Both options can wipe out your CPF, and leave too little even for the Minimum Sum.

So if you want CPF to provide for your retirement, never overreach and buy a property beyond your means. If you buy the biggest house you can possibly qualify for, be aware that you could be forced to sell it to fund your retirement.

2. The CPF Barely Keeps Pace with Inflation

Singapore’s core inflation hovers at around 3%, which is on par with most developed countries. This means that the general cost of living goes up by 3% with each passing year, and your wealth is being depleted if it can’t grow as fast.

Given the CPF’s return of 3.5% and 5% (for OA and SA respectively), your real returns are only around 0.5% for OA and 2% for SA. This means that relying on CPF alone will provide for a very modest retirement.

Should you have plans after you stop working (e.g. travel the world, look after your grandchildren financially), it may not be a good idea to rely solely on CPF. You should speak to a financial advisor or a wealth manager about different investment products, which can complement your CPF.

3. A Lot Depends on How Comfortable You Want Your Retirement to Be

A pay out of S$1,200 a month is comfortable for some people, but painful for others. We are all used to different standards of living. If you enjoy a high income of S$15,000 a month, for example, switching to S$1,200 a month will be extremely painful.

As such, it is important to work out your desired Income Replacement Rate (IRR). This can be done with holistic financial planning, which also takes into account the amount you will need at retirement, and how long you have to get there (your investment horizon).

Do not believe any arbitrary “rules”, such as sayings that you must have a million dollars to retire in Singapore, or that S$500,000 is enough to quit your job. Such figures are not grounded in your specific needs. Speak to a qualified wealth manager or financial advisor to identify the sum you need.

A Note on Debt

Personal loans range from 6 – 8% per annum, and credit card loans reach around 24%. Your CPF interest rates (or the rates of even the most phenomenal financial products on the market) will never “outgrow” your debt. It is almost impossible.

If you want to retire well, you must pay down your debts early. Be an extreme miser with loans. Make comparisons every time you need money from the bank. You can find the best loans on SingSaver.com.sg.

In Summary:

The CPF is enough to provide the bare basics, when it comes to retirement. However, your retirement will not be lavish if you rely on CPF alone, especially if you are used to a more expensive lifestyle.

We frequently hear of the word “economics” in papers or conversations, but how useful or applicable is this course of study to the real world?

Understanding economics is in reality fundamental to understanding the price movements of every single good and service in our economy. It is the aggregation of the demand and supply forces. Indeed, when we see the airfare skyrockets after the end of school term, it is economics at work. Huge travel demand outweighing limited supply of passenger seats leads to propped up prices. As such, appreciating and capitalising on economic knowledge could end you up in deeper pockets.

While it may be too time consuming and superfluous to master all the economic theories, knowing a few essential concepts may come in handy in guiding our financial and behavioral decisions.

Thanks to the prudent policies administered by MAS, Singapore enjoys a low inflation rate of 2.8% on average since 1962. However, a simple comparison between the interest rates offered by various banks indicates a mere 1.3% as the most competitive rate for 1-year fixed deposits.

What this means: The fund sitting in your bank is losing 1.5% of its value to be exchanged into goods and services annually. Given that you have $100 in your bank today, you can afford to buy 50 McChicken burgers. But one year down the road, you can only afford to purchase 49.25 of them.

Course of actions to be taken: Since the saving rate is not commensurate with the inflation rate, we may be better off investing in alternative assets that provide higher yields. However, if every rational and irrational soul is doing that, risks abound as illustrated below.

Stock investment

(Image credit: thenest.com)

Investing in stocks can yield 2 kinds of returns, namely dividend yield and capital gains yield. The former tends to be more predictable than the latter, especially if the company holds a long term track record of constant or growing dividend stream.

How to value stocks: Dividend yield is an objective measure in guiding investment decisions since they are realised returns and a better indicator of future returns. On the other hand, be extra cautious during stock encounters with historically impressive capital appreciation. Gullible investors may be tempted to buy these shares as they often fail to realise the high variability of capital gains yield could be complicated by the problem of information asymmetry where insiders possess and exploit private information to the disadvantage of outsiders.

Course of actions to be taken: Both insiders and outsiders have to keep abreast of news and developments in the macroeconomy and international economies as they affect stock returns systemically.

Specifically for outsiders, it is crucial to have a good grasp of the economic fundamentals (such as the consistency of dividend payouts and growth potential) of the company that helps to steer towards a proper valuation. A long term investment horizon is more favourable as it puts them on a more level ground with the insiders. If the outsiders were to invest in the short term, speculation is usually involved since by definition, the fact that they do not possess the superior private knowledge is prejudicial to them.

For more well-heeled investors looking to diversify their portfolio, real estate investment seems the way to go. Similarly, real estate assets provide 2 types of returns, specifically rental yield and capital gains yield. Best of all, a residential property provides its owner(s) a physical shelter to live in. Despite these benefits though, investors should be wary of overpaying for homes.

How to value property: Rental yield is an objective measure in guiding investment decisions since it measures the payback period of the hefty mortgage loan that homebuyers commit to. The URA Masterplan and a concise understanding of demographics are vital tools in predicting the capital gains yield.

Course of actions to be taken: Beware of one-off anomalous sale transactions that are not reflective of the true market forces. Stay out of homes in which the overinflated prices are not underpinned by strong economic fundamentals (such as location, amenities and size). Buy during a recessionary period instead of an inflationary period. Timing the market makes an enormous difference in your bank account.

Investments aside, most of us contribute to the economy through our employment. But to maximise the return on our faculties and time, insights have to be drawn from the demand and supply forces.

Some simple mathematics to gauge how financially rewarding is a particular industry: If the staff turnover is high (due to long working hours, poor welfare, unchallenging job roles etc.), companies should offer higher wages to attract or retain workers.

However, this is not happening. Reason being a ready supply of potential (local and foreign) employees provides virtually no impetus for corporations to raise salaries. Does this plight sound familiar?

Course of actions to be taken: Instead of complaining about meagre wages, pursue a career in an alternative industry with market dynamics (i.e. less competition) working in your favour. Although it may seem counter-intuitive, you actually build greater wealth bucking the norm and doing what others don’t do. Better still, venture into a new industry and gain the first mover advantage.

Now you see, having a good understanding of economics is useful in our day-to-day living as it forms an integral basis for making financially sound decisions.