Living in Singapore isn’t cheap. With rising costs and temptations everywhere, it can feel tough to set money aside. But whether you’re saving for a rainy day, your BTO, or a well-deserved holiday, getting into the habit now can make a big difference.

Read this simple guide to help you get started.

#1: SET A CLEAR GOAL

Don’t just say “I want to save more.” Be specific! Are you saving for an emergency fund, a new laptop, or a holiday?

Once you have a clear goal, break it into monthly targets. Open a separate savings account to track progress. Naming it something fun like Japan Trip Fund can keep you motivated.

#2: LET YOUR MONEY WORK

Put your savings in an account that earns interest. Local banks like DBS, OCBC, and UOB offer savings accounts that reward you for crediting your salary or paying bills.

Every little bit of interest adds up, and your money grows even while you sleep.

#3: EAT OUT LESS

Eating out often can burn a hole in your pocket quickly. Cooking at home a few times a week can save you serious cash and help you eat healthier.

Image Credits: unsplash.com

Even simple home-cooked meals cost less than most hawker or café food. Plus, you’ll waste less and stretch your grocery dollar further.

#4: USE THE SAVINGS BUCKETS

Organize your savings into three buckets namely:

a. Emergency fund: For unexpected expenses like medical bills or home repairs

b. Short- to mid-term goals: For things like education, weddings or travel

c. Long-term goals: Retirement or financial independence

Having separate goals helps you stay focused and on track.

#5: BE CAREFUL WITH CREDIT CARDS

Credit cards can be useful for rewards, but only if you pay off the full amount every month. Otherwise, interest charges add up fast.

If you find yourself carrying a balance, switch to cash or debit to stay in control of your spending.

#6: PAY BILLS ON TIME

Late payments lead to extra fees and can hurt your credit score. Set reminders or automate payments to avoid unnecessary charges.

If you can’t pay on time, contact the provider early. They might offer an extension or payment plan.

IN A NUTSHELL

Image Credits: unsplash.com

Saving money doesn’t mean you have to give up fun. Start small, stay consistent and track your progress. Even saving an extra S$50 a month puts you on the right path. Small habits today build a more secure future tomorrow.

I’ve been on the lookout for a credit card with the best rewards and after some research, I stumbled on this combo:

UOB Lady’s Credit Card x UOB Lady’s Savings Account

I’m excited to make the most out of my savings and spending, knowing that signing up for both can earn me up to an impressive 25X UNI$ per S$5 spent, equivalent to 10 miles per S$1!

How It Works for Me:

UOB Lady’s Credit Card: I earn 10X UNI$ per S$5 spent on up to two of my preferred rewards category(ies). That’s 4 miles for every S$1 I spend.

UOB Lady’s Savings Account: I boost my rewards with up to an additional 15X UNI$ per S$5 spent on my preferred rewards category(ies), adding up to 6 more miles per S$1.

Plus, there’s no lock-in period, giving me the flexibility to choose and change my preferred rewards category(ies) every quarter.

And the best part? There’s no minimum spend required, allowing me to earn rewards on my terms!

Painting the Picture:

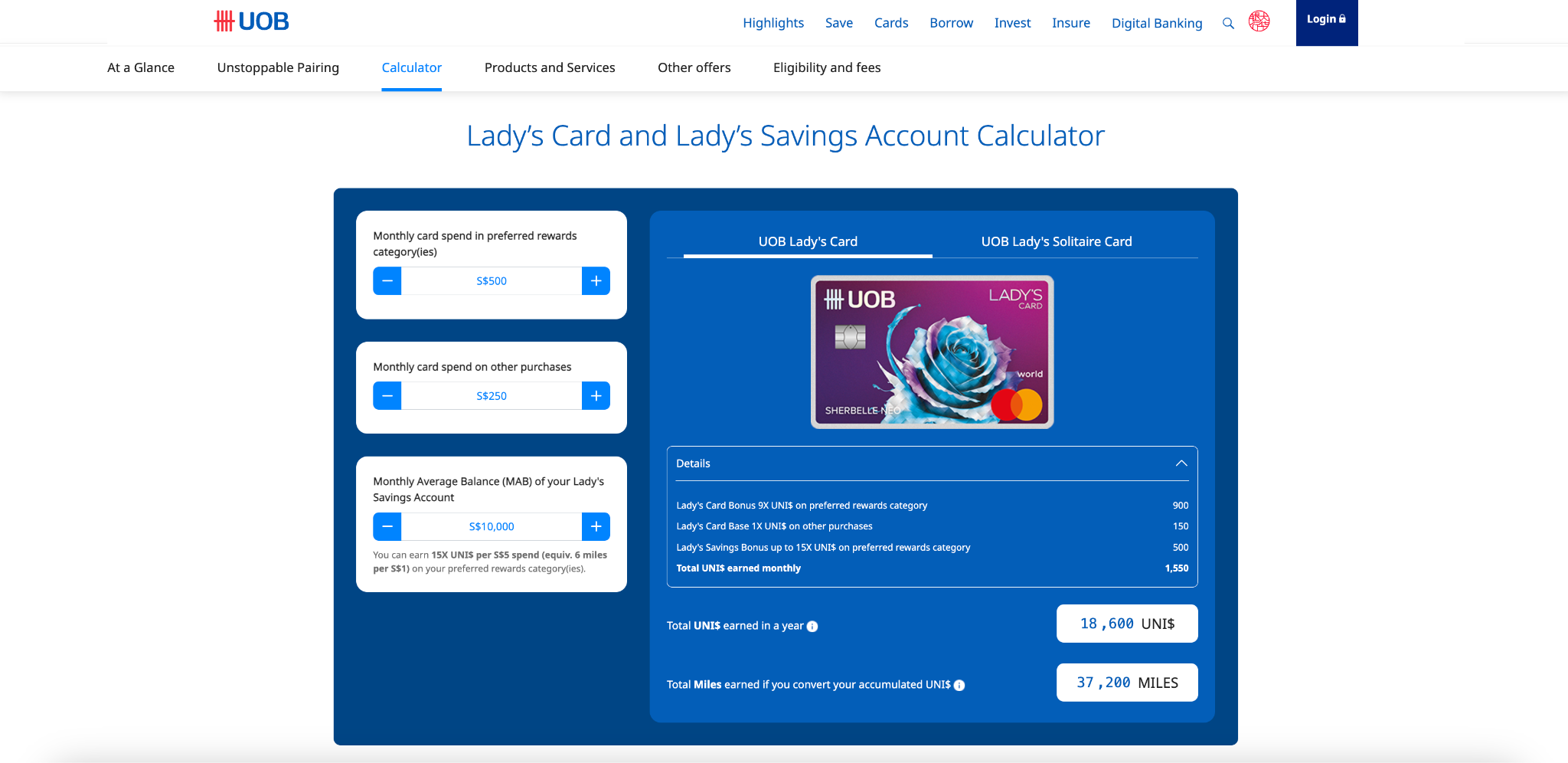

I have plans to maintain a S$50,000 Monthly Average Balance (MAB) in my UOB Lady’s Savings Account and spend S$800 each month on my preferred rewards category(ies) with my UOB Lady’s Credit Card.

For me, a monthly S$800 spend is easily attainable since I spend the bulk on the Beauty & Wellness and Dining categories.

Here’s the rough breakdown if you’re interested:

Gym membership ($100)

Beauty/cosmetic buys ($100)

Personal grooming such as hairdressing, facial treatment/hair removal, nails/lash/eyebrows, etc. ($300)

Dining at my favourite restaurant and ordering food via foodpanda ($300)

This means in just one month, I could rack up 3,200 UNI$.

Keeping this up for 12 months means I could gather a whopping 38,400 UNI$ in a year!

Redeeming My Rewards:

I can convert these UNI$ into 76,800 KrisFlyer miles (1 UNI$ = 2 miles).

With that, I could snag my round-trip business class ticket to Hong Kong* within a year! It would be my first-ever business class experience.

But if I decide not to spend all my UNI$ on flying, I have plenty of other options too.

I can redeem my UNI$ for rewards from a variety of dining, shopping, and travel merchants on UOB Rewards+.

In essence, whether I’m aiming for luxury travel or indulging in simple everyday perks, the benefits add up quickly!

*Based on Singapore Airline’s Saver Awards Chart as of October 2023, excluding taxes, charges, and fees.

Maximizing Your Rewards:

You can choose and change your preferred rewards category(ies) every quarter. These include:

Dining

Travel

Fashion

Beauty & Wellness

Family

Transport

Entertainment

This flexibility means you can adapt as your spending habits and priorities shift.

Switch to whatever categories you deem fit quarterly to maximize your UNI$ and get the best rewards for your spending and savings!

For example, during the year-end holiday season, I can switch my rewards category to Travel. This allows me to book air tickets and easily hit the S$800 spending target in a single transaction!

By consistently managing my spending, I can easily accumulate a significant amount of UNI$ annually. During travel months, I can reach the monthly spending target even faster by booking air tickets and covering other travel expenses.

If you have more savings to park aside and can maintain at least a S$100,000 MAB, you can earn an additional 15X Lady’s Savings Bonus UNI$ on your preferred rewards category(ies).

So, it’s smart to consolidate your purchases with the Lady’s Credit Card to maximize your Lady’s Savings Bonus UNI$.

Curious About Your Rewards?

Wondering how many UNI$ and miles YOU can rack up based on YOUR spending and savings?

Simply click this link to UOB’s official website and click on ‘Calculator’ to access the ‘Lady’s Card and Lady’s Savings Account Calculator’ to enter your details and see your potential rewards in a flash!

Just like this:

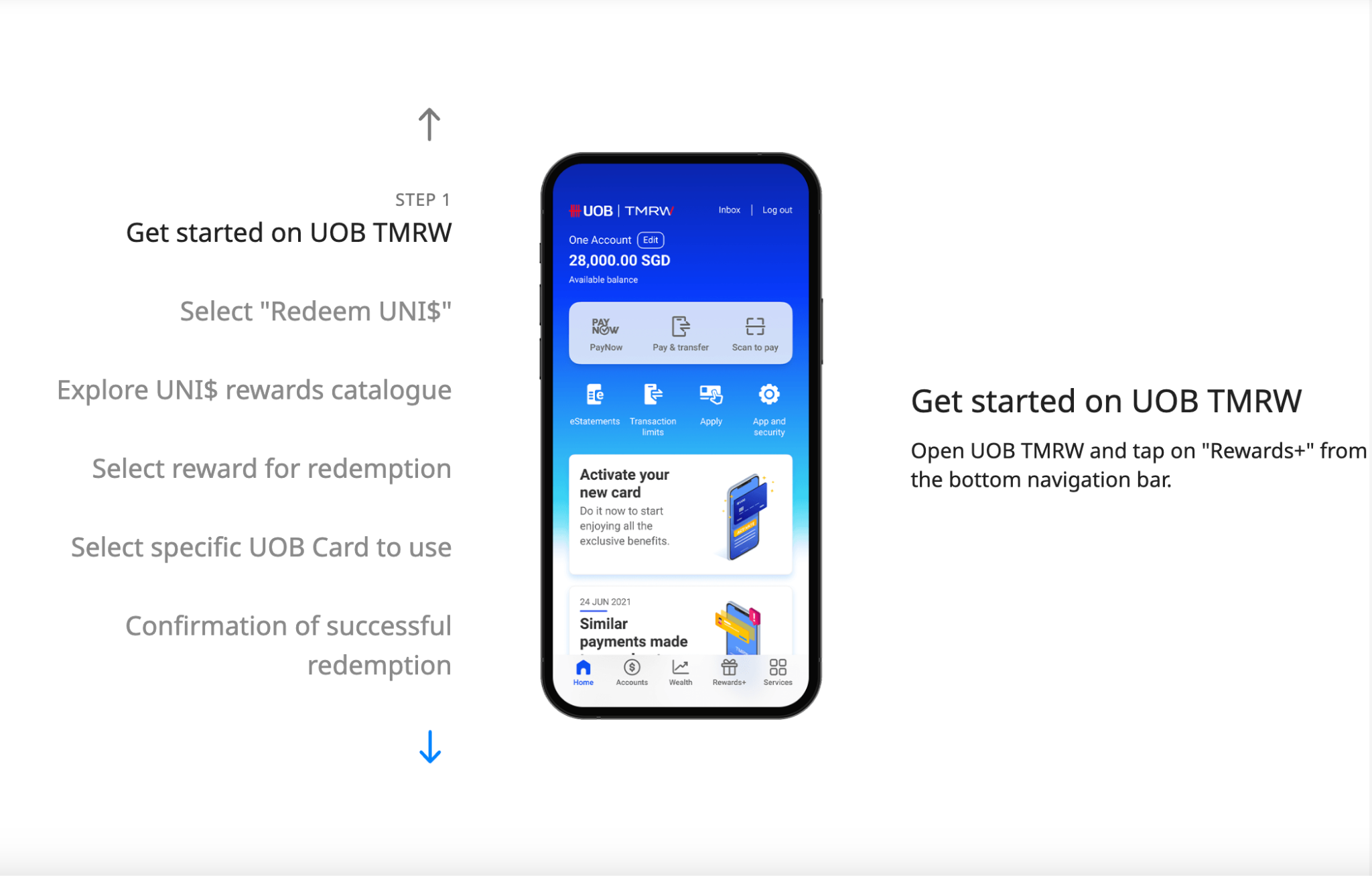

Subsequently, as a card member, you can easily view, track and redeem your UNI$ rewards all on the UOB TMRW app.

0% LuxePay Interest-Free Payment Plan over 6 or 12 months on your luxury purchase (shoes or bags)

Exclusive Birthday Treats during your birthday month

e-Commerce Protection for your online purchases

Complimentary Travel Insurance covering up to 100,000 USD

Receive a S$250 Sephora Gift Card when you spend a min. of S$6,000 on your UOB Lady’s Credit Card. Limited to the first 280 eligible cardmembers.

For the UOB Lady’s Savings Account:

Receive a Bespoke Puffy Bag with Rose Leather Charm worth S$98 by reBynd, an eco-conscious brand by Bynd Artisan, when you apply for the account online and deposits S$5,000 new funds into the account. Limited to the first 150 customers in each calendar month from 8 March to 30 April 2025 only.

That’s not all. UOB is also rewarding ALL customers who hold both the UOB Lady’s Credit Card and UOB Lady’s Savings Account as of 30 Apr 2025 with a lucky draw chance to win an Éclat KNOT Alone® Double Pave Bangle worth S$520 or Gentle Monster sunglasses worth S$490.

T&Cs apply, of course. Insured up to S$100k by SDIC.

So stop waiting and join me right away by signing up now here.

What’s better than payday? Free cash! With DBS/POSB, you can now get up to S$500 in cash rewards just by crediting your salary and spending with your POSB/DBS Credit or Debit Cards.

Here’s how it works:

Step 1: Start with S$300 Cash Reward

Register for the promotion from 7 August to 31 October 2024 and credit your salary of at least S$1,600 for three consecutive months to your DBS account. Once that’s set, you’ll be rewarded with S$300 cash! Just contact your HR department to make the switch.

Step 2: Unlock an Additional S$200

After your salary is credited, spend a minimum of S$500 monthly for three consecutive months on your DBS/POSB Credit or Debit Cards, and you’ll receive an additional S$200 cash reward—bringing your total to S$500!

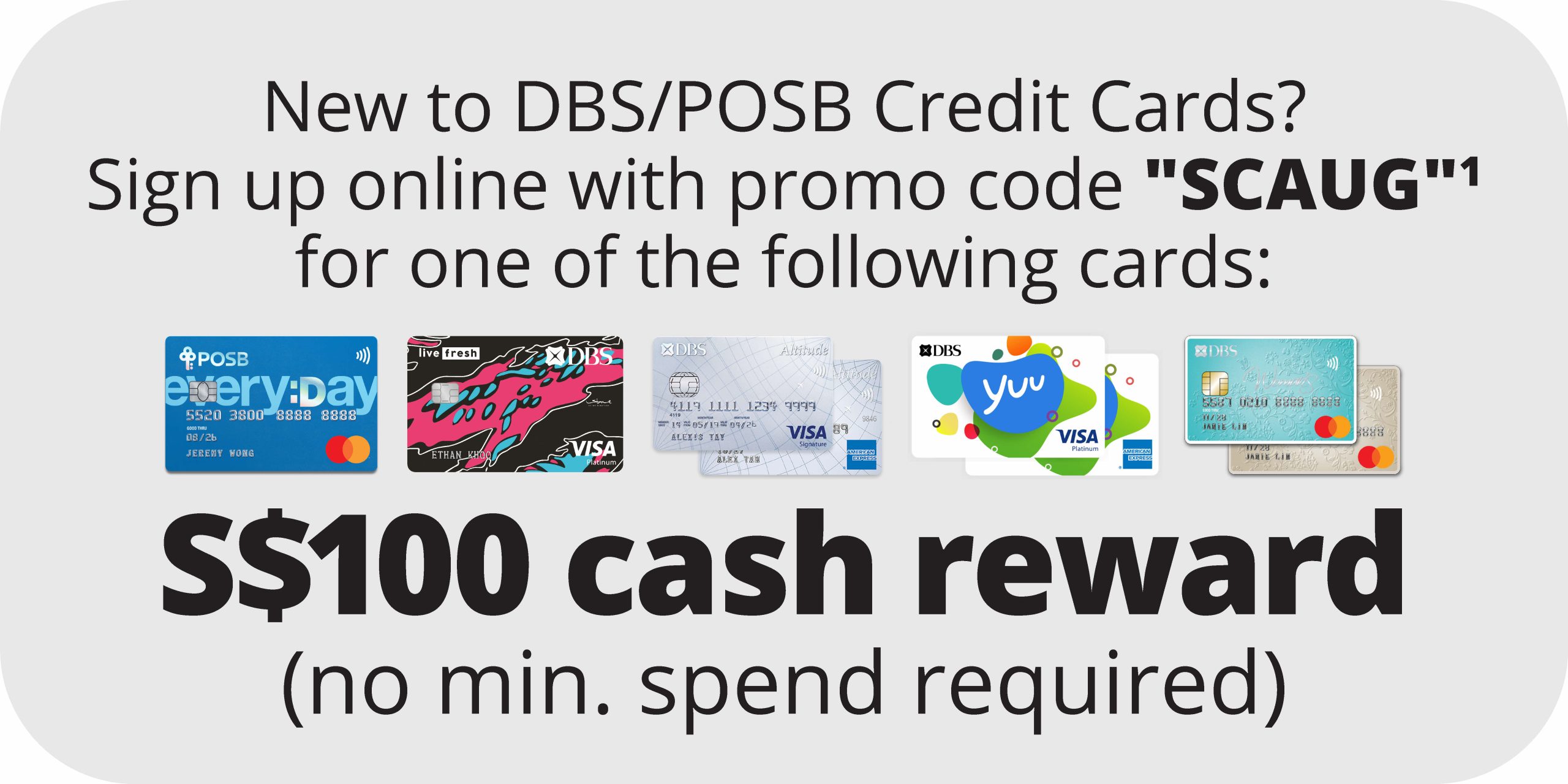

New to DBS/POSB Credit Cards?

If you’re new to DBS/POSB Credit Cards, apply now with the promo code SCAUG and receive an extra S$100 cash reward when you sign up! It’s the perfect way to kickstart your journey toward more rewards.

Reward Payout

Eligible Customers will receive the Cash Reward according to the schedule below:

Don’t miss out—register and credit your salary by 31 October 2024!

Terms and conditions apply.

Switch, spend, and get rewarded with DBS/POSB—because it’s time your money worked harder for you!

To get financial freedom you need to make wise investment decisions. While there are ample investment solutions available in the market, depending on any particular one becomes a tough decision to make.

However, stock trading, currency, commodities, and even crypto trading are becoming popular choices for modern investors. None of these can be considered a long-term investment solution.

However, fixed deposit is a long-term investment solution that comes with- Stability, and Security.

FDs are meant for investors who are willing to make decent money while being more protective than other investment solutions. However, to invest in FDs, you must know what is a fixed deposit account.

However, in the process of FDs, you need to invest a specific sum of amount in your FD account for a fixed period. This is called locking down your investment. In return, you will get a fixed interest rate, which is higher than standard savings account interest.

Also, you will get more benefits with FDs. Let’s find out!

Guaranteed Returns

One of the most compelling reasons to invest in a fixed deposit is the guarantee of returns. Unlike equities or mutual funds, where returns are subject to market fluctuations, fixed deposits offer a predetermined interest rate.

This means you know exactly how much you’ll earn over the investment period, making it a reliable way to grow your savings without worrying about market volatility.

Capital Protection

Fixed deposits are known for their capital protection. When you invest in an FD, your principal amount is secure and protected against market risks.

This feature makes fixed deposits an attractive option for conservative investors or those looking to preserve their capital while still earning a return.

Flexible Tenure Options

FDs come with a range of tenure options, from as short as a few months to as long as several years. This flexibility allows you to choose an investment period that aligns with your financial goals and liquidity needs.

Whether you are planning for a short-term expense or a long-term financial goal, there’s likely an FD term that fits your requirements.

Predictable Income Stream

Fixed deposits can be particularly beneficial for individuals seeking a predictable income stream. Most FDs offer periodic interest payouts, such as monthly, quarterly, or annually.

This can be especially useful for retirees or individuals looking to supplement their regular income. The fixed nature of these payouts ensures you can confidently plan your finances.

Tax Benefits and Special Schemes

In many countries, fixed deposits offer tax benefits under certain schemes. For instance, in India, certain fixed deposits with a tenure of five years or more qualify for tax benefits under Section 80C of the Income Tax Act.

Additionally, some banks and financial institutions offer special FD schemes with higher interest rates for senior citizens, making FDs a favorable choice for elderly investors seeking better returns.

Bag a Steady Income

Choosing the right investment solution is proportional to risk factors. With FDs, you not only bypass the risk factors but also engage in a steady investment solution.

While you are not the only person dealing with investments, making the right decisions is essential. You might be wondering about all investment solutions, especially in a competitive market where everyone is focusing on beating inflation.

Why would you consider FD instead of stocks and bonds?

Well, the answer is simple: You will get a steady return here, which is guaranteed.

Can you give us a particular amount you can assure of getting as a return on other investments? No! But with FDs, you can predict that even before you invest. So, if you want stability with a decent return, FDs are the prime source.

Life is full of surprises, and they’re not all the good kind. If a sudden big expense pops up, you might go into panic mode. Best to start building your emergency fund now and make it a minimum of 3 to 6 months of your usual spend.

With an emergency fund, you can sleep more peacefully at night knowing you’ve got a financial cushion if life throws curveballs your way. Take control of your money situation now for less stress and more stability overall.

Strategies for building your emergency fund

Cut out non-essential spending

Go through your monthly expenses and trim whatever you can, like eating out daily, entertainment, or subscriptions. Then redirect that money into your emergency fund. Even reducing discretionary spending by $50 a month can make a big difference over the course of a year.

Save a fixed amount regularly

Set up an automatic transfer of a fixed amount, say $100 per month, from your paycheck or bank account to your emergency fund. The amount depends on your income and expenses, so start with whatever you can afford. The key is to save regularly, even if just a little bit. Over time, you will build up a good amount.

Deposit any windfalls

When you receive unexpected money like a work bonus, cash gift, or even a government payout, put all or a portion of it into your emergency fund. Windfalls are a great way to give your fund balance a quick boost.

Where to keep your emergency fund

High-yield savings account

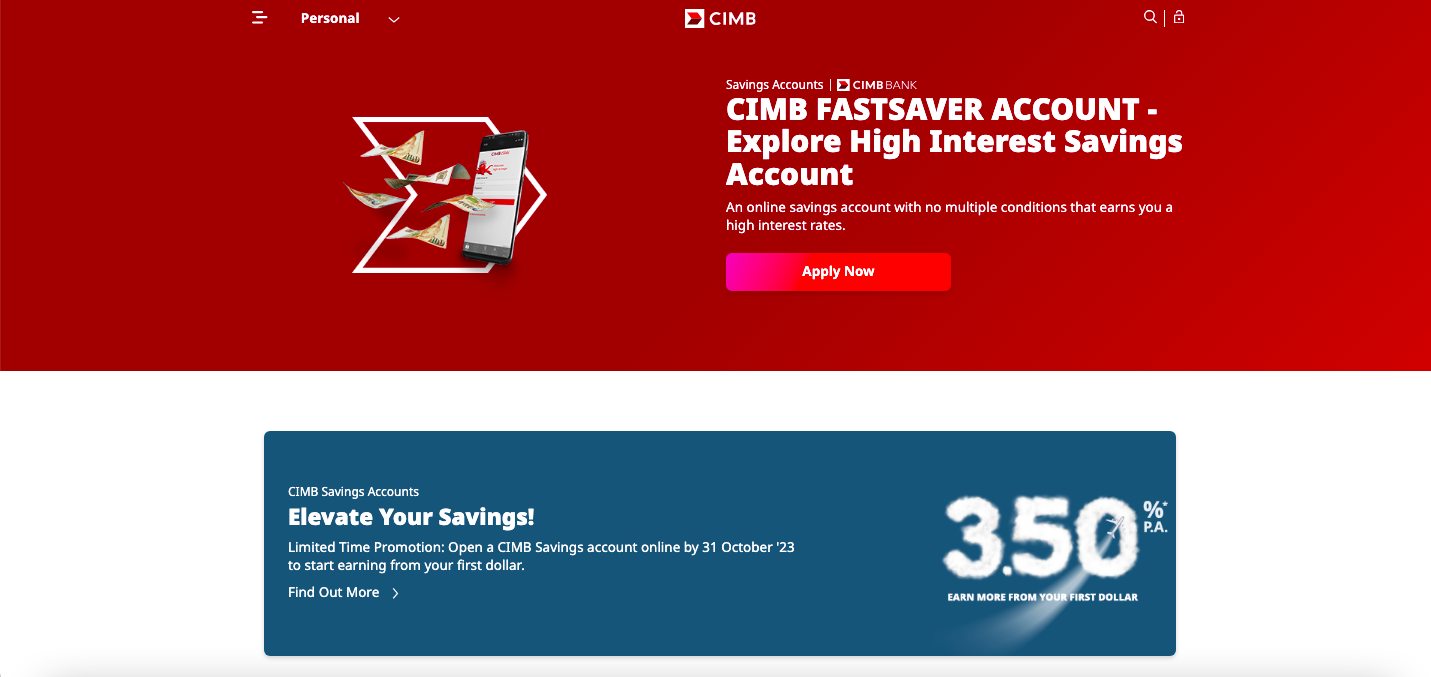

High-yield savings accounts are very liquid, meaning you can withdraw your money anytime without penalty. The interest rates are usually higher than normal savings accounts. Some recommended options are CIMB FastSaver (easy to start) and DBS Multiplier (easy to maintain).

Fixed deposits

Fixed deposits lock in your money for a fixed period, usually a few months to a year. In return, you will get higher interest rates than savings accounts, up to 3 to 4% per year. If you need to withdraw early, most banks will charge a penalty fee. So only put in money you won’t need for a while.

Singapore Savings Bonds (SSBs)

SSBs are issued by the Singapore government and you can earn up to 3%+ interest per year and your money is pretty safe. The catch is your money will be locked in for 10 years. Withdrawal is possible but you will need to pay a small fee.

Cash management accounts

Cash management accounts are a good option if you want to earn higher interest (fluctuates) but still maintain liquidity. However, they aren’t guaranteed by the Singapore Deposit Insurance Corporation (SDIC) so do your thorough research before jumping in.

Saving for your emergency fund is important and you better start saving now before the next financial crisis comes knocking on your door. Even saving $50/month can go a long way. Remember, you want enough to cover at least 3 to 6 months of essential expenses in case anything happens. Once you hit your target, don’t stop—keep adding money whenever you can. The more you save, the more prepared you will be for unexpected events. Saving money may not be the most fun thing to do every month, but having that emergency fund will guarantee plus chop give you that peace of mind if life takes a wrong turn.