Singaporean households are taking on more debt than before, yet the broader financial landscape tells a reassuring story. Household balance sheet numbers from the recent Singapore Department of Statistics (SingStat) release showed that liabilities grew for the sixth consecutive quarter, rising 5.2% in the first quarter of 2025 compared with the same period a year ago and reaching $384.1 billion. This marks the sixth consecutive quarter of rising debt, driven mainly by increased borrowing for property purchases and other major expenses.

But don’t mistake rising debt for financial distress. For many Singaporeans, taking on long-term loans to finance big-ticket items such as homes is a sensible strategy, especially when balanced with careful cash management for everyday costs. In a city where the cost of living never sleeps, spreading payments over time helps families better manage their cash flow.

Image Credits: unsplash.com

Meanwhile, household financial assets have grown even faster, increasing by around 7.5% compared with a year ago to an estimated S$670.1 billion. This means that the liquid assets Singaporeans hold, including cash and bank deposits, comfortably cover their debts. With assets outpacing liabilities, overall household net worth remains healthy, climbing 8.1% in the first quarter compared to a year earlier, reaching $3.1 trillion. This marks a slight slowdown from the previous quarter’s 8.5% growth, but the momentum is unmistakable.

Image Credits: unsplash.com

Experts point out that housing loans continue to dominate household debt portfolios. Mortgage loans now represent more than 70% of total liabilities. Yet, resilient property values have provided a sturdy cushion, shielding households from overexposure and bolstering their net worth.

In essence, borrowing when paired with strong asset growth and responsible repayment can be a sign of financial strength rather than vulnerability.

As you strive to keep up with the vibrancy and dynamism of the Singapore workplace to sustain your daily needs, being intentional with your budget is crucial. Cutting your expenses in half while maintaining a comfortable lifestyle is achievable. Here are some hacks to help you save money and reduce your expenses.

#1: PREPARE HOMEMADE MEALS

At the onset of the pandemic, I started learning how to cook. Eating out can be costly, and making my meals at home helped me to be conscious of my spending and what I put in my body.

You can create a weekly meal plan using the ingredients you already have and make a shopping list of any missing items. Shopping online can also help you reduce costs through store vouchers and occasional sales. Opting to include more veggies in your meals can also lower your food costs.

#2: SHOP SMART

When shopping for groceries and other essentials, keep an eye out for deals and promotions to save money. You can also consider buying toiletries in bulk to reduce costs.

Additionally, you can explore shopping at local markets instead of big chain supermarkets. Local wet/dry markets offer a greater variety of options and provide an opportunity to haggle for the best prices. Gain freedom of choice while sticking to your budget!

Singapore offers a wealth of free or low-cost entertainment options, such as museums, festivals, and parks. Take advantage of these options instead of costly activities like shopping or hotel hopping.

Furthermore, review your monthly expenses to see if there are areas where you can cut back. For example, you could cancel your cable TV subscription and retain your Netflix subscription only.

#4: COMMUTE WITHOUT CARS

With a reliable public transport system that continues to expand, you can easily ride buses and trains on a regular basis. Consider using public transportation instead of owning a car, which can be subject to high taxes and fees.

Image Credits: unsplash.com

Not to mention, you would also have to maintain the vehicle’s condition and regularly purchase petrol.

#5: EAT THE LEFTOVERS

Don’t let your dinner leftovers meet a moldy end in the back of your fridge. Forgetting about them wastes both money and food. Instead, consider enjoying them for lunch the next day or incorporating them into a new dish, like egg fried rice. With a bit of creativity, you can spruce up your egg fried rice by adding leftover rice and other ingredients to make Uncle Roger proud!

#6: SWITCH TO REUSABLE ITEMS

Make a positive impact on your wallet and the environment by ditching disposable items like paper towels, sandwich bags, and single-use water bottles. Instead, opt for reusable alternatives.

For example, a pack of paper towels can cost around S$4.50 at FairPrice, while a hand towel from the same store is only about S$2.90. By switching to a reusable hand towel, you’ll save S$1.60 right off the bat and get many more uses out of it. Plus, using the hand towels you already have tucked away instead of grabbing a new paper towel sheet every time you make a mess means fewer trips to the store and less waste in the trash bin. It’s a minor change that will benefit you in the long run.

#7: STEER AWAY FROM COSTLY HOUSING

One of the biggest expenses for most people in Singapore is housing. To reduce your housing costs, consider living in a less expensive area or finding roommates to share the rent with. Downsizing to a smaller flat or house can also be a viable option.

Yes, you need shelter, and you want to live in a lovely place with amenities. While these factors are important, you don’t want to spend so much on your housing that you can’t achieve your financial goals.

#8: AVOID USING CREDIT CARDS

For everyday expenses, avoid using credit cards. Remember that interest rates can be high. Instead, consider using cash or debit cards to keep track of your spending and avoid accumulating debt. By being mindful of your spending habits, you can achieve your financial goals and avoid the burden of credit card debt.

#9: CREATE YOUR OWN THINGS

Don’t spend money on things that you can make yourself. Search for DIY tutorials on YouTube, Pinterest, and social media platforms to create your own soaps, household cleaners, ant killer, rugs, and face scrubs. The possibilities for home DIY projects are endless!

#10: OPT FOR CHEAPER ALTERNATIVES

Cheaper alternatives for products and services are readily available but finding them requires some research. For instance, you can save money on handphone plans or other service subscriptions by choosing more affordable plans or cancelling unnecessary subscriptions.

When it comes to cleaning supplies, medications, and groceries, opting for store or generic brands can help you reduce your expenses while still getting quality products. You can also choose to splurge on a few select items to treat yourself.

Image Credits: unsplash.com

With a dash of foresight and smart decision-making, you can enjoy the Lion City’s luxuries while staying within your financial means.

A credit score is a measure of your credit behavior, predicting the likelihood of you paying back loans on time based on information from your credit reports.

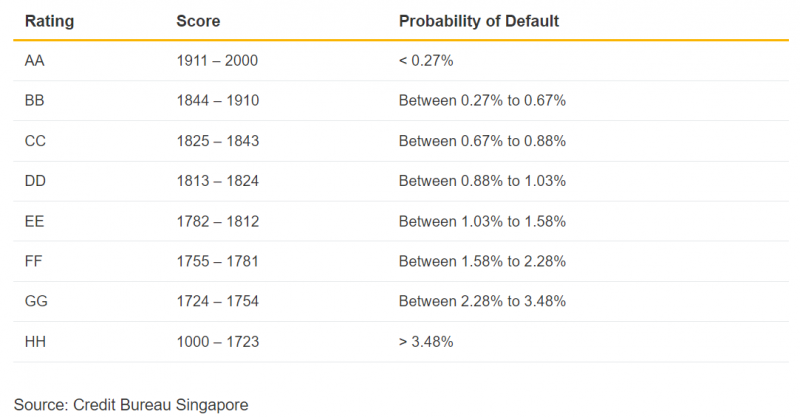

In Singapore, credit scores are determined by algorithms that track credit usage. Credit scores are ranked according to the following risk grades: AA is the highest, while BB or CC indicate late repayments or delinquency, and DD or lower indicate defaults. The credit score risk grades are as shown below.

Image Credits: valuechampion.sg

You can easily obtain a credit report from the Credit Bureau of Singapore’s website (CBS) for S$8.00 with prevailing GST. Alternatively, you can get it for free by applying for a new credit card or a loan facility.

Before we dive into ways to improve your credit score and manage your debt, it’s important to understand the significance of having a good credit score. A good credit score in Singapore can provide you with access to larger loans and better interest rates. You see, your credit score is a key factor in determining your loan eligibility for purchases like a flat or a car.

In addition to facilitating loan approvals, a good credit score can also have a significant impact on your career in finance. The Monetary Authority of Singapore (MAS) considers credit checks to be essential for employees and potential hires in financial institutions. Low credit scores can lead to job rejections in the finance industry.

Now, let’s focus on how to improve your credit score. As mentioned above, a good credit score can help you to elevate your career in finance and to boost your eligibility for larger loans. In a place where the cost of living is relatively high, it’s necessary for you to manage your debts and maintain a good credit score to be financially stable. Here are some tips to help you manage your debt and improve your credit score:

#1: MANAGE YOUR DEBT

Be organized. Make a list of all your debts, including your personal loans, credit card balances, and mortgages. Keep track of the interest rates, due dates for each debt, and the minimum payments.

#2: PRIORITIZE HIGH-INTEREST DEBT

Focus on paying off high-interest debt first, such as credit card debt. Prioritizing debt can affect how quickly you can become debt-free. Focusing on high-interest debt will save you more money and allow you to redirect your funds to other financial goals, while following the timeline you set.

#3: AVOID LATE PAYMENTS

Can you imagine how continuously paying for late fees can affect your motivation levels to pay off your debt? By the time you receive your third delinquent payment letter, your credit score would already have dropped, regardless of whether the bank waives your late payment fee. Late payments can hurt your credit score, so ensure that you pay your bills on time.

Set up virtual reminders to help you stay on track. Or ask your financial institution how you can set up automatic payments.

#4: KEEP YOUR CREDIT UTILIZATION LOW

Your credit utilization ratio is the amount of credit you’ve used compared to your credit limit. Maintaining low credit utilization can improve your credit score. If possible, try to use no more than 30% of your available credit.

#5: MONITOR YOUR CREDIT REPORT

Check your credit report regularly to ensure that all the information is accurate. Get your credit report from the Credit Bureau of Singapore. If you find any errors, do not be afraid to raise them.

#6: WORK WITH YOUR BANK

Do not avoid calls or letters from your bank, its debt collectors, and lawyers. Hanging up the call can affect your opportunity to find better ways to pay off your debt. Remain cooperative and reachable. If you are cooperative, your bank is more likely to help you restructure your payment schedule.

Image Credits: unsplash.com

In conclusion, managing your debt and improving your credit score in Singapore requires good financial habits and discipline. By following these six tips, you can upgrade your financial situation and achieve your financial goals in a realistic timeline.

Money is a strong tool that can help you achieve your goals. It can provide stability for your family and allow you to save towards important milestones. To achieve these things, you must know how to make your money work for you.

Making money work for you pertains to using money to make more of it. Your financial decisions can guide you through this. Start by learning how to budget!

#1: LEARN TO BUDGET

Change the way you handle money by budgeting. When you are budgeting, you become more purposeful about where you spend your money on. You are making money do what you desire, rather than spending it without a plan.

Budgeting includes prioritizing your spending, avoiding new debt, paying off debt, identifying harmful financial habits, reducing your spending, and saving for the future. You may need to adjust your budget from time to time.

#2: ELIMINATE DEBT

Debt means your money is not working for you. Your money is going towards paying the interest. Debt creates limitations and financial burdens.

Paying off debt allows you to redirect your funds towards things that are important to you. For instance, you can save up for graduate studies or create your retirement fund. You can begin investing money and allow your wealth to grow.

#3: SAVE AND INVEST

Once you have freed yourself from debt and have extra cash, you can put your money to work by saving and investing. The amount that you will save will depend on your lifestyle, age, and goals.

In addition to having an emergency fund, you will also need to have a retirement fund. You should also consider having the following:

a. education savings

b. travel fund

c. down payment for a house

d. business capital

e. car fund

f. long-term savings for you and your dependents

Image Credits: unsplash.com

Lastly, investing in yourself is one of the best investments you can make. While you might not be able to pinpoint an actualized return on investment, you will eventually see the results in time.

“Home life ceases to be free and beautiful as soon as it is founded on borrowing and debt.” – Henrik Isben

One of the most common issues that individuals bring into a marriage is debt. Money is high on the list of topics that couples fight about, and it is the among the top reasons why couples get divorced. Financial issues increase marital discord and stress.

If you are worried about marrying someone with debt, you must realize that you can help each other out. You are a team!

#1: BE TRANSPARENT ABOUT YOUR DEBT

Be honest about your debt situation. Hiding debt from your spouse before the wedding is simply a horrible idea. Your partner needs to know your economic situation and vice versa. You can only make shared decisions after talking about money.

#2: CREATE DECISIONS AS A TEAM

Married individuals have many financial arrangements to make. After discussing your pre-existing debt, decide how you will move forward together. Consider the following questions:

a. How will each partner contribute to the household bank balance?

b. Are you going to combine assets by opening a joint account?

c. What kind of investments will you make?

d. How do you plan to tackle previous debt?

#3: SET A MONEY DISCUSSION NIGHT

The key to surviving marriage and debt is to set a budget as a team. Find a quiet place and sit down for a discussion before next month begins. It may seem like a simple solution, but it is the answer to many money issues in marriage.

#4: NEVER PLAY THE BLAME GAME

Once you are married, you must work together to eliminate your debt. “My” debt turns to “our” debt. Having this perspective creates a significant difference.

Image Credits: Asia Wedding Network

#5: CONSIDER PERSONAL LOAN TO RELIEVE SOME FINANCIAL BURDEN

Prudent use of personal loans can save you more in the long run, especially if you’re currently saddled with severe credit card debt or are facing a financial emergency that could wipe out your savings. Ultimately, the only way to prevent bad debt from snowballing is to have the discipline to control your spending until your loan is repaid. If you find yourself in any of the above situations and are looking for a personal loan to help relieve some of your financial burden, be one of the first 2 applicants daily to have your 1st year’s interest (up to S$550) covered by SingSaver. Click here to learn more. Offer until 21st Mar 2022. T&Cs apply.

Stick to the plan and motivate each other. Living without debt is not easy, but it is worth it.