So, you want to be a millionaire? Sure! But first things first, make sure you’re not spending too much money way over your budget.

For folks looking to attain financial freedom, we recently wrote on some challenges to save more money which might be of powerful assistance. Some concepts, like the 1% trial or 52-week challenge, can be new ideas to try out.

Meanwhile, for today’s article, we will look into 10 well-rated books to read if you want to be a millionaire. Let’s roll with the titles!

#1: “The Simple Path to Wealth” by JL Collins

Most of us want to become millionaires. But the questions we may not know how to answer can include:

- How do I get started with investing?

- Why is debt a must-avoid, and what should I do if I’m heavily indebted?

- Is it possible to use my money wisely and not gamble it away on fluctuating stocks?

Simple, engaging, and informative, this book delivers solid advice on investments, the stock market, and real-life implementation tips.

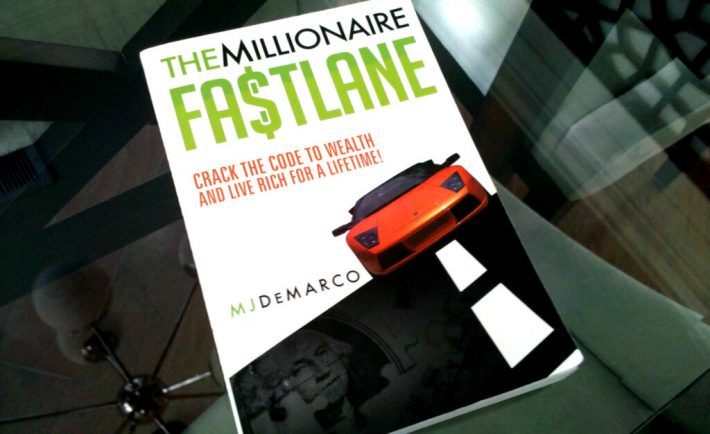

#2: “The Millionaire Fastlane” by MJ DeMarco

“The Millionaire Fastlane” is a straightforward guide to wealth generation written by a self-made entrepreneur who has learned from both his successes and his failures.

A fan of non-conservative approaches, DeMarco explores the theory that success is tied to effort. You are the vehicle, and the fuel, engine, etc., can be tailored to your specific route. The author’s advice is concise and valuable for those seeking to grow their wealth via the expressway.

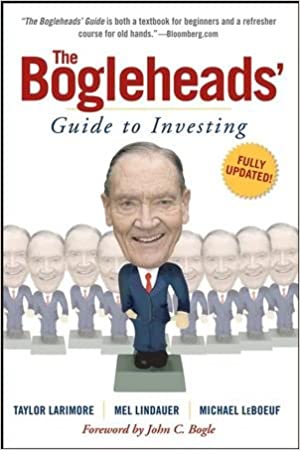

#3: “The Bogleheads’ Guide to Investing” by Taylor Larimore, Michael LeBoeuf, and Mel Lindauer

Do you know what Bogleheads are? It’s a term referring to investing enthusiasts who hold fast to the investment advice of John Bogle, the founder of Vanguard and an investor advocate.

This guidebook provides the reader with straightforward investing and financial advice designed to help the average person profit from long-term wealth creation. This book also advises readers on how to survive economic downturns and keep their footing rooted.

#4: “The Richest Man in Babylon” by George S. Clason

More a parable than a textbook, Clason’s work revolves around the subject of thrifting, financial planning, and personal wealth.

The lessons presented in this bestseller are timeless and easy to follow. You will learn how to save, spend less than you earn, and make money earn more money through seven simple rules. If you want to know, start flipping.

#5: “The Intelligent Investor” by Benjamin Graham

Known as the father of value investing, Benjamin Graham was a well-known economist and professor whose students include legends such as Warren Buffet.

Readers of “The Intelligent Investor” will focus on learning the fundamentals of value investing. Graham teaches us how to guard our investments and make them successful.

If you want to avoid common investment pitfalls like channelling too much energy to the changing sentiments of the market, this book will do the trick. Updated by famous financial journalist Jason Zweig, this edition will keep Graham’s lessons appropriate for modern demands.

A must-read for any aspiring millionaire!

#6: “How to Win Friends and Influence People” by Dale Carnegie

What does winning friends and influencing people have to do with getting rich? Plenty!

To achieve success, one must learn to work with others. They could be your friends and family members, investment advisers, business partners, or even salespeople.

Nobody who aspires to become a millionaire can afford to ignore Carnegie’s advice on how to win people over with your way of thinking. The tips conveyed in this book will help you think in fresh ways and cultivate relationships that lead to unlocking your maximum potential.

#7: “Conscious Business” by Fred Kofman

The author explains the term conscious business as the practice of expressing your passion and values through your work.

Rather than blindly chasing after profits, the conscious business person leverages their values into helping business stakeholders attain happiness.

Kofman explains that business people who approach their work with integrity, responsibility, and genuine leadership are more likely to achieve personal and financial success beyond the workplace.

#8: “Secrets of the Millionaire Mind” by T. Harv Eker

“Secrets of the Millionaire Mind” concentrates on identifying internal traits that can lead to financial success.

Eker does that by identifying one’s money and success blueprint hidden deep within the subconscious mind. For those whose blueprints are not built for success, the author offers a chance to reset one’s mental patterns to improve the likelihood of financial triumph.

#9: “The Millionaire Mind” by Thomas J. Stanley

Peeps who are keen to explore further the interaction of mindset and wealth, Stanley’s writings can offer a glimpse into the millionaire’s headspace.

While many may assume that millionaires are well-connected graduates of prestigious schools who flaunt their wealth, the truth might be more surprising. Those who want clear road maps on how millionaires found their niches, look no further.

#10: “Think and Grow Rich” by Napoleon Hill

We will close our list with one of the classic books on wealth creation and financial success. Hill’s “Think and Grow Rich“ lets you in on money-making secrets inspired by Andrew Carnegie’s magic formula for success.

The book will share with you 13 steps towards riches. From the attainment of desire to influencing the subconscious mind and putting it into action, you will get the fortune you want if you’re ready to welcome it.