Image Credits: loanadvisor.sg

Image Credits: loanadvisor.sg

Bankruptcy is a big word, and some people fear it. But if one were to be familiar with its foundations, maybe it wouldn’t be that terrifying.

According to Investopedia, bankruptcy is a legal proceeding in which a debtor and a creditor resolve debts through the court system. The debtor has its debt resolved while the creditor obtains repayment based on the debtor’s available assets.

In Singapore, section 61 of the Bankruptcy Act states that debtors may be declared bankrupt when a debt has fallen due and is worth at least S$15,000.

For folks considering bankruptcy, here are the basics you should be aware of.

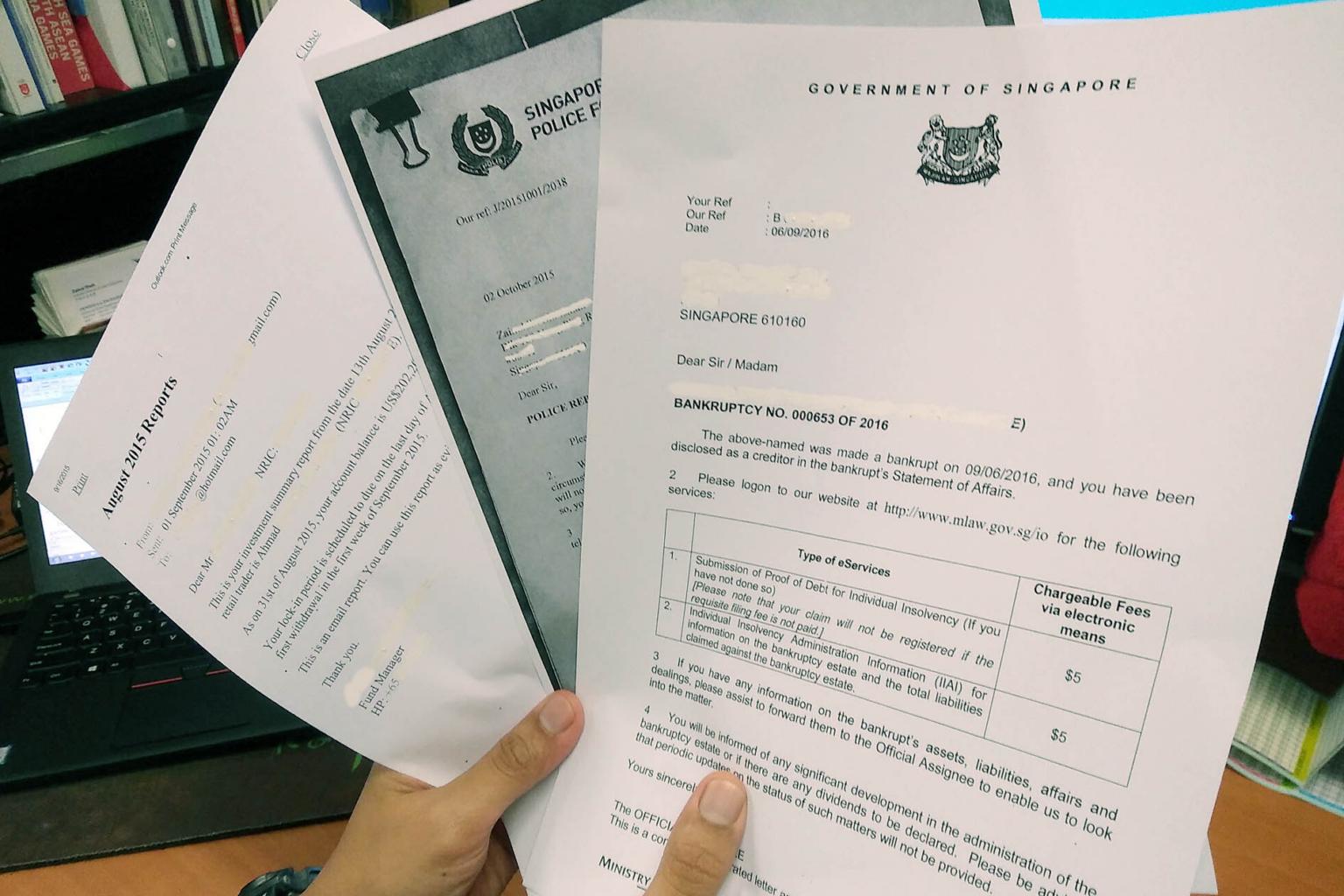

After declaring bankrupt

Once you are declared bankrupt, you gain exemption from your creditors’ legal actions intended to reclaim debt from you. A public servant called an Official Assignee (OA) would examine your financial capabilities and design a suitable repayment plan.

Think of it as your bankruptcy supervisor.

Your OA will ensure that you make monthly contributions on your road to being discharged. They will set up this monthly plan after evaluating your financial resources, income and credentials, household expenses, and the economy’s overall status.

Wave goodbye to your assets

Image Credits: EdgeProp

During the bankruptcy proceedings, your OA will sell any assets you possess to pay off your creditors. This can include items from artworks to furniture and even sentimental gifts.

The OA will not sell off any “protected assets”, which include:

- HDB flats if the owner is a Singaporean

- Central Provident Fund (CPF) contributions

- Life insurance policies if it benefits the bankrupt’s immediate family members

- Compensation awarded legally due to personal injuries or wrongful acts against the bankrupt

While it may be tempting to hide or dispose of your possessions quietly, lying to your OA or evading the procedure on purpose can lead to fines of up to S$10,000 and/or up to 3 years in prison.

Not worth it, ladies and gentlemen.

Ready for restrictions on daily activities

Bankrupt persons in Singapore are subject to various duties and responsibilities. Gambling, travelling, seeking credit, or managing businesses while involved in bankruptcy proceedings can lead to monetary fines or jail time.

These restrictions exist to prevent bankrupts from exploiting corporate structures, concealing income, hiding assets, or generally cheating the system. However, the OA can ease or accommodate these restrictions.

Their willingness to do this is based on your level of cooperation. If you are engaged in the bankruptcy process and consistently settling your debts on time, the OA is more likely to view you as reliable and ease those limitations.

Especially so in the business realm, full cooperation, including the provision of requested documents promptly, is the single best strategy for getting those restraints lifted as soon as possible.

If you feel that the OA is not treating you fairly or is imposing ridiculous restrictions, the ideal course of action is to seek the court’s review. Simply ignoring the limits is likely to end with criminal charges against you.

Look forward to the discharge

Image Credits: The Straits Times

Bankruptcy is not forever. Eventually, your debts will be paid, and you will be discharged from them. However, a discharge is dependent on the fulfilment of specific conditions and approval from either the OA or the High Court.

First-time bankrupts with debts of less than S$500,000 may be discharged after 3 to 7 years. For repeat offenders, it will take between five and nine years.

There is a well-known belief that a bankrupt is automatically released after three years, but this is not true. To speed up the process, cooperate fully with the OA and make sure you’re keeping up with your monthly repayment amount.

Bankrupts who have debts exceeding S$500,000 will need to apply to the High Court to seek an Order of Discharge. However, the courts will examine the interests of all involved parties before making a decision.

Noncompliance with the OA or any violation of behavioural restrictions will make the court reluctant to dismiss your bankruptcy.

Resume life after bankruptcy

Being discharged from bankruptcy is not necessarily a return to normal. At least not immediately. Depending on the circumstances of your bankruptcy, the courts may require you to entrust any new properties to the OA if debts remain after discharge.

Should the owed amount be repaid, bankruptcy can only be removed from your records after five years. If not, the bankruptcy status will remain in your public record permanently. Employers and creditors will have access to this information, so this should be a huge red flag for concern.

Final thoughts

Image Credits: AsiaOne

Bankruptcy is not a walk in the park, but it is not the end of the world too. The Bankruptcy Act is designed to be fair to both debtors and creditors and focuses on providing rehabilitative measures to the bankrupt.

For the severely indebted, bankruptcy can provide a mechanism to help recover financial health and gain a second chance at life. Be sure to cooperate fully with the courts, and the OA and the law will likely give you more space to breathe.