The new year beams with career possibilities and job opportunities. As more and more stores have opened, many eager candidates have been given the chance to shine. These candidates bring their best behavior during job interviews. They give answers that the employer wants to hear and attempt to convince him that he or she is the right person for the job.

Knowing which interview red flags to watch out for can help you speed up the process of screening and hiring. You do not want to feel the costs of hiring badly, nor do you want to send the wrong message to an interviewer. Consider these tips.

#1: ARRIVING LATE FOR THE INTERVIEW

Tardiness demonstrates a lack of respect for people and their time. It is the hallmark of unsuccessful people. When a candidate arrives late, he or she gets flustered and apologetic. This type of person can keep meetings from starting, conduct customer visits following their schedules, and constantly say that they will be late for work.

With so many qualified candidates, why would an interviewer hire someone who is late? An employer must not hire someone who is late for the most important meeting of his or her career.

#2: LACK OF COMPANY KNOWLEDGE

Red flags are shinning when you show little to no knowledge about the company’s products or services, customers, and target audience. It is essential for a candidate to research on the company’s background as they prepare for the interview. Start by reading through the pages of the company’s website.

A candidate who has no knowledge about the company shows lack of preparation and interest about the prospective role. You may come across as someone who fits poorly within the company’s values and goals.

#3: LACK OF OWNERSHIP

Another red flag is a candidate who does not admit to any responsibility for his or her past mistakes. It is unpleasant if you blame your co-workers, bosses, and previous company for failed projects and more.

As an interviewer, you must listen carefully to the reasons why someone left his previous job. The right candidate will admit to errors, make thoughtful mistakes, and do their best to repair their problems.

#4: BRAGGING ABOUT OTHER OFFERS

If you want to convey that you are desirable, bragging about your other offers is not a good idea. Arrogance is not an attractive quality. However, mentioning about other offers may not always be a red flag. At the later stages of your job application, it is alright to be transparent when it comes to your other offers. You can say something like this:

Image Credits: pixabay.com

“I am very interested in the position you have offered me. Please let me know the timing and details for the next step, because I am also evaluating another offer.”

While some of us have a career that makes us feel energised every single day, most of us are in a job that we fantasise about quitting. Whether it’s the early mornings, the stress level, or the over-commitment of time, there are often a few common reasons.

If you’re feeling at a loss on what to do, this article will share some red flags you need to ponder over. Maybe it’s about time you quit your job and say “yes” to a better work opportunity somewhere else?

#1: Spending all weekend dreading Monday

Most of us suffer Monday blues, but if you are dreading Monday morning so much that it leeches all of the fun out of your weekend, quitting should take a front position on your mind. A career that drains and has to have you give up a well-deserved weekend isn’t worth keeping.

#2: Having deep hatred for your job

Image Credits: Getty Images/iStockphoto

Do you hate everything about your job – your boss, your employees and, even your work tasks? It’s time to quit. Plain and simple. Yes, we understand that most of us are working to bring food to the table. But consider your mental health if you want to keep your feet on the race track.

#3: Getting passed over for deserved promotions

Have you been putting in extra time and effort to better yourself on the job but keep getting passed over again and again for a promotion? This is a real reason for concern.

Sure, it makes sense if the person who won the position is more qualified. However, if someone underqualified or entirely undeserving gets that promotion, maybe it’s time to pack up and go somewhere else where your skills are better valued.

#4: Feeling unappreciated and stagnant

Image Credits: Human Resource

Working with a management team who doesn’t appreciate your presence or contributions is dangerous for your overall sense of self-confidence. Simply put, you deserve to work at a place that takes you seriously.

Also, peeps who think they have stayed too long and become stagnant in their learning curve should rethink their position. A job is not all about money. It’s also about growth opportunities. It’s your chance to be a better administrator, consultant, or marketer (for example) than you were when you first started.

#5: Continually running on the work treadmill

From dawn to midnight and from Monday to Friday, work may constantly be plaguing you. Maybe it’s the worry or stress over deadlines, or perhaps it could just be the general fear of it overhanging you.

But if it’s always on your mind, even on rest days, it’s probably time for a change. Folks who find themselves venting about it endlessly to their loved ones should also take this as a warning sign.

After all, work is just work and shouldn’t invade your personal life to such an unhealthy extent.

Final thoughts

Image Credits: Monster Jobs

Deciding to quit your job is often very challenging, indeed. It can be even scarier for those who’ve been with the company for long enough to feel too “okay” to move.

However, if you think about it, having a job that fulfils you and makes you feel treasured has a more prominent part to play in retaining you for the road ahead. Well, sleep on it and make the decision when you’re ready.

An excellent way to get started is to begin browsing for job openings and sending resumes. When a suitable role presents itself, and you’re offered a contract, then you know it’s the right time to send in that long-awaited resignation email.

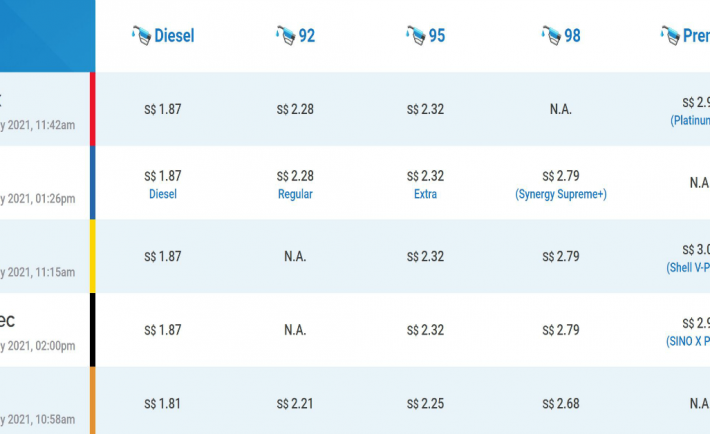

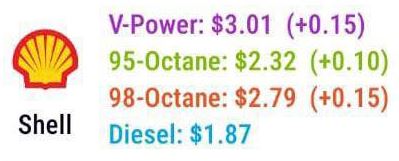

Petrol pump prices have gone up after the Government has announced the hike of petrol duty rates on Tuesday (Feb 16).

The hike, which took immediate effect, has cause pump price to rise to what they were before the circuit breaker.

The duty for premium grade (98-octane and above) petrol will be raised by 15 cents a litre to 79 cents a litre and the duty for intermediate grade (92-octane and 95-octane) petrol will be raised by 10 cents a litre to 66 cents a litre.

This means that the most popular 95-octane petrol is now retailing at S$2.32 a litre at all stations, except SPC which charges a litre at S$2.25. The hike also see Shell V-Power tops at S$3.01 per litre.

Here are the latest fuel prices according to fuel price tracker Fuel Kaki.

Tesla is one of the most innovative companies out there, aiming to transition the world’s energy sources to renewable energy. One of its primary ways of doing so is through its iconic electric cars.

By owning one of these powerful vehicles, you no longer have to pay for petrol. Instead, you can charge your Tesla cars at charging stations wherever you go, just as you would power up your phone or electronic devices.

Here are the main features you need to know about the energy-efficient car if you’re planning to hit the road with a custom online order soon.

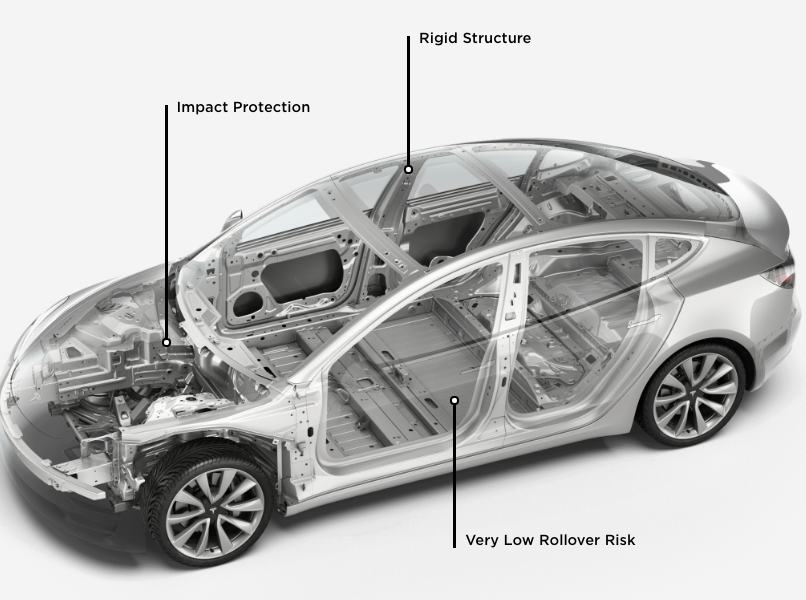

Built for safety

When you think of a car, safety may be one of the most critical features that come to mind. After all, your life is literally in its hands.

Thankfully, safety is an essential part of the Model 3 design. Its body and frame are made entirely out of steel and aluminium, making it the most robust metal structure yet.

The car can even withstand its weight stacked on top of itself four times, even with a glass roof! That’s the same as having two adult African elephants on top of your roof. Impressive, isn’t it?

Ultra-fast acceleration

To get to the places you want to go, you’re going to need the quickest acceleration possible. Model 3 can exceed your expectations by climbing from 0 to 100 km per hour in little as 3.3 seconds.

That’s all thanks to the option of a dual-motor all-wheel drive, and 20” Uberturbine Wheels and Performance Brakes that have lowered suspension. They give you complete control, no matter the weather condition.

Dual motor

The motor for the Tesla Model 3 is quite different from your average gas-powered car. It has two engines that run independently from each other, which provide better redundancy in just one moving part.

That also means it offers minimised maintenance needs, all while providing the most durability for your buck. Plus, the dual-motor lets you harness the power of complete flexibility when it comes to manoeuvring your car front and rear wheels for better traction and handling.

Range

Image Credits: The Straits Times

Because the Model 3 is fully electric, you can drive without worrying about stopping at a petrol station. Just by charging overnight, you’ll be set with a full battery every day.

But what if you’re growing old or simply absentminded? Fret not. Thirty minutes is all you need to charge for your vehicle to run for a 270 km distance.

With over 20,000 Superchargers across the world and more opening every week, convenience is just around the corner. Tesla drivers can look forward to more Supercharger locations on our sunny island in time to come.

Autopilot

The Tesla Model 3 not only brings you places but brings the future right before your eyes in the form of autopilot.

When stretches of roads make driving tedious, switching on autopilot will offer you advanced features such as twelve ultrasonic sensors to help you along the way.

Other features worth noting include the navigating guidance from highway on-ramp to off-ramp, single-touch auto parking, and automatic lane changes while on the highway.

Stunning interior

Forget what you know about your regular car. Get ready to step into a whole new interior with your Model 3.

Instead of carrying around a key, consider your smartphone the new replacement and controller hub for all the driver controls you need to work, together with the 15-inch touchscreen. The sleek modern interior also features an all-glass roof, which lets the sunlight in for a brighter and better drive experience.

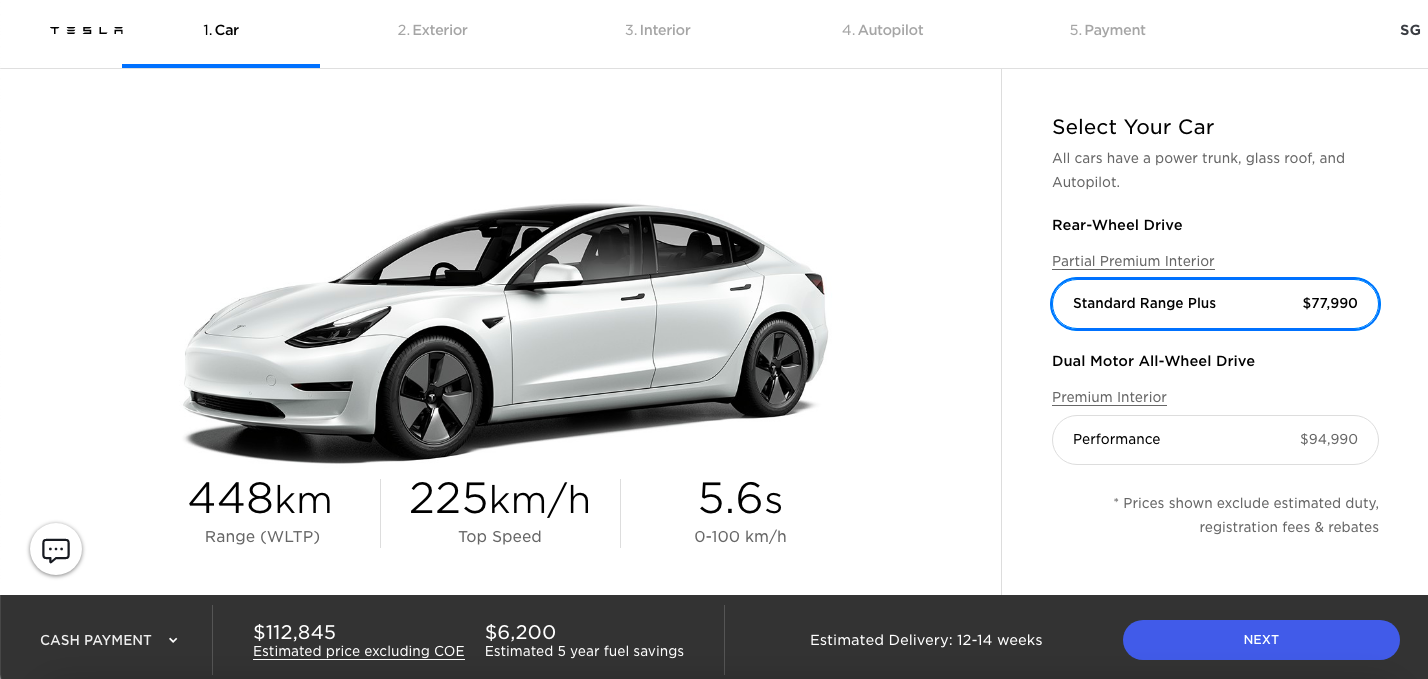

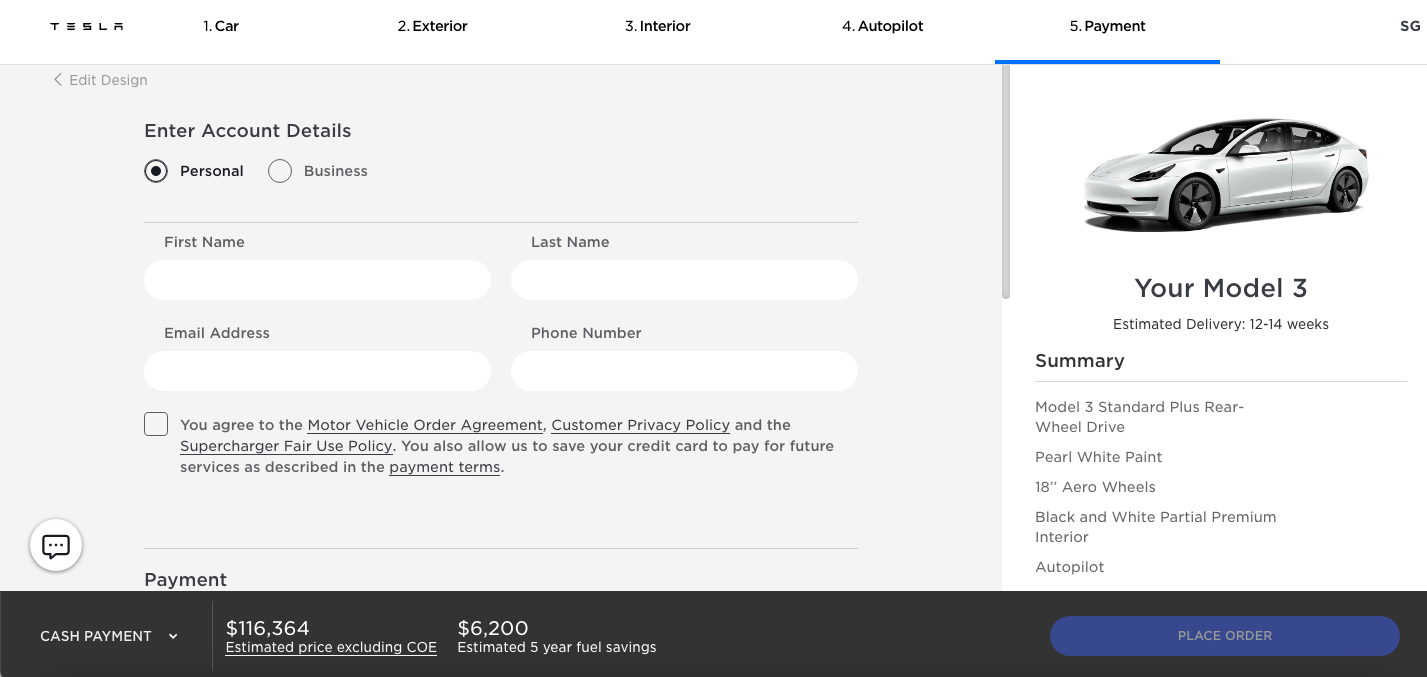

Step 1: Partial Premium Interior vs Premium Interior

Take your pick from a Partial Premium Interior or Premium Interior. The latter will raise the cost to S$154,815 from S$112,845 (excluding COE).

However, the extra S$40,000+ you pay is not just for the interior. It also affects the performance in terms of the range (WLTP), top speed, and acceleration power.

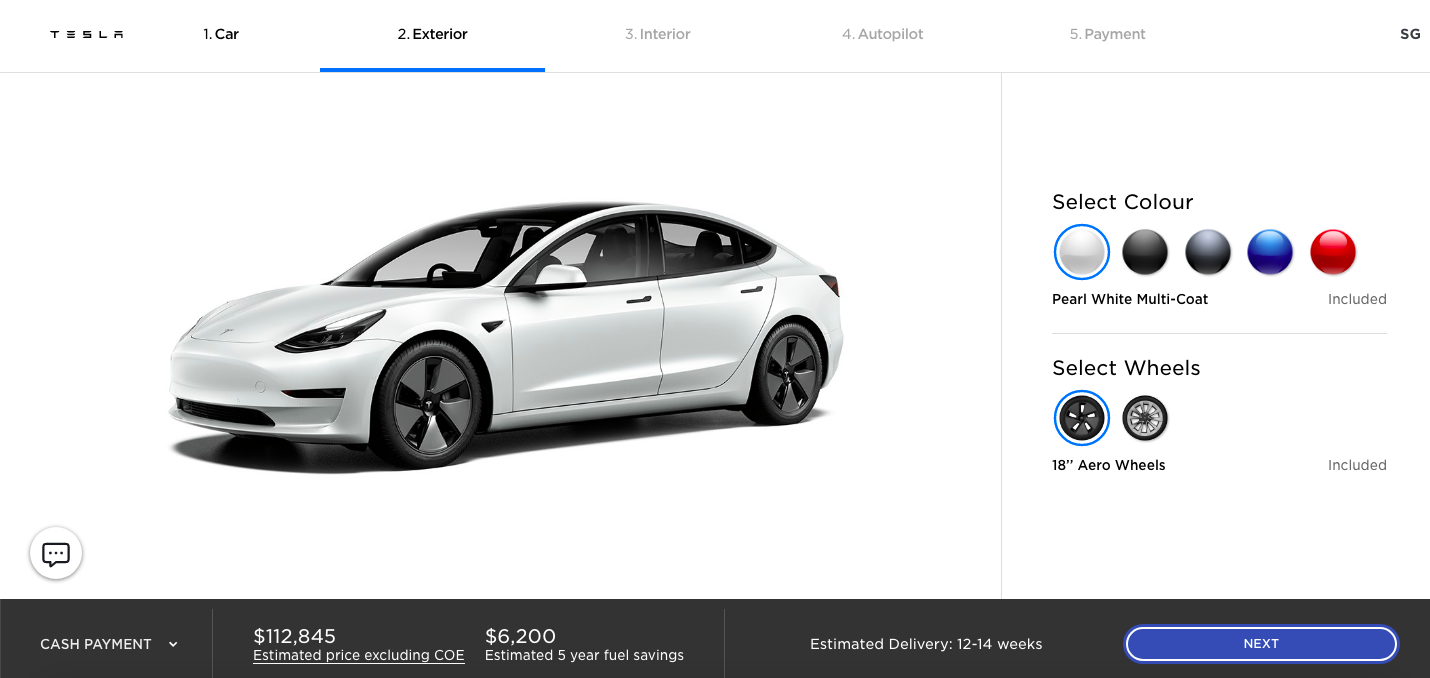

Step 2: Colour & Wheels

Now, it’s time to put on some “clothes” for your Tesla Model 3. Take the default in pearl white multi-coat and 18’’ aero wheels, and there will be no extra charges.

Or you can also choose to have it in solid black, midnight silver metallic, or deep blue metallic for an extra S$1,500. A bright red multi-coat will cost you S$3,000. Next, you have the choice to upgrade to a set of 19’’ sport wheels for S$2,000.

Take some time to think it through before you proceed.

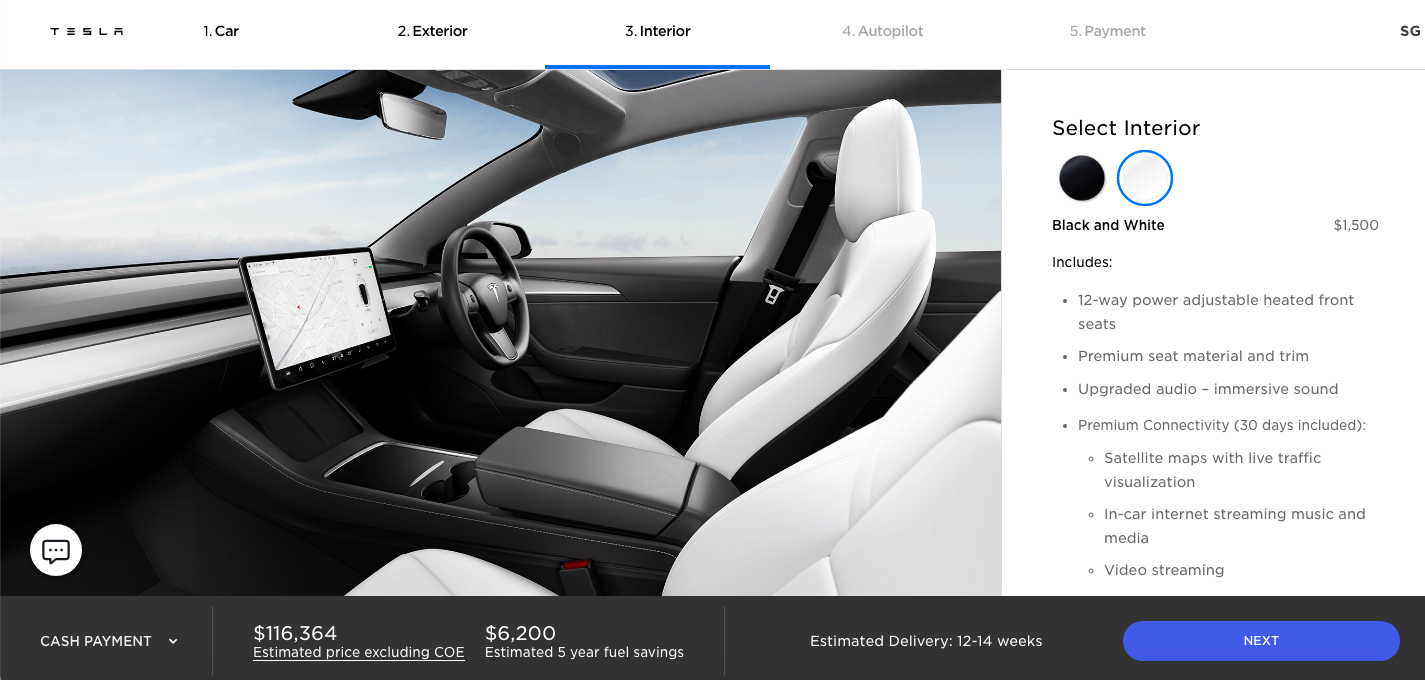

Step 3: Black vs Monochrome

By now, you should know that when you’re given the freedom to customise, it often comes with extra money. How would you like your interior? Stick with black if you don’t want to fork out another dollar. Or you can go for black & white by paying S$1,500.

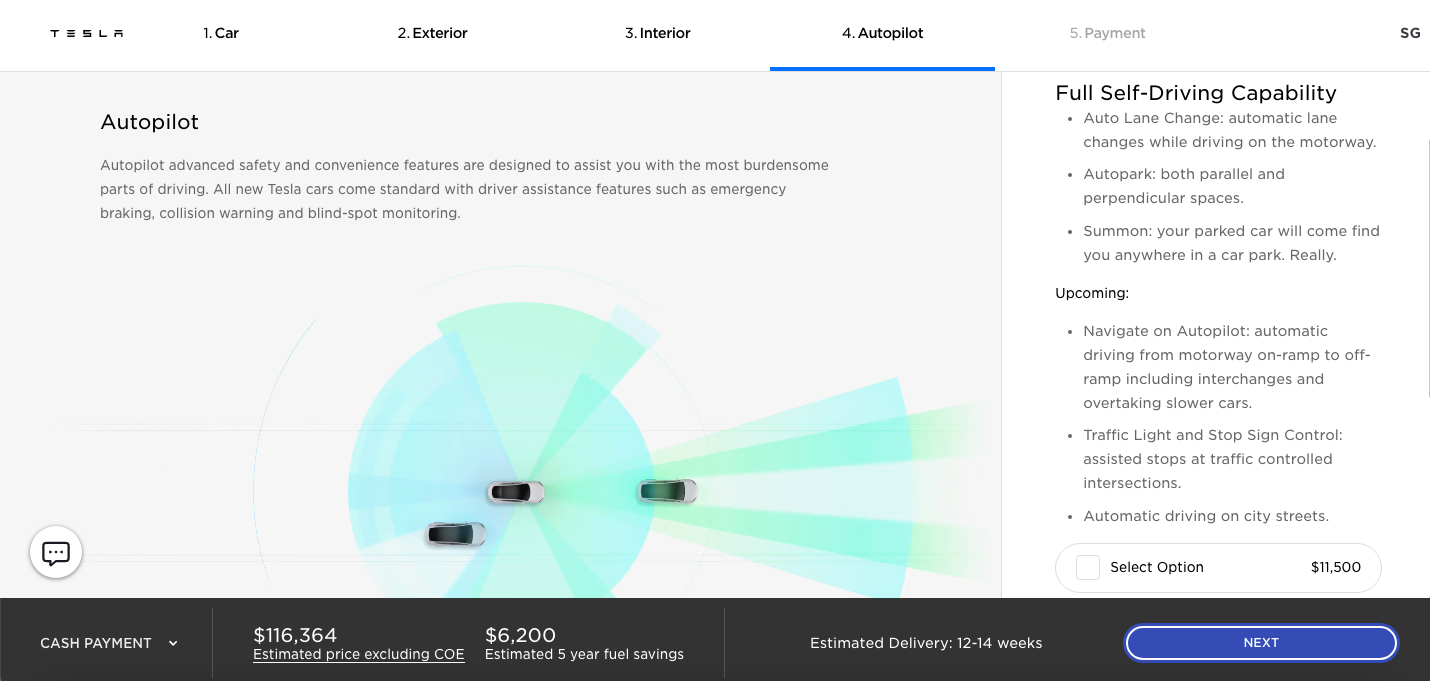

Step 4: Autopilot

We’re almost done! This is the second last step to the payment page.

Those who want the most advanced safety and convenience features must be willing to pay S$11,500. The good news is that you can skip this now and choose to buy post-delivery. Just be mindful that with new features rolled out by Tesla in the future, prices may rise accordingly too.

Step 5: Payment

Congratulations on getting to this last page. Here, you just have to enter your account details, card, and billing information before placing an order. There is also a one-time S$150 non-refundable order fee to be charged.

Placed an order? Great! Now, sit back and relax. Your customised Tesla Model 3 will reach you in about 12 to 14 weeks. Click here to view a comprehensive list of FAQs and happy waiting!

In Singapore, there’s always a constant strive to earn more money.

It’s perfectly understandable considering how high goods and services are priced, and how we want to provide a better future for our family.

Some of us take the next step by preserving our wealth and future income through the use of different types of insurance.

But only a few go even further to make it all fool-proof with estate planning.

What is estate planning all about? And what are some of the easy things we can do right now?

Let’s find out.

What Is Estate Planning?

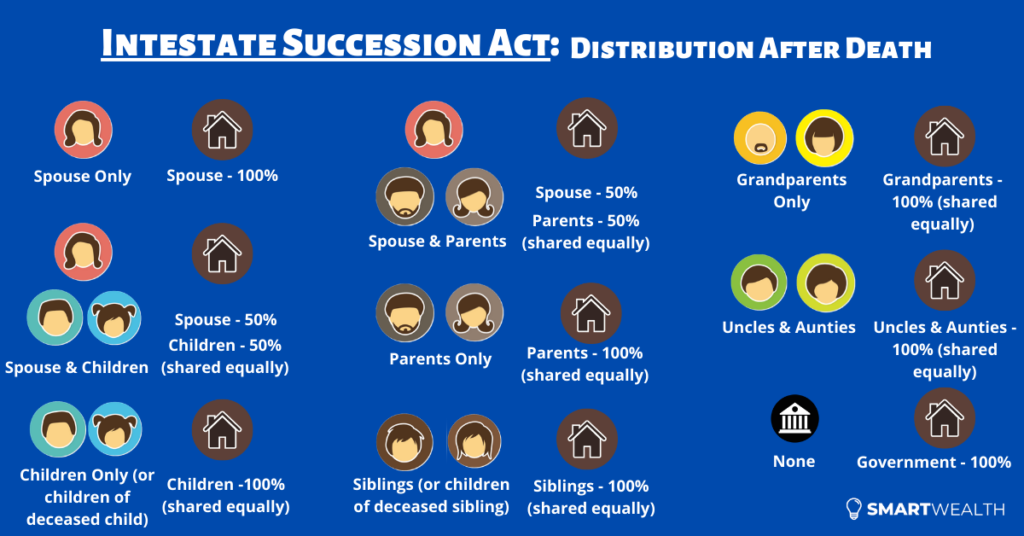

When death happens, all your eligible assets (e.g properties, money in the bank account, investments, insurance) will form your estate which will be distributed according to prior instructions (if any).

The purpose of estate planning (which can only be done before death) is to decide how your estate is going to be distributed upon the inevitable.

This distribution is indicated with the use of several legal documents.

All these ensure that the wealth you’ve accumulated thus far will go to the intended beneficiaries (people/entities who’ll be receiving your assets), in a timely and efficient manner.

Why Should You Care?

We tend to focus on wealth accumulation (savings and investments) and wealth preservation (insurance).

But a lot less on wealth distribution (estate planning), which is equally important in the grand scheme of things.

Firstly, the process of unlocking assets will be more tedious and complex. This inevitably prolongs the time for beneficiaries to receive proceeds. If the family depends on timely money coming in, this issue will be more dire. Who’s going to provide them with liquidity to pay off current bills and expenses?

Secondly, also because of the complex and lengthy process, it’ll cost more.

And lastly, most of the proceeds will go according to the intestate succession act or the Muslim law.

Therefore, your assets may not go to the intended people. And even if they do, not in the correct allocation that you wish for.

For example, if your spouse, children and parents are still living, your assets will be distributed to your spouse and children only, and none goes to your parents (even if they raised you up since young).

And it could also go to the unintended people.

For example, if your spouse and children are still living, and you think that your spouse doesn’t deserve anything, distribution will still go to your spouse.

These will cause ugly disputes amongst family members because there’s no clear and distinct indication of WHO should receive WHAT.

Furthermore, when you’re not around anymore, there’s no one else to turn to except for any legal documents you leave behind.

But when you employ even the simplest of estate planning tools, you effectively eliminate all these potential problems.

What are some of them?

3 Core Estate Planning Tools in Singapore

When dealing with financial matters, there’s always some resistance in taking action.

For example, people always want to find out what’s the best investment before investing, which is perfectly fine. But a problem that comes out from that is that too much information paralyses them and nothing is done in the end.

It’s also the same with estate planning.

But I can assure you that setting up these 3 tools will have the most impact and take the least amount of effort.

1) CPF Nomination

If you’re a Singapore Citizen or a Permanent Resident, you will have CPF accounts – Ordinary, Special, MediSave, Retirement.

If you don’t make a CPF nomination, and death happens, distribution of CPF savings will take a longer time, higher costs and goes by the law.

So you’d always want to get it done. It’s free anyway.

But most see it as a hassle because it used to be done via hardcopy forms (with 2 witnesses) or by going to the CPF service centres.

However, back in 2020, CPF allowed the nomination to be done online, and this made the application easy and convenient. While you still need 2 witnesses, the entire process is done electronically. If you want a step-by-step guide, you can check out how to make a CPF nomination online.

Even if a nomination is made, you can easily change it in the future. It’s usually done by submitting a new one, and that will override the existing nomination.

2) Insurance Policy Nomination

If you’ve bought life insurance and think nothing else needs to be done, think again.

The second part is to make a nomination where you can specify who will receive the proceeds and in what percentage.

Nominations can be made on life insurance policies with a death benefit. Take note that nominations can only be done on private individual policies and not on company/group insurance – they’re not owned by you.

There are 2 types of nominations: revocable and irrevocable (trust). Most choose the former as the nomination can be changed easily in the future.

Although it isn’t compulsory, it’ll be useful.

This is because by nominating, the insurance company can pay out directly to the beneficiaries when there’s an eligible claim. This effectively bypasses the usual probate process, saving time and money.

But here’s a trick question: do you want to nominate all your insurance policies?

The answer: it depends.

If your proceeds are large and all your policies are nominated, it’ll mean that your beneficiaries will receive the proceeds all at once.

Will they be able to handle such amounts?

There are many cases where the beneficiaries mishandle monies, and in the end, it got them into further trouble.

So if your proceeds aren’t that much (which you should have it reviewed), then it wouldn’t matter all too much.

But if it amounts to a bigger sum, you can make nominations on a few policies just for liquidity purposes. The rest can still be specified in a Will to pay out on a staggered or monthly basis.

To make a nomination, you can download the relevant forms from the insurance company, fill it out properly and sign in the presence of 2 witnesses. Or you can approach your financial consultant to help you with it.

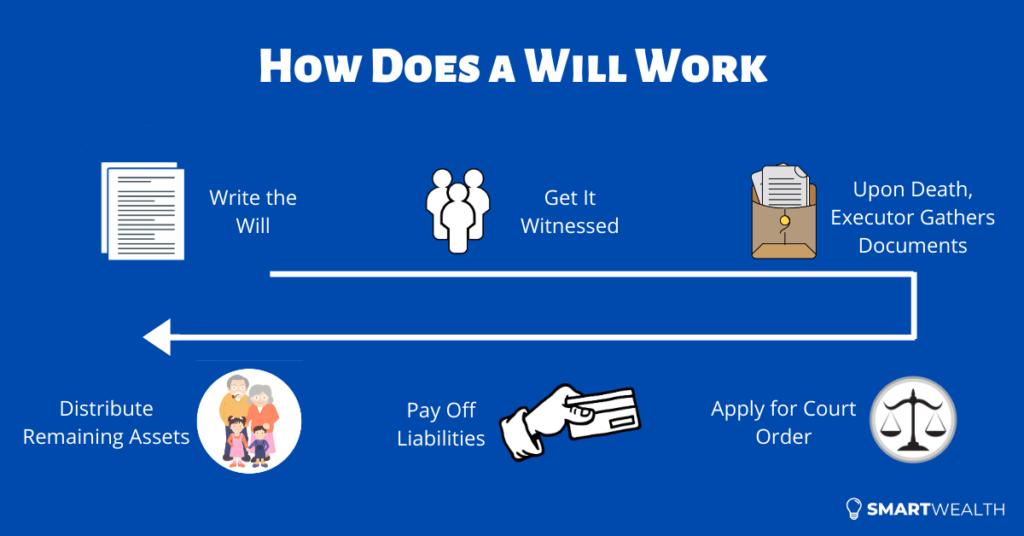

3) Writing a Will

Even when you’ve done the CPF and insurance policy nominations, some assets will still be left out.

Examples:

Money in the bank account

Investments over several platforms

Properties (depending on the ownership type)

etc

If you don’t make a Will, all these will still be distributed according to the intestate law or the Muslim law.

Other than the usual benefits of writing a Will, you can also use it to appoint a guardian to take care of young children and create a testamentary trust to stagger payouts.

Just know that getting a professional to write a Will only costs a few hundred dollars.

The obvious advantage is convenience but more importantly, the Will is drafted to be able to stand in court if challenged.

Other Points to Take Note Of

Apart from the 3 basic tools mentioned above, there are other aspects you should know also.

Firstly, setting up trusts can give you greater control.

Although the Will covers most needs, the trust will bring estate planning to the highest level.

These benefits include:

can be created when you’re living

provide for a special needs child

utmost confidentiality

delaying gifts to beneficiaries

etc

While higher net-worth individuals derive more value from it, there are affordable trusts out there that can suit the needs of the masses.

Secondly, a distant cousin to estate planning is advance care planning.

Have you thought of what happens when you’re neither “dead” nor “alive”? In other words, mentally incapacitated.

You can’t do anything about your finances. And estate planning doesn’t kick in.

That’s when advance care planning comes in. It also involves different tools such as the Lasting Power of Attorney and the Advance Medical Directive.

These are important because it will specify what happens next when certain situations come up.

For example, when an Advance Medical Directive is done up, you specify that you don’t wish to be on life support to artificially prolong your life.

And for the last point, you need to have wealth.

You see, if you don’t have any wealth (your liabilities are higher than assets), there’s nothing to distribute even if you’ve done estate planning properly. Even if you’re mentally incapacitated, there may not be money to even pay for your medical expenses.

That’s why, financial planning (wealth accumulation and insurance protection), estate planning and advance care planning, all have a part to play in the bigger picture.

If one is missing, your financial plan is not wearing its full suit of armour. And when a battle comes, damages will be done.

What’s Next?

Estate planning is often in the back seat.

But at times, you have to bring it to the forefront.

That means either to set up the tools or to review them.

So take small steps by looking at the 3 basic ones first – CPF Nomination, Insurance Policy Nomination, and Writing a Will.

And then explore other areas when you’re ready.

About the Author:

Abram Lim runs SmartWealth which covers topics on personal finance – insurance, savings, investments, retirement planning, etc. It strives to produce research-backed articles so that readers can make better financial decisions with objectivity.