The story goes something like that. In 1989, Mr Sulistio and his wife Soemiati purchased gold bars using their joint account at the United Overseas Bank in Singapore.

At first, the couples kept the gold bars under both their names. But Mr Sulistio, now 87, signed documents to pass possession to his wife in 2016. In 2017, she passed away. He later learned that she had willed the gold bars to four of their five children.

Sued his children following an unsuccessful challenge to the will

Image Credits: The Australian

He sued the four after a failed appeal to her will in Hong Kong. The signing of the documents did not modify the original intention to preserve the gold bars as joint possessions, Mr Sulistio said.

He asserted that he was the rightful owner of the gold bars, as the sole survivor. But Justice Valerie Thean rejected his claims.

The judge claimed in a written decision that there was no doubt that the pair originally had a collective goal of possessing the gold bars for their mutual good. However, she noticed that there was enough convincing evidence of a shift in their aim in 2016.

Signing of certificates as part of a wider agreement

Justice Thean discovered that as a component of a larger deal between the pair, Mr Sulistio endorsed the documents. It turns out that Madam Soemiati had requested for the gold bars in return for having their son Rudy to handle their Indonesian territory.

Mr Rudy was left out of the will of Madam Soemiati and came to the defence of his father in the lawsuit.

According to the judge, Madam Soemiati wanted to possess the gold bars for her interests. That is, if she were to pass on without using the gold bars, she would like to favour the defendants.

The couple’s marriage broke down in 2012

Image Credits: The Wedding Vow

In the 1950s, Mr Sulistio and Madam Soemiati were married and had three daughters and two sons. They stayed in Hong Kong as a couple.

Their daughters said their parents’ relationship deteriorated in 2012. It was partly because of the strained relationship between Madam Soemiati and Mr Sulistio’s nurse. Their eldest daughter suggested that Madam Soemiati was disappointed that the nurse bullied her, but Mr Sulistio did little to rectify the issue.

An attempt to guarantee her financial security

The court acknowledged the defendants’ allegation that the gold bars’ legal movement was part of an arrangement under which Madam Soemiati sought to ensure her financial stability.

Madam Soemiati, who was severely ill with increasing medical costs, was worried that her savings were depleted. This was due to vast amounts of money moved from joint accounts with her spouse to Mr Rudy.

Mr Rudy also did not dispute the acquisition of roughly US$7.2 million (S$9.5 million) between 2010 and 2016. Furthermore, according to the verdict, at least US$1 million remains unsubstantiated for.

Several consumer-facing Financial Technology (FinTech) companies, from digital payments to insurance and transfer payments, have arisen to support Singaporeans’ personal finances. You may have heard of robo-adviser companies such as StashAway, Syfe, and AutoWealth that help with investments.

What are robo-advisers?

To optimise investment portfolios according to the risk profile of the customer, Robo-advisers rely on algorithms. In reaction to market changes, portfolio readjustment is performed automatically.

As such, there is little need for active monitoring by the investor with all these automatic features. As seen from various posts and comment threads on local financial platforms, the low fees paid in relation to human investment advisors have further raised interest in robo-advisers.

A Statista study forecasts that assets under watch by local robo-advisers and user numbers are estimated to rise by over 50 per cent in 2021 to hit US$1.06 billion and 105,000 users accordingly.

Robo-advisers help break barriers to entry

Image Credits: Freepik

The perceived difficulty of gaining financial expertise and the scarcity of time for investment and fund management are two widely quoted reasons for not investing.

With technology assistance, robo-advisers eliminate these hurdles, making them a fantastic way to kickstart investing, particularly for beginners. This is not to mention that the procedure of signing-up is reasonably straightforward.

In 15 minutes, a profile can be registered. To propose an appropriate portfolio concerning the investor’s financial targets and risk aversion, one only needs to answer some preliminary questions.

Standard considerations include age, gender, marital status, salary, investment horizon, and priorities, such as funding for a house versus retirement planning. At the same time, risk evaluation focuses on experience with multiple financial instruments and gain and loss perception.

Once that is in place, algorithms based on current financial models will handle the portfolio. Easy peasy, isn’t it?

Advantages of using robo-advisers

The isolation of feelings from investing using robo-advisers is a gain. Investors are far less likely to respond irrationally to disruptive market developments and exit from the market out of panic, with investments using advanced automated trading.

Robo-advisers often foster healthy financial habits by encouraging clients to add to their investments on a routine basis. This induces investors to take advantage of the dollar-cost averaging (DCA), which has been proven to be a successful method for allowing the long-term accumulation of capital by novice investors.

A look at the downsides

Image Credits: fa.com.sg

No one thing in the world is perfect, and this applies to robo-advisers too. Given their emphasis on ease and effectiveness, robo-advisers cannot make investment decisions precisely personalised to each user’s financial condition.

Instead, they enable clients to pick from pre-selected portfolios from a restricted menu. They deal only with personal finance’s investment facets and miss the human touch of actual financial advisors.

Human financial planners devote much more time to identifying the needs of their customers. Thus, they can provide numerous solutions that cover various holistic financial management elements, including savings and coverage.

Is investor passivity harmful?

The low percentage of investor participation needed is one of the principal selling points of robo-advisers. But is the lack of investor involvement a cause for concern?

Investor indifference may foster a laid-back approach towards other areas of financial planning. Since computers and algorithms can assign this seemingly cumbersome task, this may lead to a refusal to gain financial expertise going forward.

Although robo-advisers cater to tech-savvy, passive, and limited-capital investors, automated investment does not appeal to active investors. This is especially so for those who want to have portfolio ownership and may be dissatisfied with having a bot controlling their assets entirely.

According to an HSBC survey done last June, only one-quarter of Singaporeans had used mobile banking to invest. This hesitation in handling digital capital shows the real lack of investment expertise or trust. It also highlights the need to empower Singaporeans with financial knowledge.

Lack of financial knowledge can be devastating

Image Credits: City Nomads

Dr Gordon Tan Kuo Siong, Faculty Early Career Award Fellow at the Singapore University of Technology and Design, shared how a lack of financial knowledge can be devastating.

Using the story of Alex Kearns, he brings out the importance of financial literacy. Last June, the news reported the death of the 20-year-old trader by suicide. After Kearns mistakenly thought he lost hundreds of thousands of dollars on Robinhood, a free-trading app, he took his own life.

For sound investment and financial planning, the acquisition of knowledge is necessary. As the term “caveat emptor” indicates, consumers’ ultimate responsibility is to perform proper research when making a transaction. Buyers should request information on the details of the items they purchase.

In short, consumers should arm themselves with the information they need on the investment products that robo-advisors suggest. As for the businesses who promote these services, it is vital to ensure adequate resources on how their products operate.

Some deets on local robo-advisers

Several local robo-advisers have also launched educational initiatives to develop more educated investors. A set of courses covering personal finance and trading on its app, as well as frequent newsletters and market insights, have been made freely available by StashAway.

Syfe posts short articles and conducts online seminars to provide the public with financial information. These programs are praiseworthy and should not be treated as unnecessary supplements.

In conclusion, if robo-advisers boost their customers’ financial literacy and consumers make an effort to consider what they are investing into, buyers will have much more interest in creating machine-enhanced financial decisions and endow their money to a robot.

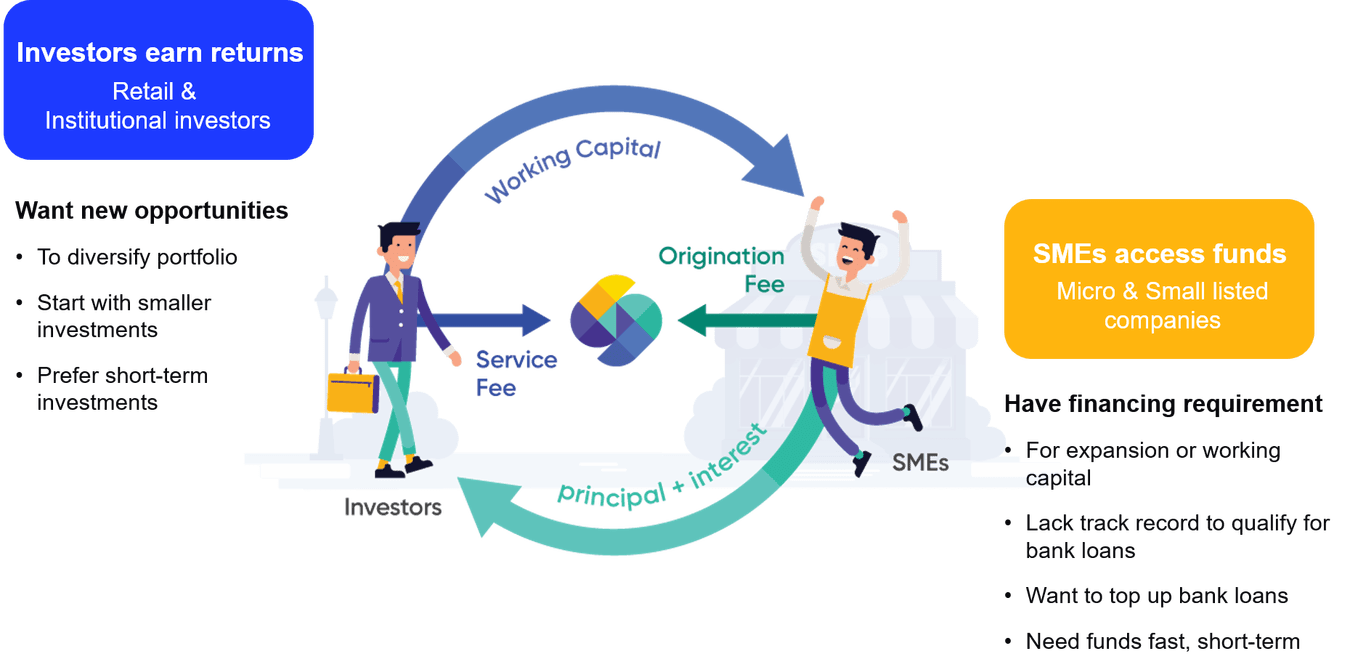

P2P investments or more commonly known as Peer-to-Peer (P2P) lending is a type of debt-based crowdfunding enabled by digital platforms that connect borrowers with investors without going through a traditional financial intermediary such as a bank. This concept will see investors lending to borrowers (i.e. SMEs) via the platform as a form of investment, and the interest earned from it will be their returns. Despite being a relatively new concept in Singapore, it has grown significantly over the years and has shown no signs of slowing down.

How does P2P investment work for investors?

For investors, it is a means for diversification into another asset class. As most P2P investments offer a frequent repayment schedule (monthly or within 90-120 days period), it can be considered a great supplement to more traditional long term asset classes like stocks or bonds. With interest rates on saving accounts heading south, investors can look for alternative ways to earn interest on their cash.

How much can investors earn?

Be it an individual or institutional investor, the reward on their investment will come in the form of the interest payments serviced by the borrower. At Funding Societies, investors can choose to participate across 6 different investment products with interest rates ranging from 3% – 18% per annum.

Risks and returns go hand-in-hand and the difference in interest rates range is tied to the risk associated with the product. For example, a guaranteed returns investment will yield an interest of between 3% – 5% p.a. while an unsecured business term investment can fetch between 8% – 18% p.a..

How much to invest in P2P investment?

There are no hard and fast rules on how much of one’s portfolio should be allocated to any particular investment assets, and this is the same for P2P investing. What is important is that investors should always consider diversifying across many notes and avoid concentration risk to create a healthy well balanced portfolio.

At Funding Societies, investments start from S$20 onwards and most products provide a periodic repayment of principal and interest. Jointly, it is a great recipe for investors to diversify and reinvest their investments.

P2P investment with Funding Societies

Funding Societies is Southeast Asia’s largest P2P lending platform with over S$1.7b in SME financing funded. In Singapore, the platform holds a Capital Markets Services (CMS) Licence and is regulated by the local authorities. Over the years, they have been able to raise several rounds of equity funding led by investors such as Sequoia India, Softbank Ventures Asia and SGInnovate to name a few. A few things to note when investing with Funding Societies:

Interest returns are exempted from tax: For interests earned in year 2020 onwards

Low barrier to entry: Investments start from $20 per note

Short tenor: Investment tenors ranges from 1 to 12 months

Returns on Investment: Interest rates usually range between 3% to 5% per annum for a Guaranteed Investment product, 6% to 8% per annum for a Property-backed investment and 8% to 18% per annum for Invoice financing and unsecured business term investments

Default Rate: The Singapore platform default rate is 1.89%

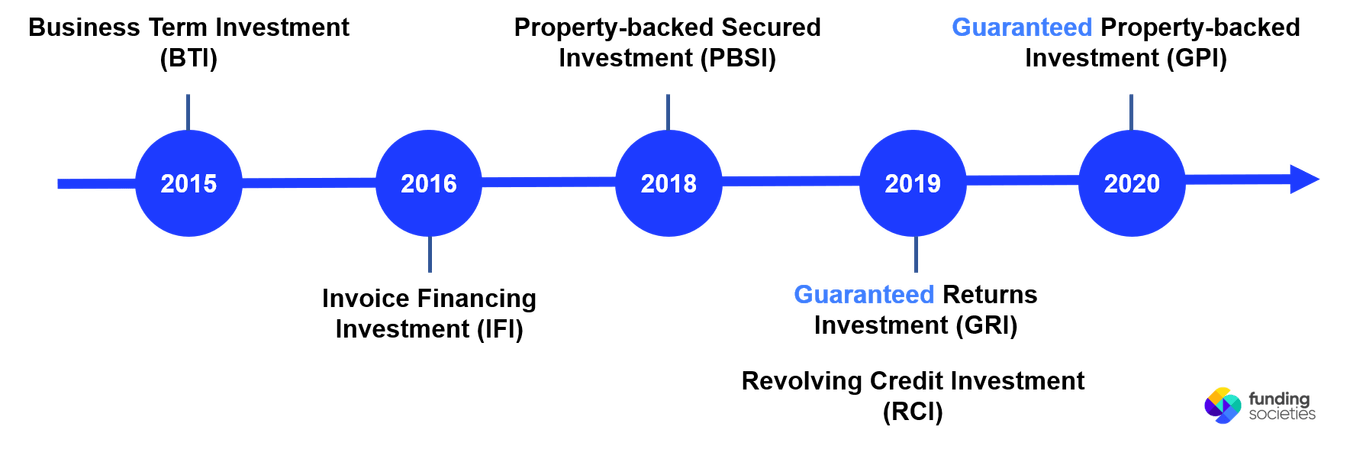

P2P investment products

As the investor base grew overtime, they needed to continuously innovate new products to meet the needs of a wider range of investor profiles. Having launched the first product back in 2015, Funding Societies has now grown to offer 6 different investment products with varying levels of risk-return profiles.

TL;DR: P2P Investment Products Overview

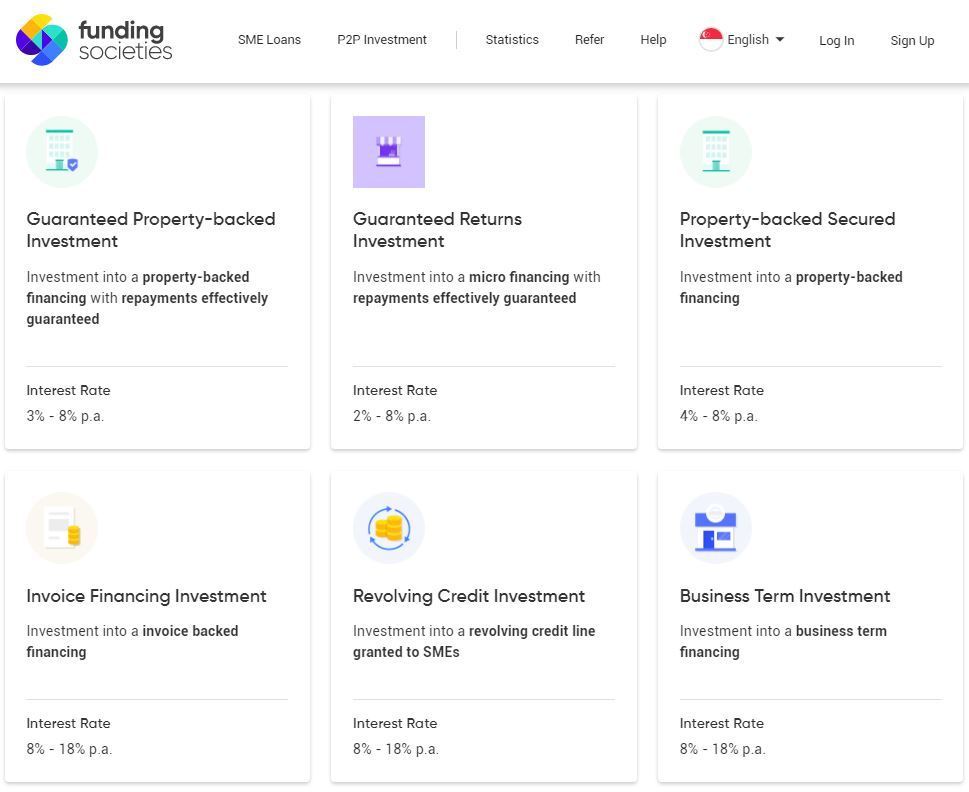

1. Property-backed Secured Investment

The Property-backed Secured Investment (PBSI) is a rather unique collateral-backed investment product launched to provide investors with an additional security in the form of a local Singapore property to back the investment. The property is pledged by the SME undertaking the financing.

Funding Societies holds first charge on the property on behalf of investors and it can be auctioned off to recover funds should the SME defaults.

To alleviate concerns on property value fluctuations, the percentage of financing amount varies as per the property types (residential/commercial/industrial) and in most cases is only up to 70% of the property value. The forced value of the property is also considered while arriving at the financing quantum. By doing so, Funding Societies maintains a buffer for fluctuation in property prices as well as for distress sale situations. The interest rate for this investment product is typically between 4% – 8% per annum.

2. Guaranteed Property-backed Investment

Launched in July 2020, Guaranteed Property-backed Investment (GPI) is an investment into a Property-backed Secured Investment with an additional effective guarantee of repayments to investors. Likewise to Property-backed Secured Investment, Funding Societies has the right to liquidate the property to recover the funds should the SME fail to fulfil their obligations.

Falling under the Guaranteed line of products means that both the principal & interest repayments are effectively guaranteed to the investor regardless of the SME’s status. The interest rate for this investment product is typically between 3% – 8% per annum.

3. Guaranteed Returns Investment

Guaranteed Returns Investment (GRI) is another investment product under the Guaranteed line of products. This product was first launched in August 2019 as a means to offer more investment opportunities to investors.

GRI is an investment into a micro financing with repayments effectively guaranteed. Similar to GPI, investors are effectively guaranteed to receive both the principal & interest repayments when they participate in this investment product. The interest rate for this investment product is typically between 3% – 5% per annum.

Please invest with the knowledge that while returns are effectively guaranteed by FS Capital Pte. Ltd., there may be a chance where we might not be able to fulfil the obligations under this arrangement. To mitigate this risk, a cash reserve buffer to allow for repayments to be made on time is maintained.

4. Invoice Financing Investment

The Invoice Financing Investment (IFI) product allows investors to invest into an invoice backed financing offered to SMEs. SMEs take this financing by pledging against the receivables of an invoice. By doing so, it helps to bridge the cash flow gap between actual sales and receipt of payments.

Due to the nature of the financing, investors in this product usually enjoy a relatively short tenor of 30 – 120 days. The short tenor enables investors to receive and reinvest their money relatively quickly. The interest rate for this investment product is typically between 8% – 18% per annum.

5. Revolving Credit Investment

If you own a credit card, you will probably be aware of how revolving credit or more commonly known as a line of credit works. Based on one’s credit standing, they will be issued a credit limit to draw down from over time. Likewise in the case of Revolving Credit Investment (RCI), it is an investment into a revolving credit line granted to SMEs. The SME can repay anytime within the approved tenor and draw down again so long as the amount outstanding is within the limit.

As an investor, you can participate in a single or multiple drawdowns, each with a tenor typically between 1 to 12 months with a chance of early partial or full repayments. The interest rate for this investment product is typically between 8% – 18% per annum.

6. Business Term Investment

Business Term Investment (BTI) was the first product offered alongside the launch of the Funding Societies platform back in 2015. It is an unsecured financing undertaken by SMEs as a means for working capital, expansion or bridging needs. The interest rate for this investment product is typically between 8% – 18% per annum.

Be it a way to diversify your investment portfolio or to beat the falling savings account interest rates, investors can consider to embark on their P2P investment journey with a platform like Funding Societies. If you have done your own due diligence and decided to invest with Funding Societies, they currently have a promotion for new investors. Sign up with promo code MDXMAS20 and make a total investment of S$200 by 31st Jan 2021 to get a S$20 cashback.

Terms and Conditions apply

Investors must sign up with the aforementioned promo code and make a total investment of at least S$200 by 31st Jan 2021 to be eligible for the $20 cashback. Cashback will be credited into the eligible investors’ accounts by the end of February 2021. Funding Societies’ investor T&Cs apply.

Funding Societies is the largest SME digital financing platform in Southeast Asia. It is licensed in Singapore, Indonesia and Malaysia, and backed by Sequoia India, Softbank Ventures Asia Corp and SGInnovate amongst many others. It provides business financing to small and medium-sized enterprises (SMEs), which is crowdfunded by individual and institutional investors. Investors can invest from as low as S$20 with a tenor of no more than 12 months. Depending on the investment product, interest rates can range between 2% to 18% per annum.

It is Christmastime and people are more eager to purchase gifts that have lasting value. For some people, that timeless gift often turns out to be an heirloom piece of jewelry. Grandparents often pass down their jewelry in the hopes that their grandchildren can “sell it one day” when the need arises. I cannot say that it has not crossed my mind. Then again, I find it difficult to sell the ring that my late grandparents have given me.

Buying an original piece of jewelry with a rich history from a family member or a friend can be the middle ground when it comes to heirloom pieces. Nonetheless, jewelry and gold can be a wise investment.

BUY SOMETHING TIMELESS

If you are going to buy jewelry as an investment, ensure that it is something you enjoy keeping and wearing. I recently bought a Nina Ricci necklace, which I plan to pass down to my future daughter. It is delicate, romantic, and simple. She may not be able to sell it, but it can be a part of her beautiful collection.

Avoid overpaying for a piece of jewelry as commissions and fees can be high. It will be difficult for you to break-even, if that happens.

CONSIDER THE VALUE AND PRICE

There are companies willing to buy back your jewelry at the real-time value, less its 10% buyback fee as they will melt it and transform it into a new jewelry. Other companies are willing to offer a price close to the value of the pure metal in your jewelry. Do your research.

There are laws regulating the purity stamp on the metal. It is best to get an appraisal from a reputable jeweler to examine the quality and the design of your gems and precious metals.

ACKNOWLEDGE THE POSITIVE HISTORICAL TREND

Unlike coins and paper currency, gold has managed to increase its value over time. Its price has consistently risen every year since 2001. While gold prices do not shoot up dramatically, the general trends remains to be upward. Hence, have a long-term investment mindset.

KNOW THAT PRICES CAN BE VOLATILE

Much like any other investments, the jewelry’s value can fluctuate wildly. The most obvious difference between a pair of gold earrings and gold bullion is that you cannot wear the latter. Treating jewelry as an investment can get tricky. Profits on the sale of gold and jewelry are taxed.

You might pay a premium for buying jewelry made of pure gold. You see, some buyers prefer if they can wear their gold.

DIVERSIFY YOUR PORTFOLIO

The key to diversification is to find investments that do not closely match each other. History has proven that gold is negatively correlated with stocks and other investment instruments. For instance, stocks boomed in the 1990s, but gold faltered. In 2008, investors migrated to gold while the stocks dropped substantially in value.

Image Credits: unsplash.com

Proper diversification entails combining stocks, bonds, golds, jewelry, and other assets. Producing a diverse portfolio can reduce the overall volatility and risks.

Investing is the act of allocating your money in the hopes that you will achieve a profit in the future. The money generated from your investments can provide income and fulfillment of long-term financial security.

Now is the ideal time to start investing! Allow me to convince you with these “6 Essential Reasons Why You Should Learn To Invest”.

#1: WORK SMARTER, NOT HARDER

Many people do not think about investments until they are well into their 20s or 30s. Although opportunities to invest may come before that, investing is not something that is automatically embraced by all. Do not panic! You can become an investor at any age.

The sooner you open an investment account, the better it will be for your financial future. Take advantage of the greatest asset of all – time. Investing while you are young gives you the chance to work smarter. Would you rather save a considerable amount of money every year or save a huge amount of money later in life? Think about that.

#2: GET MORE EARNING POTENTIAL

Investing your money allows you to grow your wealth. Most investment vehicles such as stocks and bonds offer returns on your money over the long run. The return allows your money to build over time.

The money you build can be used to create a business or expand your existing one. Many investors support entrepreneurs and contribute to the creation of new products and new jobs. The more successful entities you have backed up, the stronger your returns will be.

#3: SAVE FOR RETIREMENT

Let us face it! You need to be prepared for your retirement. You should save money for retirement as you are working. You can put your retirement savings into a portfolio of diversified assets such as real estate, precious metals, stocks, mutual funds, and bonds. As soon as you retire, you will be able to live off from the funds that you have earned.

Base your personal tolerance of risk on your age and lifestyle. You may employ greater risks to increase your chances of earning greater wealth in your younger years. Becoming more conservative with your investments as you grow older can be wise.

#4: POWER OF COMPOUND INTEREST

Learning about investments will enable you to know the power of compound interest. Compound interest allows your money to make more money for you. It pays to invest early and often. The longer your money can benefit from the power of compound interest, the higher your gains will be as time goes by.

Say you invest S$1,000 this year and you earn a 10% return on that. This means that you will end up having S$1,100. If you do not contribute anything next year, you will still make money through the compound interest. Instead of earning another S$100, you will earn S$110 because you are getting 10% from a balance of S$1,100. You will have S$1,210 by the end of next year.

#5: DIVERSIFY YOUR ASSETS

You need to diversity your assets as your investments make one part of your financial picture – not all of it. You should not keep all your money in cash, in your house, or in your car. Instead, invest in a variety of categories to cushion unforeseen losses. It makes more financial sense to keep your emergency fund, your house (real estate), your hard assets (e.g., car), and your portfolio of investments.

#6: REACH YOUR FINANCIAL GOALS

Image credits: pixabay.com

Learning how to strategically invest your money allows you to reach your financial goals. If your money is earning a higher rate of return than your savings account, you will be able to earn more money within a faster period. This return on your investments can help you reach your financial goals such as buying a car, starting your own business, or putting your children through university.