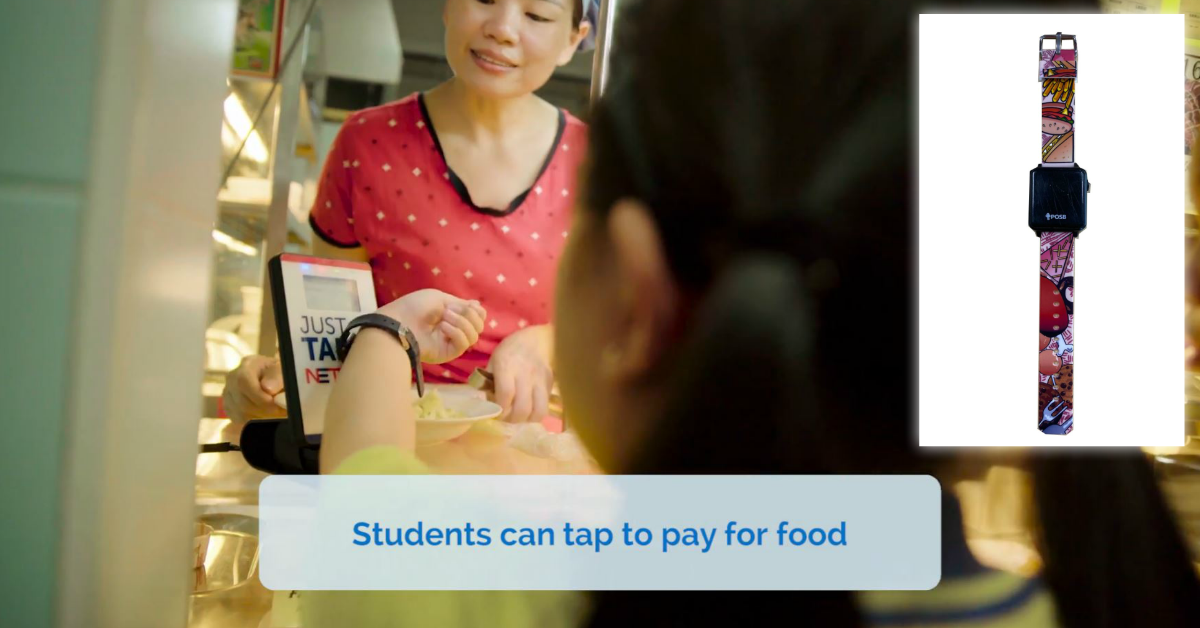

Saving is a habit that takes time to build. It’s never too early to start teaching your child the importance of saving and spending wisely. With My Account, you can keep track of how much you save and add features to meet your growing needs.

Start by opening a My Account for your child and receive a POSB Smart Buddy Watch with a Limited-Edition Strap (Worth S$45) to keep track of their daily spending.

Reward:

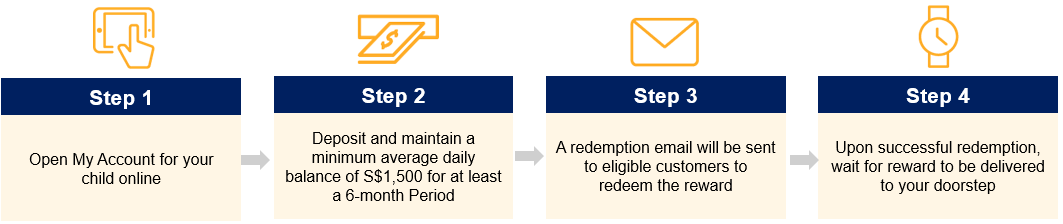

Receive a POSB Smart Buddy Watch with a Limited-Edition Strap (worth up to S$45)* when you deposit and maintain average daily of S$1,500 for a 6-month period.

*Limited to first 600 redemptions only, while stocks last.

How to be rewarded:

Promotion period is from 2 March 2021 to 30 June 2021.

Please prepare the following required documents prior to your application.

About POSB Smart Buddy

POSB Smart Buddy is the world’s first in-school savings and payments wearables on your child’s wrist. It lets your child tap to pay in school and at selected merchants, check on balances, and track fitness levels.

As a parent, enjoy greater convenience in managing your child’s finances and encourage smart living and saving habits – all with an accompanying mobile app.

Do you believe that one of the foundations of achieving wealth is saving as much money as you can? A highly effective method of building your savings is to live below your means, and we can’t emphasise that enough in our articles.

Just in case you get us wrong, this doesn’t mean taking a vow of poverty and selling all your possessions away. It just means actively monitoring your spending and watching for ways to spend less.

Spending more money than you make is a bad habit. Overspending can put you in debt, which is incompatible with your aim for financial freedom.

To better evaluate your spending, make a list of all your monthly expenses – housing, food, bills, memberships, and subscriptions – and compare it to your monthly income. If your expenditure exceeds your salary, you must find ways to increase your earnings or decrease your spending.

For freelancers with variable incomes, this can be challenging. One strategy is to calculate your average monthly payment over a rolling 12-month period and use that number to budget. You may also use a more conservative approach by taking your lowest-earning month as a baseline to account from.

#2: Budgeting based on your pre-tax income

Image Credits: wincofoam.com

Constructing your budget on your pre-tax earnings can be a huge mistake. If you’re a Singapore Citizen (SC), Singapore Permanent Resident (SPR), or a foreigner who has stayed for 183 days or more, you would be well aware of Singapore’s income tax requirements.

The more money you earn, the more you pay in taxes. This means our take-home pay is less than our hourly rate or our salary would suggest. It is, therefore, unwise to craft your budget on your pre-tax income since you do not get to keep everything you earn.

Build your budget around your take-home pay minus the taxes for a more accurate financial review.

#3: Oustanding balances on your credit accounts

Having credit cards to supplement your income can be highly attractive. However, unpaid debt on your credit lines is detrimental to your financial health.

According to some local findings, the average interest rate on a credit card on our sunny island is about 25%. If you do not pay off your credit card in full every month, the remaining balance will begin accruing interest, and this may grow out of hand if not kept in check.

Debt can increase rapidly even before you realise it. Be sure to pay off your credit balances in full at the end of each month, and if you can’t, at least go past the minimum sum required to “get by’. This is because merely making minimum payments every month is a dangerous practice.

Should you find yourself unable to do so, it means you are spending too much on credit.

#4: Having a negative net worth

Image Credits: corporatefinanceinstitute.com

Investopedia defines net worth as the value of all of your assets minus your liabilities. If your net worth is negative, you owe more money than you own. Makes sense? If not, read that again.

This is not a desirable state of affairs for sure. To know your net worth, you can calculate it using Moneysense’s Net Worth Calculator. The numbers will help you take stock of your current financial situation.

For those who are severely indebted, with a net worth of – S$15,000 or less, you may wish to consider examining Singapore’s bankruptcy laws to help you repair your finances and start afresh.

#5: Housing expenses over 40% of your gross income

To find out your ideal housing expenses, simply multiply your monthly income by 0.3 or 0.4 to see what your monthly budget for housing expenses should be. If your rent exceeds this number, you may need to try and find a less expensive apartment and not survive just on your savings.

#6: Spending to keep up with social influences

Image Credits: motors.hongsehgroup.com

In our current age of Instagram and TikTok, it is easy to get swirled into the world’s neverending wants. We may see influencers, friends, or family members buying new items or taking expensive staycations and begin to wonder if we should do the same.

But before we buy that latest device or spend money on an extravagant restaurant date, we must ask if we’re doing this for ourselves or to impress someone else on the worldwide web? Is it worth finding money in the budget to keep up with appearances?

Spend your money wisely and avoid the trap of wanting the latest of everything because that will only lead you down the point of no return.

#7: Your savings are literally zero

An absence of savings is a common-sense indicator of excessive spending.

A healthy savings account can help you survive unexpected expenses medically related and help you prepare for significant life events like starting a family or even early retirement.

If your savings account is empty or underfunded, you are spending too much and saving too little. Finding small opportunities to save money will help get your spending under control and your savings back on track.

Are you in need of quick cash for an emergency? One of the most important factors when considering applying for a personal loan is the interest rate.

Whether you’re planning to go for the Standard Chartered CashOne Personal Loan (as low as 3.48% p.a.) or CIMB CashLite (3.5% p.a.), pause for a moment to think it through.

Ask yourself these questions before getting a personal loan.

#1: Why do you need the money?

There are many reasons you may wish to borrow money. Maybe you’re faced with medical bills or unexpected home renovations.

For those looking to pay off high-interest debt, applying for a personal loan would make sense too. For example, if you have a credit card debt at a 25% interest rate per year, it would be wise to take up a personal loan with a 7% interest rate to consolidate your debts and pay it off first.

Go ahead and get that personal loan if you know it’s for a good cause, such as reducing the interest.

#2: What is the interest rate?

Image Credits: Investopedia

Speaking of interest, here’s our next point.

Before you borrow money, understand that the lender will make a profit by charging you interest. According to Investopedia, interest is a charge applied to you, expressed as a principal percentage. And, of course, a lower interest rate is better for you as the borrower.

However, it’s not as simple as it seems. There are two rates to consider: Applied Rate (AR) and Effective Interest Rate (EIR). In short, AR keeps the loan principal as a constant over the life of the loan. In contrast, EIR calculates the reduction in principal as you pay down the sum.

Do more research if you are unsure of the terms.

#3: Are there other charges?

In addition to interest, there may be additional fees.

Possible charges include a fixed annual fee tagged to borrowing, a late payment fee if you miss a payment, or a change fee if you need to renegotiate your loan terms.

Some banks even charge an early repayment fee as early repayments affect a portion of their predicted profits. Be aware of these possible charges before you move forward with the application.

#4: Can you manage the loan repayments?

Image Credits: The Economic Times

When considering whether to take up a personal loan, you must decide if you can handle the repayments.

Once you know the interest rate, extra fees, and anticipated monthly repayment amount, make necessary calculations from your income to see if you can afford to pay it back.

To do so, you want to write out a detailed budget including your spending needs on groceries, household bills, and miscellaneous expenses. From the breakdown, see if you have enough leftovers to weather an unforeseen financial storm.

Yes, that’s for your rainy days.

#5: How will it affect your credit score?

Lenders use credit scores to decide whether to issue you a loan. Credit scores affect loan terms such as interest rates, tenure, and principal limits.

Your payment history, the ratio of debt to credit, the age and quantity of your accounts you own, and any derogatory reports such as loan defaults can affect your credit score.

If you think you can do without a personal loan this time around, then skip it. Ensuring that your credit is in good shape will help you get a better loan in the future when you seriously need it.

It prevents financial institutions from lending new credit facilities to borrowers with debts greater than six times their monthly income. This credit limit helps to protect borrowers from getting into high debts too much to bear.

And of course, other than CLMM implemented by the authorities, other factors will also affect your borrowing limit. This includes your credit score, monthly salary, and the relationship you have with the bank.

#7: How reliable is the lender?

Be mindful that some people and institutions may not be worth your time and transaction in any situation involving money.

If a lender fails to run a credit check, seems disorganised, or cannot answer basic questions, be wary. You want to deal with a reputable banking institution and not one that agrees to a loan without reviewing your credit history.

#8: When will you get the funds?

Image Credits: Jmc Accounts

Most people seeking personal loans are racing against time. If that is a factor, you want to find out how long is the approval process. From approval to disbursement of the loan, speeds will vary from bank to bank.

Here are three personal loans promising instant processing times:

The decision to borrow money should be considered carefully. Evaluating and understanding your loan’s reasons, the interest rates, loan repayments, and more mentioned in this article can help you make the best decision possible when seeking a personal loan.

It is fair to say that most of us want to achieve financial freedom. To have enough savings and solid investments to afford the lifestyle you wish to can sound really attractive. Unfortunately, finding that freedom can be challenging.

Many people hold debt, overspend, or encounter challenges that make financial freedom challenging to achieve. However, all hope is not lost. Develop and maintain these simple financial habits if you want to attain financial freedom.

#1: Set specific goals

A goal like “I am going to be rich one day” is vague. A better way to set targets is to use the SMART technique. They should be Specific, Measurable, Achievable, Realistic, and Time-focused.

You should be working towards a SMART aim like “I am going to increase my savings by 1% a month for twelve months.” Write your desire down in a journal, and make it your mantra. Specific goals lead to accurate results, so cut out that fluff thinking.

#2: Write a budget

Image Credits: pixabay.com

Budgeting is essential for wise money management. Instead of squandering money away and realising reason why i’m broke, it’s better to start analysing your spending habits.

Ensure your bills are promptly paid and your savings are funded before allocating money to luxury expenses or feed your lifestyle inflation. Understanding where your money goes each day is the best way to control your urge to splurge.

#3: Clear your debts

With existing debts looming over your life, financial freedom seems like a faraway dream. When you owe financial institutions money, don’t forget that the interests are rolling.

To eliminate debt, you may want to try the pyramid strategy. Pay off your smallest debt first, then allocate that money to your next-smallest bill, and so on until you have paid your debts off altogether.

We can’t emphasise enough because it’s one of the stablest ways to grow your savings. If you have a direct salary deposit from your employer to your bank account on payday, ensure a percentage of your income goes into savings right away.

It’s easy to set up recurring transfers to send money to a specific saving account every time you get paid, so you shouldn’t be giving any lame excuses. Once the automation is in, the routine will ease you into saving, so resist the urge to withdraw.

Take ownership to have at least a basic understanding of how money works – be it in the topic of debt or investments. Read books written by experts or consider taking some courses to develop your knowledge of money.

Speaking of which, do you know that Seedly is organising a Personal Finance Festival 2021? The most extensive personal finance event in Singapore is happening on Saturday, 10 April 2021, from 10am to 5pm. Read more about it here.

Yes, the market is volatile and can occasionally crash. Unforeseen circumstances can cause even the most robust markets to shrink. But without risk, there is no return. As such, the stock market is one of the greatest ways to grow your wealth.

If you know not where to get started, how about beginning your journey through Robo-advisors? From OCBC RoboInvest to DBS digiPortfolio and Stashaway, there are several local options for Singapore investors.

#7: Monitor your credit scores

Your credit score is the first thing lenders will examine when you wish to make a major purchase, such as a car or a house.

Do you know how to grab hold of your credit report? You can get a copy from the Credit Bureau (Singapore). Each CBS Credit Report is chargeable at S$6.42 (inclusive of GST). Simply make a purchase online, at any SingPost branches, at the Credit Bureau office, or CrimsonLogic Service Bureaus.

If you achieve financial freedom but then neglect your health, your hard work could go to waste due to unexpected healthcare costs. Constant exercise, eating right, and avoiding unhealthy lifestyle choices will benefit you in the long run.

While you take of your health, don’t forget to keep an eye on your things. Making sure that they last longer can help you save money.

This is true for everything, from mobile phones to laptops and cars. Keeping them well-maintained is likely to increase their lifespan and save you money on costly repairs or replacements down the road.

#9: Don’t exceed your means

Frugality is frequently on our radar, and you might have read about it in several money-themed blogs too. But you know what? It is an excellent trait for achieving financial freedom, and we’re going to play it like a broken record.

The ideal way to live within your means is to distinguish between things you want and the things you need. Just because you can afford something does not mean you need to buy it. If there’s a cheaper option out there, go for it.

#10: Talk to an expert

Image Credits: Great Eastern

Once you have accumulated some savings, talk to a professional about how to manage your money. Picking the right financial advisor who is legally obligated to act in your best interest instead of theirs is vital.

Final thoughts

While financial freedom may seem like a daunting goal to reach, it is well within your means to achieve it! Taking a disciplined approach and developing the abovementioned habits over time will help you get to your desired state of financial freedom in no time.

2020 was a bust. If you haven’t done anything about your personal finances then, you could just blame it on the COVID-19 pandemic.

But it’s 2021.

And it looks like we’re going to have to live with COVID-19 for a while.

So if you’re still living from paycheck to paycheck.

Or maybe you’re still putting off investing for your future.

Or you haven’t bought insurance to protect yourself and your loved ones…

Well, it’s time to stop making excuses this year and do something about it! And all you need is one day!

Be Part of Singapore’s Largest Personal Finance Festival

It’s 2021, and Seedly is back to help YOU take control of your personal finances with Seedly Personal Finance Festival 2021 — the LARGEST personal finance festival in Singapore — that is happening on Saturday, 10 April 2021, 10am to 5pm.

On Monday, 1 March 2021 only, enjoy 50% OFF Seedly Personal Finance Festival 2021 tickets:

All Access Pass at $5 (usual price $10)

The first 2,000 ticket sign-ups will also get a limited edition goodie bag worth $55!

Act fast because the tickets for Seedly Personal Finance Festival 2020 were sold out within 5 hours!

What Is Seedly Personal Finance Festival 2021 About?

Seedly Personal Finance Festival 2021 is Singapore’s largest personal finance festival where you can learn to take control of your personal finances in one day.

You can expect keynotes, discussion panels, and workshops on various topics like:

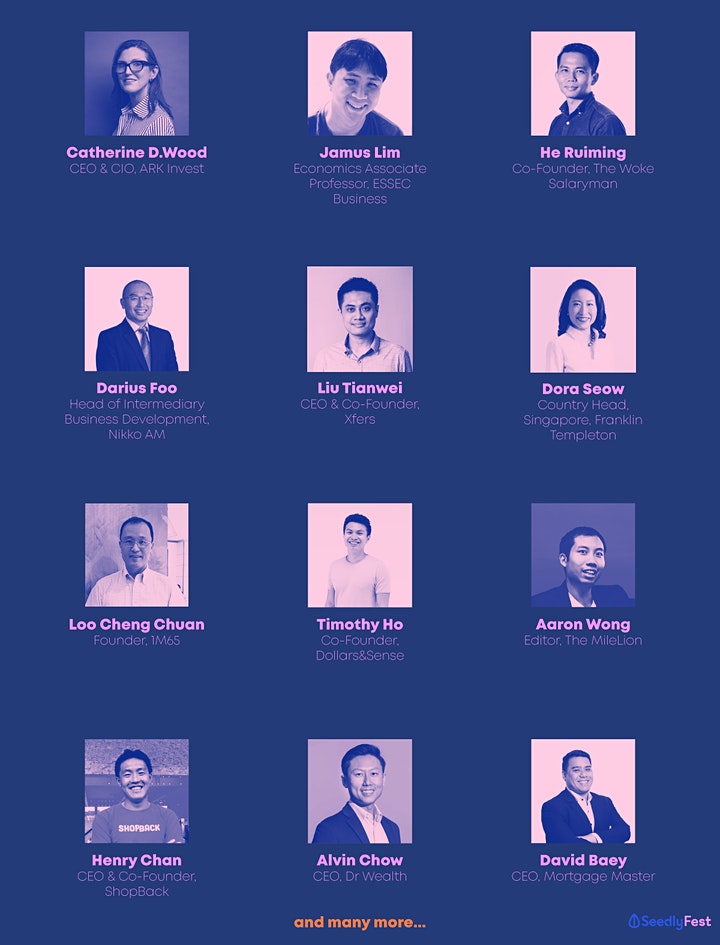

All of these will be presented in an actionable and simple manner by an international line-up of experts, industry titans, and leaders from the personal finance space like:

Catherine D. Wood, Founder, CEO & CIO of ARK Invest

Jamus Lim, International Economist & Associate Prof of Economics, ESSEC Asia-Pacific

Goh Wei Choon and He Ruiming, Co-founders of The Woke Salaryman

Liu Tianwei, CEO & Co-founder of Xfers

Dora Seow, Country Head Singapore, Franklin Templeton

Loo Cheng Chuan, Founder of 1M65

To sweeten the deal, there’re even lucky draws where you can stand a chance to win $3,200 worth of prizes and staycations from 6 luxury hotels!

Sort out your personal finances and get a chance to relax at a swanky hotel like Capella, Marina Bay Sands, or Andaz for free? Sounds like a fiscally responsible decision.

Where and When Is Seedly Personal Finance Festival 2021?

Due to COVID-19, Seedly Personal Finance Festival 2021 will be held virtually on Saturday, 10 April 2021, 10am to 5pm.

Where to Buy Tickets for Seedly Personal Finance Festival 2021?

Just head over to the Seedly Personal Finance Festival 2021 website and buy your tickets on 1 March 2021 to enjoy the 50% discount off an All Access Pass!