According to the High Court, an individual becomes bankrupt if he or she owes at least S$10,000 and has no means to pay it.

Filing for bankruptcy can be done by the creditor or the debtor. A deposit of S$1,600 to the Official Assignee (OA) is required. The OA is the authority that is responsible for selling as many of your assets as possible to repay your creditors. Credit bureaus will display your bankruptcy date for five years after the date of discharge.

Aside from this, it is essential to note that there are assets that are protected by the creditors such as furniture, HDB flats, compensation awarded for legal actions, and life insurance policies.

The effect of bankruptcy does not only take a toll on your finances but also on other aspects of your life. For instance, there will be restrictions in travelling overseas and in looking for a job especially as a director of a company. Truly, it drastically affects your lifestyle, your career, and your relationships.

This is why it is important to avoid falling to this “black hole” by being financially knowledgable. To put it in perspective, here are 4 Ways To Prevent Bankruptcy…

MANAGE YOUR DEBTS

First, be aware of how much your debts and assets total to. Include every billing statement, every document, loans, and mortgages you may have. Take immediate action when you notice that it is getting hard to pay for your debts.

CUT DOWN YOUR EXPENSES

After seeing the bigger picture, it is time to cut down your expenses. Reduce the unnecessary expenses first such as designer bags or costly coffee beans. Then, add the minimum payments of your debts and the cost of your necessities to your monthly budget.

SELL YOUR STUFF

To aid your budget, you must sell your unnecessary items among others. Selling whatever you can spare can help pay off your multiplying debts.

SEEK HELP

Calculate the money that you need to prevent bankruptcy. Examine how much money you are able to get. Then, consider seeking help from your family and friends to make up for the difference. Yes! Asking your friends and family for money maybe a shady area but this situation is an exception.

If you still find it uncomfortable to seek their help then, consider hiring a professional (e.g., credit counseling agency or debt management firm) to help you reduce your interest rates and penalties at friendly time frame.

In order to make your dream of retiring early a reality, you generally have two options: to spend less or to earn more. If you are an avid reader of personal articles, it is no surprise that spending less is included in “Ways To Save For Retirement”. But, when you want to focus on maximizing your earning potential then, you will have to do several measures to earn more.

SPENDING LESS

Pros:

Spending less gives an a more instantaneous result compared to earning more due to its direct nature. It is easier to accomplish because of money management and budgeting techniques.

Cons:

There is a limit to when you can spend less before you hit a boiling point. For instance, some people restrict their way of life to the point that it is extremely uncomfortable and unsatisfactory.

Tips:

Lower your utility bills by unplugging cables, turning off the lights, and minimizing the air conditioner temperature.

Cancel your hand phone plans and switch to prepaid in order to regulate your telecom bills.

It is important to track where your money is going through the last month’s bank statements and receipts. Notice what you have spending too much on and reduce it.

Cut down your T.V. bill by canceling your cable subscription and opting for watching at Toggle.sg. Toggle.sg lets you watch episodes of your favorite shows at Channel 5, Channel 8, Channel U, Okto, Suria, and Vasantham – for free! But, viewing of premium content is on a subscription basis.

Lastly, if you are buying a new appliance, make sure that it is an energy efficient model. Smaller appliances not only help you save more on space but on bills also.

EARNING MORE

Pros:

The ways you can earn are endless. Ultimately, it is based on your good financial choices, a ton of effort, and a sprinkle of luck. Additionally, here is no limitation in the amount you can possibly earn.

Cons:

Making more money takes time and effort. You will need to find a better job or to work more hours in order get a start-up capital for your small business. The flow of profit after the initial business launch takes time too.

Tips:

Increase your earnings by upgrading your skills. To upgrade your skills, you can enroll to workshops or courses. Consider going down to your community centre (CC) and find out the affordable courses they offer. Transform the awesome skills you learned into viable freelance businesses or part-time occupations.

Start your own small business such as an online clothing shop. Online business allows you to sell your product or service at the convenience of your own home and your own time.

Lastly, contemplate on proposing a salary increase or a leaving the company for a better company.

WHICH ONE WEIGHS MORE?

On your way to save for your retirement fund, frugality or spending less is the first step. Once you are financially stable, it makes more sense to seek for higher income.

You can earn millions of dollars but if you are spending irrationally, you can get into financial problems. And, even if you are cutting down your spending, you may not reach your goal if you do not earn a decent amount of money. So, the best way to reach your retirement goal is to have a combination of both options.

Gold is probably the most vaunted precious metal most people are familiar with. Indeed, grannies love to don this prized jewellery around their necks while grandpas revel in displaying their wealth with their 18K golden Rolexes.

But this is not all. Gold has far more phenomenal uses than you can ever imagine. And this is part of the reason why the price of gold has not fallen beyond S$1,450 per ounce for the past 5 years.

Image credit: luxpresso.com

Most electronic devices

While 78% of the gold consumed every year is used for jewellery, the most significant industrial use of gold is manifested in electronics. Gold is a highly efficient conductor of electricity, only second to silver and copper. From pocket electronic gadgets to large electronic appliances, gold shows up in almost all of them, albeit in minute amounts. If you own a mobile phone, a calculator, a computer, a global positioning system unit and a television set, you are definitely a proud owner of gold. But the reason for the hefty price of iPhone 6 Gold does not lie in the gold content, for most of the mobile phones merely contain around 50 cents worth of gold.

Image credit: blog.badonlinedates.com

Medical uses

Want a vibrant golden smile? Dentists are still using gold alloys for tooth fillings, crowns, and bridges because gold is durable, non-allergenic and corrosion-free like silver and platinum. Many surgical instruments and life-support devices are also manufactured with tiny amounts of gold. Gold is a component in drugs to treat medical conditions such as the joint disorder arthritis by reducing swelling, bone damage and relieving joint pain and stiffness. For the diagnosis of diseases, gold is also injected into the body in its radioactive form.

Image credit: goldresource.net

Aerospace

Have you ever thought of what space vehicles are made of? Many parts are actually fitted with gold-coated polyester film to reflect infrared radiation and stabilize the temperature of the spacecraft or risk overheating. As gold is malleable, it also acts as a lubricant between the mechanical parts of the spacecraft in orbit.

Before committing to any investment, it is always prudent to find out the uses of the particular financial product. It allows you to project its future returns more accurately based on economically sound fundamentals instead of sheer speculation. It is also critical to know the relationships between gold price, U.S. dollar and interest rates. The appreciating dollar and prospects for higher U.S. interest rates have curbed gold’s gleaming appeal as a protection of wealth and led to its price decline. Finally, given that the biggest consumer markets are none other than India and China, their economic growth would inevitably impact the gold price significantly.

While i love the amazing skyline from Victoria Peak, what got me excited were not the insta-worthy photos i took or the dim sum i gobbled down at Lung King Heen.

It was the fact that i actually travel for free.

Free? Does it means that i won a free trip to Hong Kong or had my travel sponsored by a company?

Good guess, but nope!

Well, the trick here is about planning my own finances. I couldn’t have included Hong Kong into the list of places to visit without exceeding the budget i set aside for this year.

A few years ago when i was still a student, i didn’t care too much about my own finances since i was spending within my means. Like many others, I had my money stashed away in a POSB’s saving account. Who care about interest rates when we hardly have five figures in our possession? The returns were pittance that it hardly warrant any extra attention.

My attitude changed when i had friends who were boasting about how much money they were making. I told myself i wanted to be like them — to be rich, in the shortest amount of time.

It seems then that the only way is to investventure gamble into the stocks market. I had no idea where to start until one day i was approached by a financial adviser when i was exiting the MRT station. And being a ambitious and impulsive young adult, i was persuaded into buying a saving plan that invests into the market with some kind of insurance cover that comes with it.

It felt good even though i had no idea what i was buying into – the feel good factor that i am now investing like an adult.

I call in to check on the policy every month, but apparently i was told that it is still in the early stage and had little or no cash value.

After a few months i gave up because it hardly grows and sadly i was told that if i were to terminate the plan, i would end up with almost nothing.

The change

From then on, I told myself that no one else can manage my own finances except myself. I need to take the responsibility or i will be the one suffering down the road.

I spend months reading up on books, forums, MoneySense and any resources that i could laid hands on. I begin to understand the importance of budgeting, investing and how to manage my own finances.

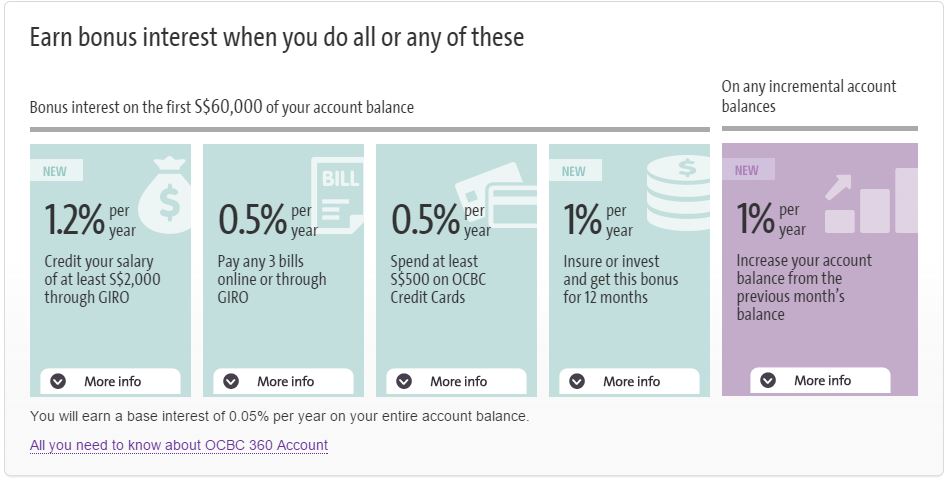

I started by switching my funds to a higher interest-bearing account such as the OCBC 360 where customers could potentially earn up to 3.25% as at 1 May 2015.

It was also then that i realized that previously i was holding on to an investment-linked plan which comes with high fee and charges. It is not cost-effective to achieve my goals and i had to take the hard decision to surrender and make a loss.

A better way that i learnt is to buy term insurance and invest the difference. Term insurance is cheap and affordable although it does not have cash value. But the difference i could potentially save could be put into better investment vehicle such as the low cost fund that tracks the Straits Time Index (STI) which has a historical return of around 8 per cent in the long run.

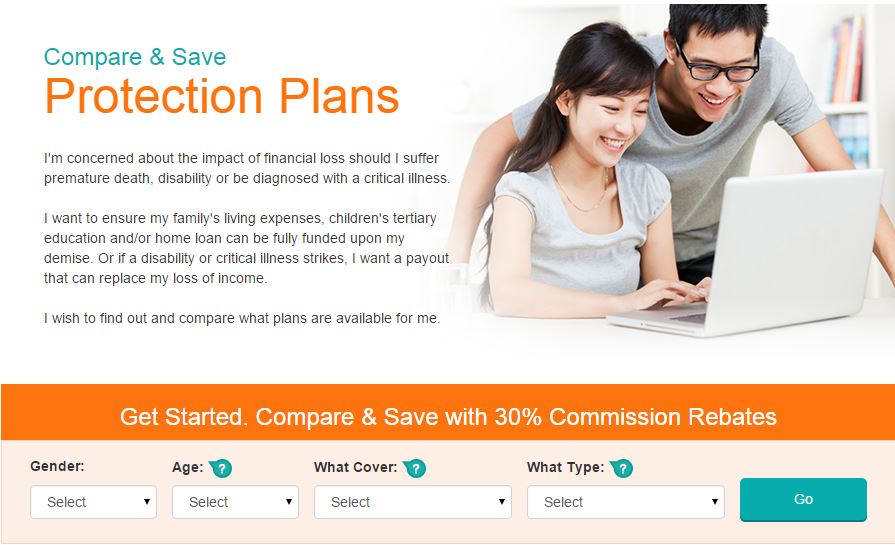

I was introduced to the online platform DIYInsurance — a portal which allows me to compare the different term insurance plans out there. What appeals to me is that they rebate 30% of the commission back to the customer and at the same time still make an effort to go through the planning process, making sure that the person is on the right track.

They have a live chat system where i can ask any questions on how to use the online platform, as well as clarifying with the client services manager on the semantics of insurance definition. It was fuss free and it beats the inconvenience of holding on to the line when you call in to financial institutions for enquiries.

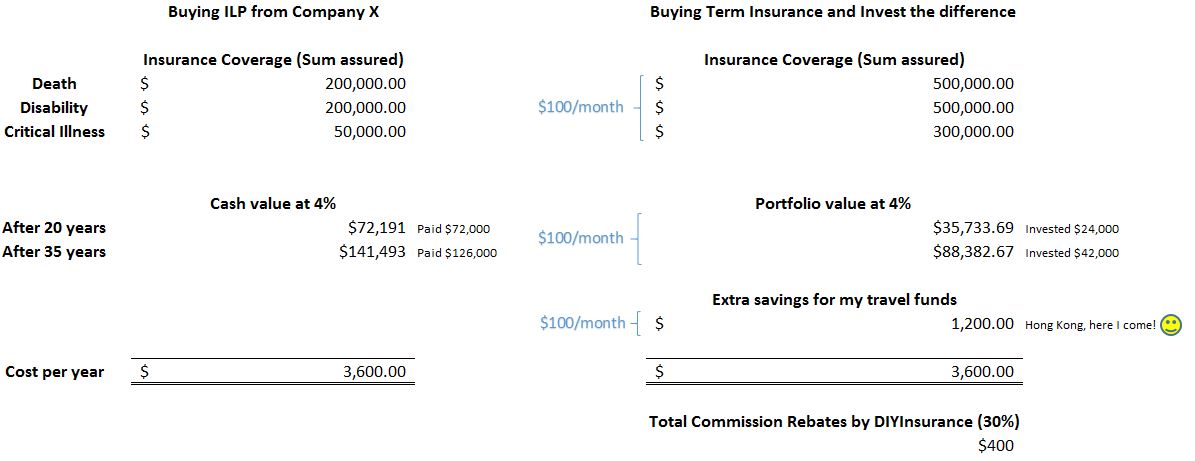

If you are wondering how much money i save using the DIY method, i have done up some numbers for comparison.

(Click to enlarge)

As you can see, i was previously paying $300 a month for a $200K cover on death and disability and a $50K rider on critical illnesses. If the funds grow at 4%, it will take me 20 years to break even and 35 years to make a small profit of $15K. (calculate the ROI)

If i were to employ the alternative strategy of buying term and investing the difference, i’d be merely paying $100 a month for a $500K cover on death, disability and $300K on critical illnesses. The other $100 will be channeled to a low cost fund, and assuming it grows at the same rate, my portfolio would be sitting at a value of $35K after 20 years or $88K after 35 years. (note that i’m contributing 2/3 of what i’d have otherwise contributed to the ILP and i have pegged its growth at 4% for comparison purposes)

As a result, i managed to put away $100 a month into my travel funds and this adds up to a significant amount of $1,200 a year. A sum that is sufficient for me to pay for the return air ticket to Hong Kong which including hotel and shopping expenses incurred during the trip. I am also getting $400 worth of commission rebates from DIYInsurance which i can either re-invest or spend it on my next trip. (I have re-invested it)

In conclusion

By taking charge of my own finances, i am now enjoying a higher returns of 2.25% (excluding the 1% bonus to insure or invest) from the money sitting in the bank as well as future incoming funds. I have also manage to cut down on unnecessary fee and charges slapped on expensive insurance products by switching to a more affordable term cover and investing in a low cost funds.

I have lost some money in the investment linked product but at the same time i have took home valuable knowledge and wisdom of managing my own finances, and as a result, created more wealth from it.

Well, perhaps a road trip to Australia next?

(Article contributed by Cheryl, a Marketing Executive working in Singapore.)

We frequently hear of the word “economics” in papers or conversations, but how useful or applicable is this course of study to the real world?

Understanding economics is in reality fundamental to understanding the price movements of every single good and service in our economy. It is the aggregation of the demand and supply forces. Indeed, when we see the airfare skyrockets after the end of school term, it is economics at work. Huge travel demand outweighing limited supply of passenger seats leads to propped up prices. As such, appreciating and capitalising on economic knowledge could end you up in deeper pockets.

While it may be too time consuming and superfluous to master all the economic theories, knowing a few essential concepts may come in handy in guiding our financial and behavioral decisions.

Thanks to the prudent policies administered by MAS, Singapore enjoys a low inflation rate of 2.8% on average since 1962. However, a simple comparison between the interest rates offered by various banks indicates a mere 1.3% as the most competitive rate for 1-year fixed deposits.

What this means: The fund sitting in your bank is losing 1.5% of its value to be exchanged into goods and services annually. Given that you have $100 in your bank today, you can afford to buy 50 McChicken burgers. But one year down the road, you can only afford to purchase 49.25 of them.

Course of actions to be taken: Since the saving rate is not commensurate with the inflation rate, we may be better off investing in alternative assets that provide higher yields. However, if every rational and irrational soul is doing that, risks abound as illustrated below.

Stock investment

(Image credit: thenest.com)

Investing in stocks can yield 2 kinds of returns, namely dividend yield and capital gains yield. The former tends to be more predictable than the latter, especially if the company holds a long term track record of constant or growing dividend stream.

How to value stocks: Dividend yield is an objective measure in guiding investment decisions since they are realised returns and a better indicator of future returns. On the other hand, be extra cautious during stock encounters with historically impressive capital appreciation. Gullible investors may be tempted to buy these shares as they often fail to realise the high variability of capital gains yield could be complicated by the problem of information asymmetry where insiders possess and exploit private information to the disadvantage of outsiders.

Course of actions to be taken: Both insiders and outsiders have to keep abreast of news and developments in the macroeconomy and international economies as they affect stock returns systemically.

Specifically for outsiders, it is crucial to have a good grasp of the economic fundamentals (such as the consistency of dividend payouts and growth potential) of the company that helps to steer towards a proper valuation. A long term investment horizon is more favourable as it puts them on a more level ground with the insiders. If the outsiders were to invest in the short term, speculation is usually involved since by definition, the fact that they do not possess the superior private knowledge is prejudicial to them.

For more well-heeled investors looking to diversify their portfolio, real estate investment seems the way to go. Similarly, real estate assets provide 2 types of returns, specifically rental yield and capital gains yield. Best of all, a residential property provides its owner(s) a physical shelter to live in. Despite these benefits though, investors should be wary of overpaying for homes.

How to value property: Rental yield is an objective measure in guiding investment decisions since it measures the payback period of the hefty mortgage loan that homebuyers commit to. The URA Masterplan and a concise understanding of demographics are vital tools in predicting the capital gains yield.

Course of actions to be taken: Beware of one-off anomalous sale transactions that are not reflective of the true market forces. Stay out of homes in which the overinflated prices are not underpinned by strong economic fundamentals (such as location, amenities and size). Buy during a recessionary period instead of an inflationary period. Timing the market makes an enormous difference in your bank account.

Investments aside, most of us contribute to the economy through our employment. But to maximise the return on our faculties and time, insights have to be drawn from the demand and supply forces.

Some simple mathematics to gauge how financially rewarding is a particular industry: If the staff turnover is high (due to long working hours, poor welfare, unchallenging job roles etc.), companies should offer higher wages to attract or retain workers.

However, this is not happening. Reason being a ready supply of potential (local and foreign) employees provides virtually no impetus for corporations to raise salaries. Does this plight sound familiar?

Course of actions to be taken: Instead of complaining about meagre wages, pursue a career in an alternative industry with market dynamics (i.e. less competition) working in your favour. Although it may seem counter-intuitive, you actually build greater wealth bucking the norm and doing what others don’t do. Better still, venture into a new industry and gain the first mover advantage.

Now you see, having a good understanding of economics is useful in our day-to-day living as it forms an integral basis for making financially sound decisions.