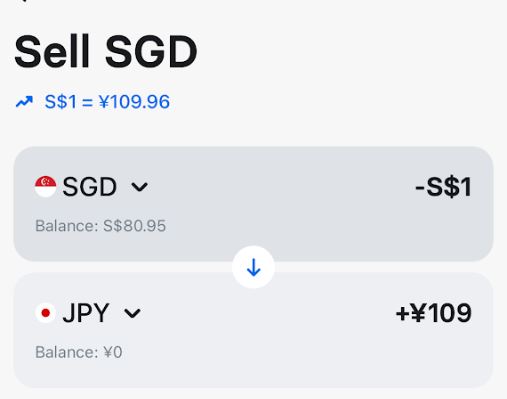

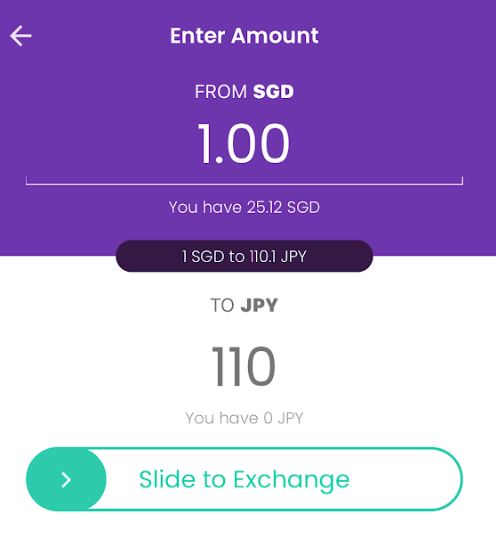

The Singapore Dollar (SGD) has hit a record high against the Japanese Yen (JPY), with the exchange rate reaching as high as ¥110.10 for every 1 Singapore Dollar on 31 October 2023.

The Japanese Yen (JPY) experienced a decline in value due to the Bank of Japan’s (BoJ) commitment to maintaining an exceptionally accommodative policy to bolster the domestic economy.

For those who are planning a trip to Japan soon, this might be a good time to exchange for some Japanese yen.

When the exchange rate hits 109.66 in October this year, many customers have visited local money changers to stash up on the currency. For those who are own multi-currency travel wallets such as YouTrip or Revolut can take advantage of the favourable exchange rate to do an in-app exchange in real time.

If you’re a pet parent and want things to be taken care of properly when you leave this world, you’ve got to start digging deep into estate planning for pets.

Never heard of or the idea has never crossed your mind?

Well, allow us to share with you more in this post.

Indirect beneficiary

Providing for your furkid is like providing for a vulnerable beneficiary.

But do you know that our animal companions are classified as property? This means they cannot be named directly as beneficiaries or inherit our stuff.

Simply put, I cannot leave a lump sum directly to my puppy. However, in my will, I can name a caretaker as a beneficiary. As long as they agree to take care of my sweet fluff, then my pup becomes an ‘indirect beneficiary’.

Just relying on a family member or relative without entrusting them with money is not a good idea. Who wants to take sudden responsibility for a furkid if they have to pay extra out of their own pocket?

With that said, structure your will properly so that your appointed caregiver can only access your money after confirming they will take care of your pet.

A safer bet with a pet trust

Sure, a legally binding document to distribute your estate can give you peace of mind. And you can name your caregiver and earmark money.

But once assets are distributed, the job’s done. In other words, the will executor is not legally bound to see your wishes through.

So how?

If you want a more confirm plus chop bet, this is where a pet trust comes in useful.

Setting up a trust by appointing a trustee company means they are lawfully tied to carry out your instructions according to your wishes. Whereas a will is based on trust between you and your appointed caregiver only.

With a pet trust, your chosen caregiver is legally restrained to only spend money on your pet’s needs, not on their personal wants. Otherwise, they may risk having their funds frozen.

Image Credits: unsplash.com

How much money should you leave behind?

How much money do you need to leave behind for your pet?

A good way to estimate the amount is to take their annual spending and factor in their breed lifespan. Then make your calculations.

For instance, if your cat is expected to live 10 more years and you spend $1,000/year, that means you need to allocate at least $10,000.

But vet visits may increase when they are older so plan for medical bills or consider pet insurance to cover those costs. Don’t forget to factor in inflation too.

As we come to a close, do you know how much estate planning costs?

Depending on the complexity, we’re looking at a few hundred dollars to thousands of dollars for those that involve testamentary trust or standby trust.

If you want to know the exact numbers, you should hit up a financial advisor or estate planner for the deets.

Life is short and unexpected, so there’s no harm in starting to plan early if you want your furkid (and your money) to be in good hands after you bid goodbye to life on earth.

Considering CFD or Forex trading for your financial portfolio? This article gives you a clear picture of their differences and how you can get started.

Forex and CFDs are international financial instruments. Both are highly leveraged instruments that offer the possibility of financial success, but they are not the same. Contracts for difference are a special kind of derivative financial product, while Forex involves buying and selling currencies.

What Is CFD Trading?

Contracts for Difference are derivative contracts allowing investors to speculate on price changes in underlying assets without purchasing or owning such assets. They enable investors to trade the difference between an asset’s opening and closing prices through a broker. CFD trading offers a wide variety of assets, including stocks, indices, commodities, and cryptocurrencies. Its minimal barrier to entry means it can be used by anybody, anywhere in the world. Using leverage, you may manage bigger holdings with the same amount of money.

What Is Forex Trading?

Foreign exchange is the buying and selling of currencies in the Foreign Exchange market. Currency exchange is decentralized, allowing traders to purchase and sell currency pairings like GBP/JPY or EUR/USD to benefit from price changes. Due to the overlap of sessions in several time zones, currency trading can occur around the clock, five days a week. As in CFD trading, traders can use leverage to magnify their gains on a reduced financial investment.

What Is the Difference Between a CFD and Forex Trading?

Unlike Forex trading, which only trades currencies, CFDs allow you to speculate on various markets your broker can cover. Traders can take a bullish or a bearish stance on an asset and place either a short or a long position. Gains or losses are determined by the fluctuation between the asset’s opening and closing prices.

The foreign exchange market is global in scope. There is typically no centralized currency exchange. The value of one currency is exchanged in relation to another.

Pips are the smallest increment of change in a currency pair that can result in a profit or loss.

Leverage is a feature of Forex and CFD trading that allows investors to manage a larger position with the same amount of cash. However, leverage amounts may vary depending on factors like the broker, location, and regulations.

Liquidity and Access to the Market

Since the foreign exchange market is open around the clock across several time zones and can be accessed by anybody with an internet connection and a broker account, it offers excellent market access and liquidity. The forex market is the most liquid financial marketplace, with daily exchange volume averaging $6 trillion. In addition, this market has low entry barriers, necessitating only a little starting capital investment and some familiarity with currency pairs.

Market access and liquidity of CFD trading make it possible to trade on a wide variety of worldwide marketplaces throughout their respective hours. As expected, they vary depending on the underlying asset being traded. Traders benefit from this variety of markets and assets but face problems like adapting to various laws, fees, spreads, and commissions.

Spreads, Commissions, and Other Charges

The spread, or the difference between the broker-quoted buy and sell price, is a frequent cost associated with buying and selling CFDs and FX. This charge covers your broker’s overhead and the money they make from your trades. The spread shifts due to changes in the asset, the broker, the market, and the liquidity.

Currency trading on the FX market has more competitive spreads than CFDs since more people trade in this market. In addition to spreads, you may incur other expenses for each trade while trading CFDs. CFD trading makes greater use of them, especially when dealing with equities and indices.

Foreign exchange trading can be done for speculative purposes, although its principal function is facilitating commerce and investment across national boundaries. Foreign exchange markets include transactions between central banks, businesses, institutional investors, and private speculators. Hedging is another reason people trade Forex. Currency traders often work with forex brokers, although Forex can also be traded on the Contracts for Difference market.

The initial intent of the CFD market was to serve as a hedging mechanism. CFD contracts can be a hedging tool for existing equity and commodity investments. Contracts for difference do not expire like option contracts. Rolling over overnight contracts may incur additional fees depending on the provider. Since there is currently no oversight, the fees may differ.

Mini and micro units are more manageable for smaller traders and are available for several currency transactions. Currency futures contracts can also be traded as options. Currency exchange-traded funds (ETFs) allow investors to trade currencies on the stock exchange.

Final Words: How To Trade CFD and Forex

First, you must create and fund an account with a trustworthy broker. Make sure your broker has a solid reputation through background research.

After selecting a broker and opening an account with them, you will need to fund your account using the method you have chosen. Some account types and platforms are more suited to your specific needs and style than others, so do your homework.

You should also choose a way to trade that is consistent with your objectives and risk comfort level. You can reduce your risk and enter and exit positions with more consideration when you have a plan. You can use technical and fundamental analysis to spot opportunities and determine when to enter and quit a market.

Ultimately, you must decide which asset or currency pair to trade. Studying the economic statistics, geopolitical events, and central bank policies that affect the price fluctuations of your preferred currency pair is crucial. After deciding the currency pair to trade in, you may purchase or sell it on your platform. Always keep a tight eye on your investments and employ risk management strategies to reduce potential losses.

Comparison is the thief of joy, and keeping up appearances with friends can be detrimental to one’s physical, mental, and financial health. As you scroll through your Facebook or Instagram timeline, you witness the highlights of your friends’ lives. However, people mostly share their triumphs rather than their struggles. In today’s social media-driven world, where meticulously crafted profiles and highlight reels dominate our online presence, the pressure to maintain a façade with friends has become increasingly arduous.

On these platforms, you are exposed to their accomplishments, extravagant trips, new cars, lavish weddings, and piles of gifts on Christmas and birthdays. Social media continuously raises the bar for what people with average salaries feel compelled to do in order to compete not only with celebrities but also with their own friends, striving to be perceived as successful.

We strive to present ourselves in a positive light, displaying our best moments and achievements. However, behind the polished facade, preserving these appearances can take a toll on our mental and emotional well-being. In this article, we will explore the reasons why it has become difficult to keep up appearances with friends and delve into the potential consequences of this constant need for validation.

FEAR OF JUDGMENT

The fear of being judged is one of the primary reasons why maintaining appearances with friends is challenging. We worry that if we reveal our vulnerabilities, struggles, or imperfections, our friends might perceive us differently. This fear drives us to constantly seek validation and present an idealized version of ourselves instead of embracing our true selves.

SOCIAL MEDIA INFLUENCE

The rise of social media platforms has significantly contributed to the pressure of keeping up appearances. Platforms like Instagram and Facebook emphasize the importance of portraying a flawless life filled with extravagant vacations, glamorous events, and remarkable accomplishments. Comparing our lives to the carefully curated content of others can leave us feeling inadequate, fostering a sense of insecurity and compelling us to maintain a facade that aligns with societal expectations.

Image Credits: unsplash.com

EMOTIONAL EXHAUSTION

Comparing ourselves to others diminishes our own accomplishments and robs us of the joy we should feel for our own success. Constantly presenting an idealized version of us to friends can be emotionally draining. When we feel the need to always appear happy, successful, and content, we deny ourselves the opportunity to express our true emotions. Bottling up our feelings can lead to increased stress, anxiety, and a sense of isolation, as we fear that revealing our struggles may result in rejection or disapproval from our friends.

UNREALISTIC EXPECTATIONS

The pressure to keep up appearances with friends arises from the unrealistic expectations set by society. We are bombarded with images and stories of seemingly perfect lives, leaving us feeling inadequate if our own lives don’t measure up. This can create a vicious cycle of comparison and self-doubt as we constantly strive to attain an unattainable standard of perfection.

AUTHENTIC CONNECTIONS

By constantly trying to maintain appearances, we risk sacrificing authentic connections with our friends. True friendships are built on trust, empathy, and vulnerability. When we present an idealized version of ourselves, we deny our friends the opportunity to know us on a deeper level. Embracing our imperfections and allowing ourselves to be vulnerable fosters genuine connections and creates a supportive network of friends who accept us for who we truly are.

THE BIGGEST PROBLEM

The most significant issue arises when people live beyond their means, often by neglecting savings and accumulating debt. They can create the illusion of living a lifestyle they cannot actually afford.

Image Credits: unsplash.com

In conclusion, while the desire to keep up appearances with friends is understandable, it is crucial to recognize the toll it can take on our well-being.

It is essential to remember that true friendships are built on honesty, trust, and acceptance. Embracing our vulnerabilities and being our authentic selves will not only strengthen our relationships but also enhance our overall sense of well-being. Let us break free from the cycle of appearances and foster deeper connections based on genuine understanding and support.

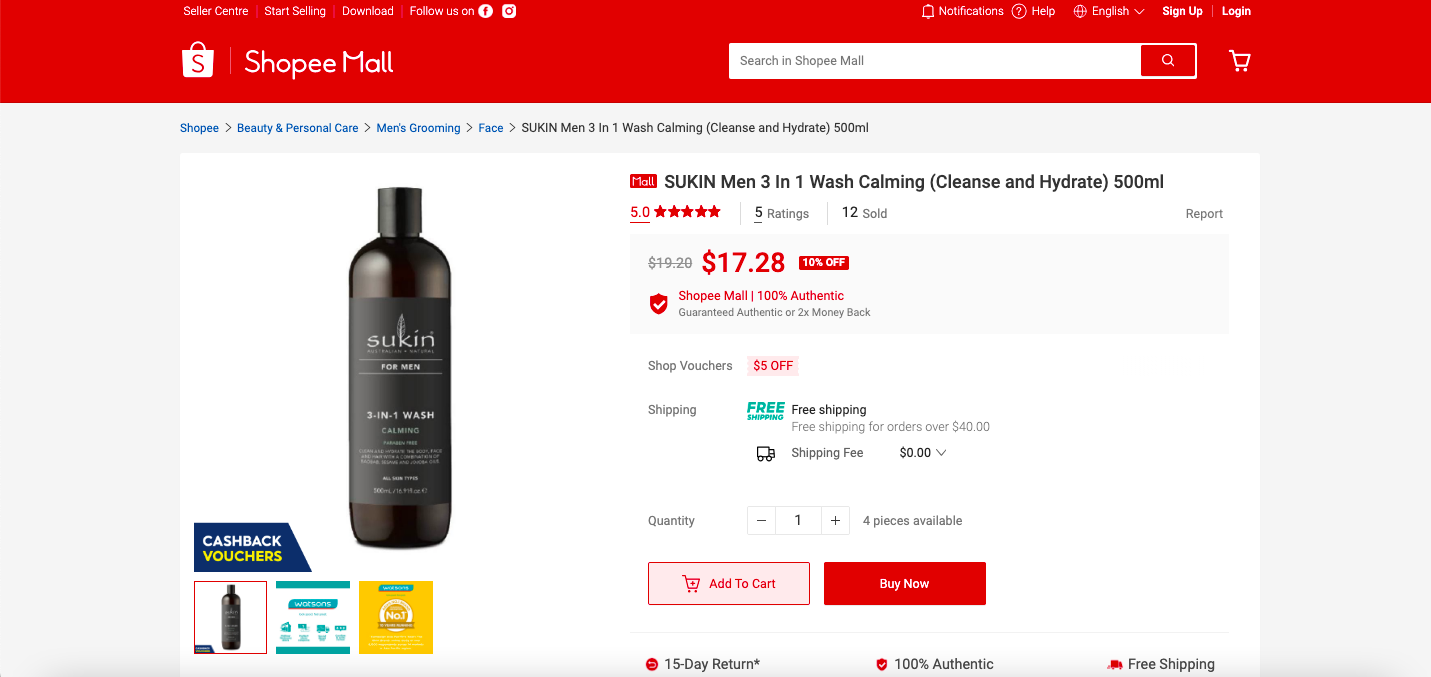

Long gone are the days when “atas” skincare is just for women.

Men’s skincare has come a long way, and it’s time to debunk the notion that it’s exclusively for women.

With a growing awareness of the importance of self-care and grooming, men are embracing skincare routines tailored to their specific needs.

So if you agree, allow us to introduce you to some affordable luxe facial cleansers, all under $33, that will leave your skin feeling fresh and primed.

First up, we have this multi-tasking product for the frazzled man on the go.

Infused with soothing aloe, hydrating baobab, and calming cedarwood, this 3-in-1 body, hair, and face wash helps you streamline your morning routine with just one bottle. The sesame and jojoba oils cleanse your skin without stripping away natural moisture, leaving it feeling hydrated.

Whether you’re dashing out the door for work or heading to the gym, this multi-tasking wash helps you get ready faster without sacrificing care for all skin types.

Next up, we have this 2-in-1 liquid cleanser and toner that removes deep-down dirt, oil, and residue for clear, refreshed skin that’s ready for a shave.

The oat and coconut blend gently dissolves pore-clogging impurities without stripping moisture, leaving your complexion feeling hydrated, smooth, and fresh. Chamomile extract helps soothe and calm while reducing signs of irritation.

A little of this formula goes a long way to cleansing skin thoroughly yet delicately, ensuring your face feels revived and renewed, ready for the rest of your day. And much better, in a travel-friendly size.

This rich, fine-textured 2-in-1 face wash and shaving cream cleanses, refreshes, and energizes your skin while removing dirt, oil, and debris.

The formula works up to a rich lather with small amounts of lukewarm water, gently cleansing and soothing inflamed skin thanks to camellia japonica seed extract with antioxidant properties.

An ideal product for your daily cleansing ritual, it transforms into a conditioning shaving cream that softens whiskers for that shaving routine.

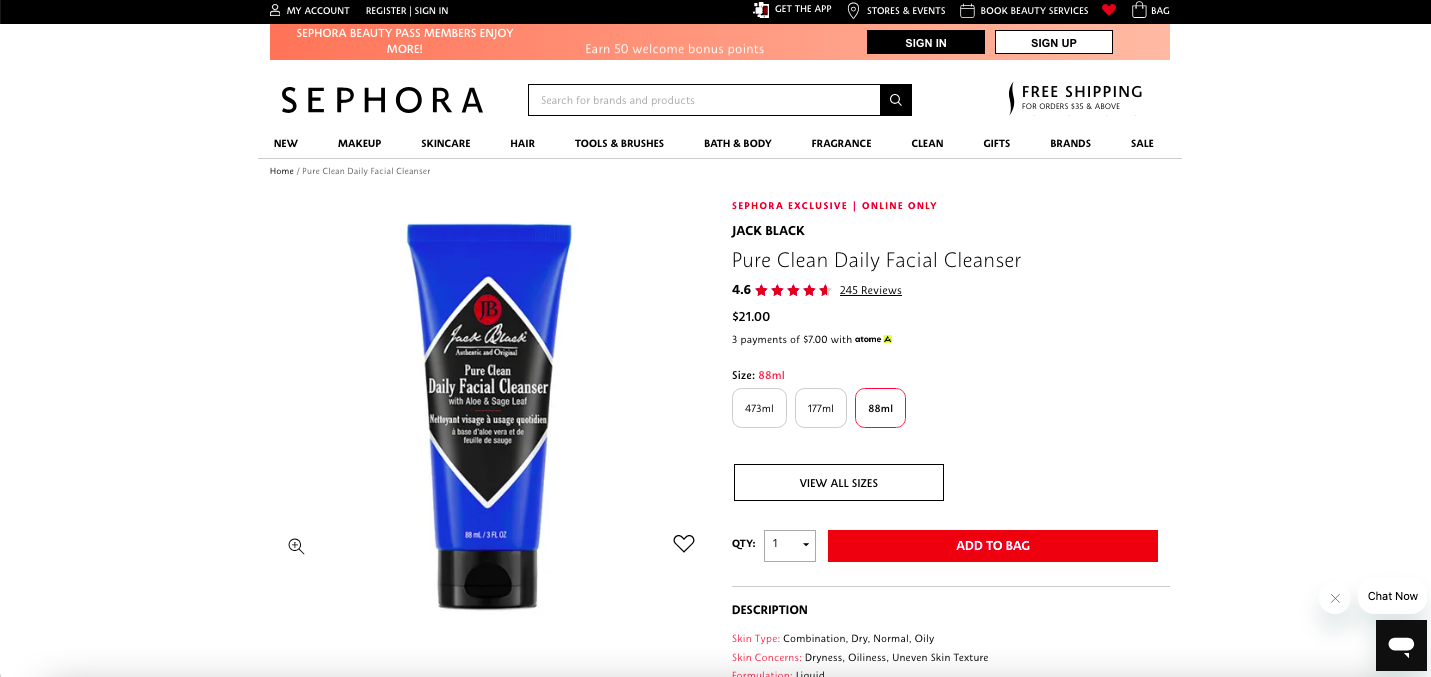

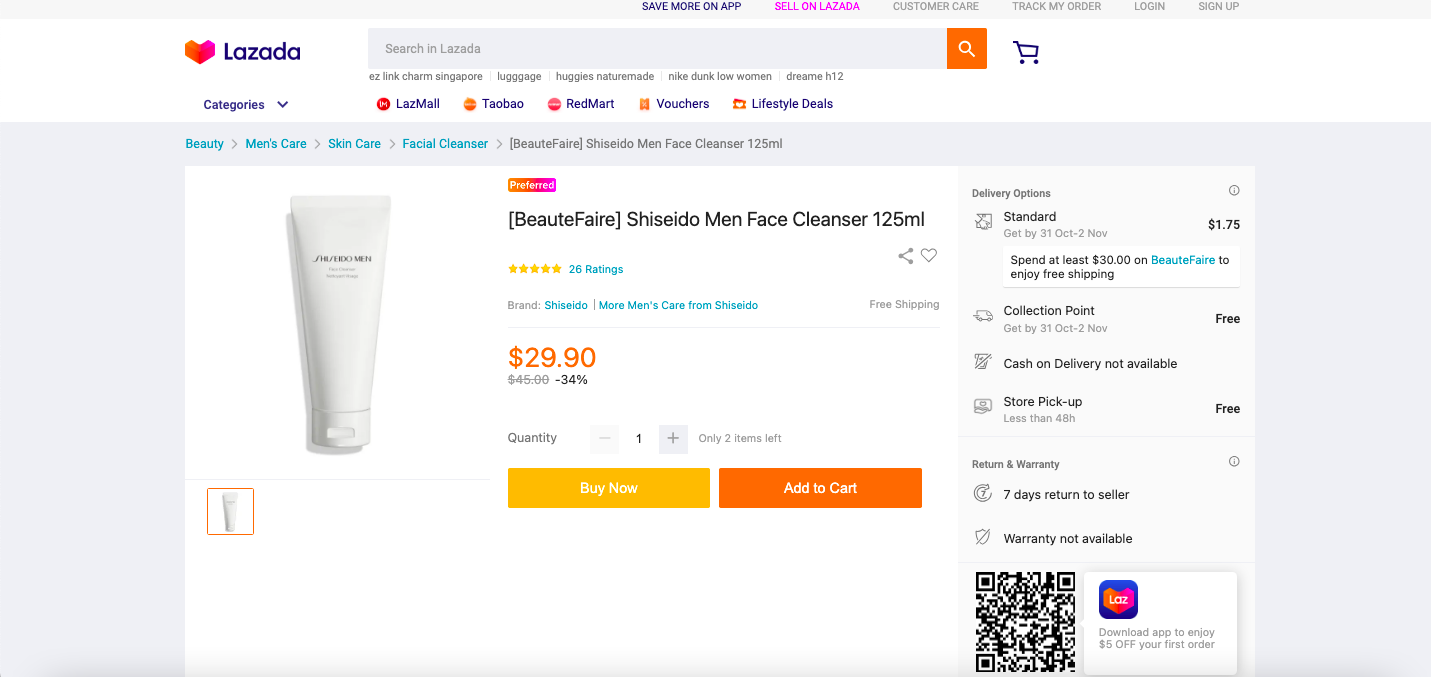

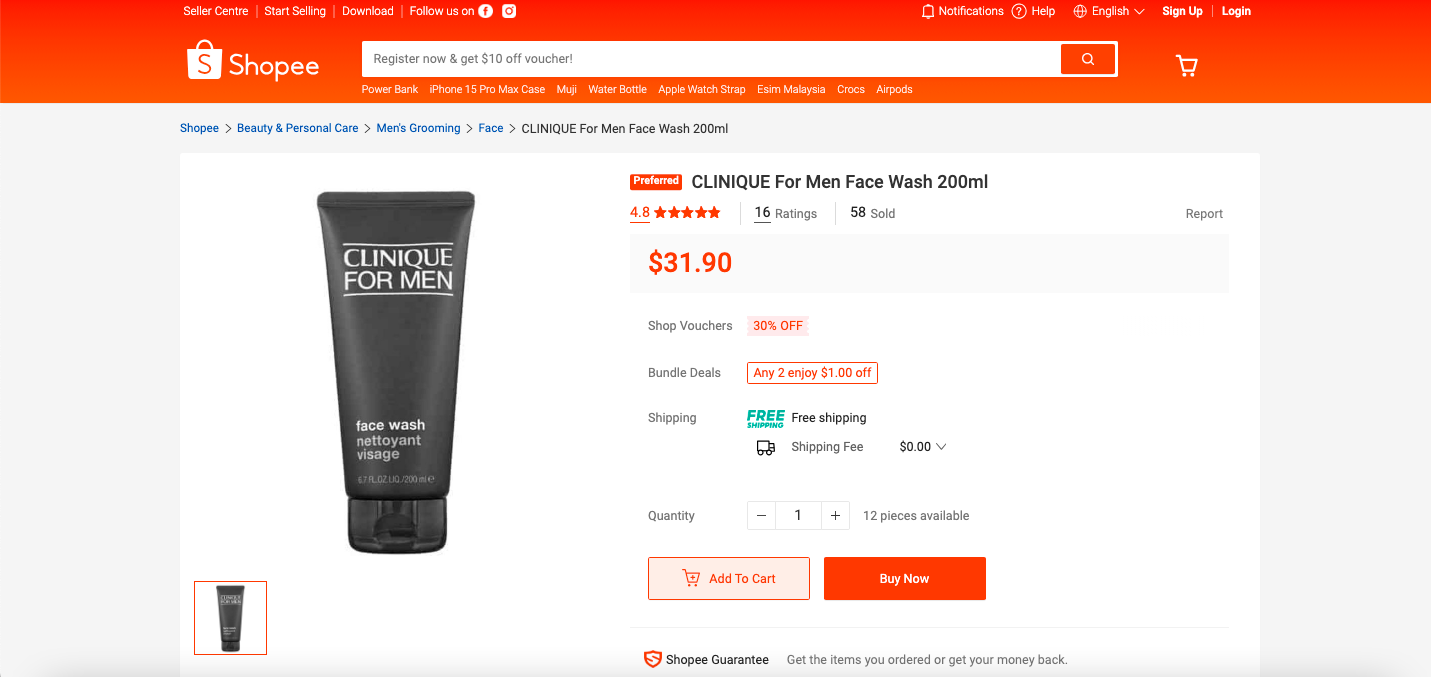

Last but not least, here’s a basic necessity for a comfortable shave—a gentle cleanser that preps skin without stripping away natural moisture.

This face wash from Clinique for Men thoroughly removes dirt, oil, and other pore-clogging impurities with ingredients like aloe barbadensis leaf juice that soothes skin with anti-bacterial and anti-inflammatory properties.

The formula leaves skin feeling fresh and ready for an irritation-free shave that’s soft, never tight or dry.

It’s time to prioritize self-care, gentlemen. These pretty affordable more “atas” facial cleansers offer a gateway to healthier skin. Remember, taking care of your skin is not about vanity; it’s a necessity. So start incorporating these luxe cleansers into your skincare routine and reap the benefits of healthy and glowing skin from today.