The SG Bonus was announced in Budget 2018 to share the fruits of Singapore’s development with Singaporeans. All eligible Singaporeans will receive hardcopy letter notifications on their SG Bonus benefit from 2 October 2018. Those who have registered their mobile numbers with SingPass will also receive SMS notifications.

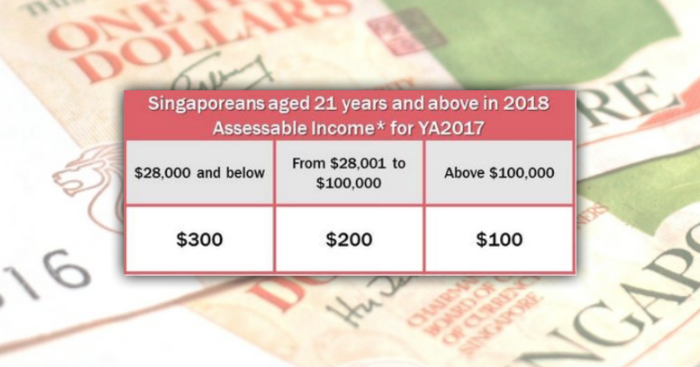

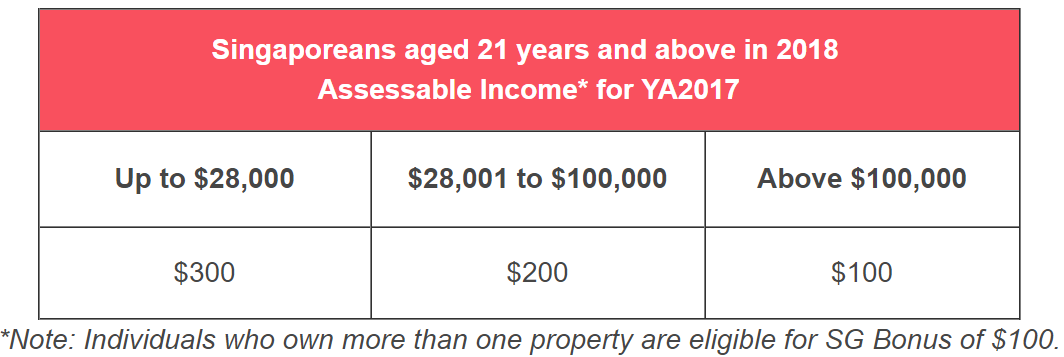

The amount of SG Bonus is tiered according to income, with more for those earning less:

SG Bonus will be paid to eligible Singaporeans in end 2018.

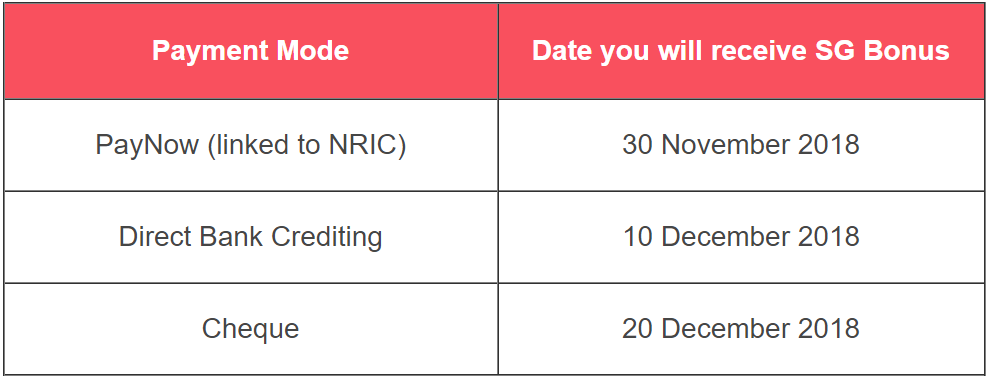

Citizens are encouraged to register their NRIC on PayNow by 7 November 2018 to receive their SG Bonus earlier (see payment dates below). They may do so via their bank’s mobile banking or Internet banking platforms.

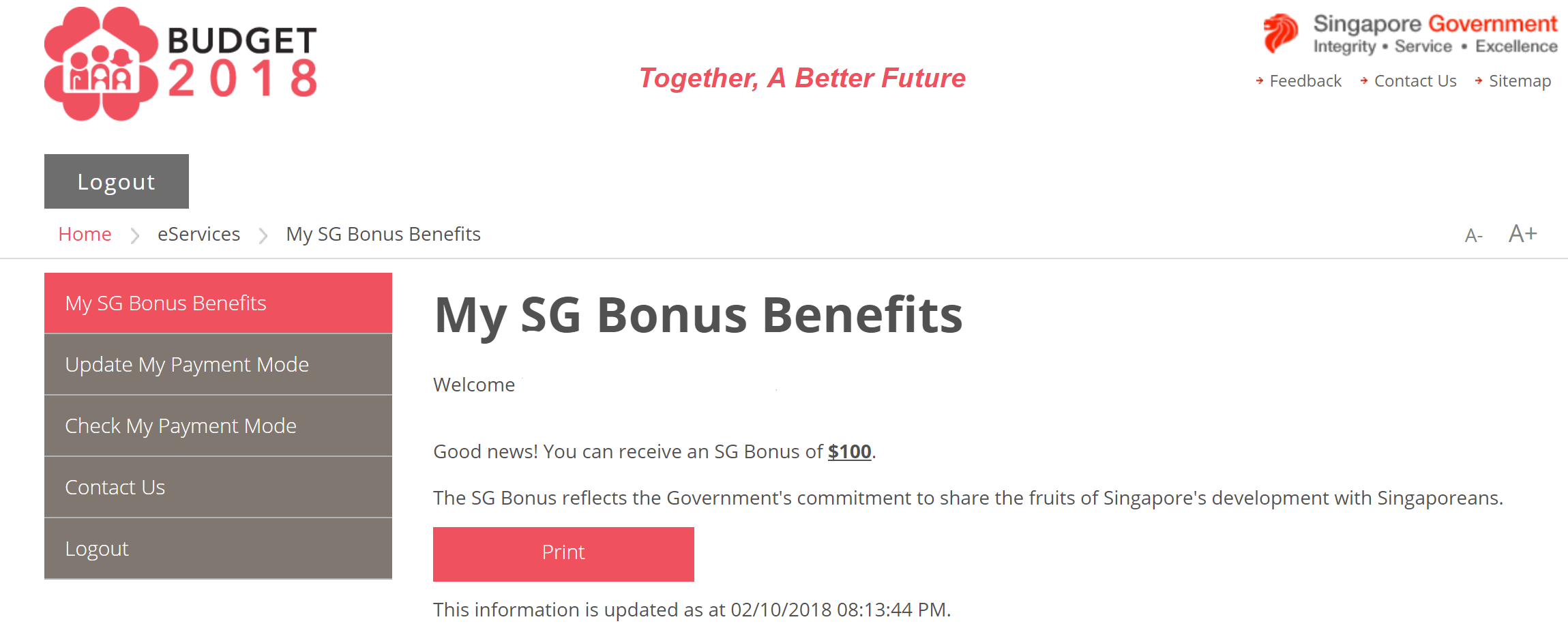

Log in to the SG Bonus e-Service (SingPass login required) to sign up for the SG Bonus, update your payment mode, or make a donation:

Purchasing health insurance can be a daunting task. It may be a tricky situation if your family member has cancer. Fortunately, you can make different choices that offer the best coverage for prescription drug and medical needs.

These cautions and suggestions will help you to shop for policy for your cancer treatment:

Plan Covers Your Clinics, Hospitals, and Doctors

Evaluate your plan if it includes a cover for doctors, hospitals, and clinics. Plans may change your preferred clinics, hospitals and doctors. If your plan is not covering your clinics and doctors, you have to change this policy. Doctors or hospitals out of network may increase your expense.

Plans like australian health insurance – iSelect offer special benefits to a policyholder. You have to do your homework to find out a reliable plan. Keep it in mind that high-deductible plans need you to pay 100% of medical costs until you mollify your deductibles. Deductibles can be more than out-of-network care.

Plan Cover Costs of Prescription Drugs

Some plans are associated with co-pay that is a fixed rate for the prescription of each patient. Other insurance plans may charge one co-insurance that is ideal for the total charges of a drug. It may be expensive for a cancer patient who undergoes multiple services like radiation therapy and chemotherapy for treatment. For cancer medications, a co-pay can be a cheap option than co-insurances.

Plans often divide medications as per formulary into categories or tier. The medicines in higher tiers can be expensive for you. Cancer medications are placed in the highest tier. You may compare every formulary to see the tiers/categories of your drug.

Effects of Step Therapy

Several insurers follow “fail first” or “step therapy” rules in healthcare policies. They necessitate patients to try cheap medications before offering coverage for drugs the doctors would prescribe. If initial medicines prove useless for a patient, the treatment may progress toward expensive therapies.

Advocates of patient and physicians are concerned that this therapy can delay the access to treatments offering maximum benefits. Therefore, they consider it wrong for patients. Several states have laws that permit doctors to apply or supersede these policies. If your state doesn’t enact this law, you can talk to the insurance company to know about their policies.

Work-based Insurance Plans

Several work-based insurance plans offer open enrollment period almost once in a year. It allows you to evaluate your health plans. You can add a new member of family or change plans to avail this opportunity. You may get an option to keep similar plans without any change. If you get an option to change plans, you must carefully evaluate new prospects and their way to cover the treatment of cancer patients.

Carefully secure copies of paperwork relevant to your claims, such as FMLA (family medical leave, sick leave, receipts, bills, EOBs (explanation of benefits and necessary medical letters. Maintain your records and send reimbursement bills to your insurance provider.

Unfortunately waving a wand will not help you to cut down your spending. Instead, here are some practical tips that you may start with!

#1: THE 30-DAY RULE

When you spot a tempting item from the mall, wait until 30 days before purchasing it. Write it down on a list of pending items. When a month has passed, cross out the items that you are willing to skip on. The only exceptions to this rule are groceries and other fixed expenses.

#2: WORKING HARD IS NOT AN EXCUSE

How many times have you purchased an item that you “deserve”? Yes! You may be using your hard-earned money to enjoy finer things in life. However, hard work should not be an excuse to spend. Income does not automatically increase as your workload expands! Your budget must outweigh your work stress.

#3: PLASTIC IS NOT FANTASTIC

Leaving your credit cards at home is one of the easiest ways to stop spending. Equip yourself with the amount of cash that you are willing to spend in a grocery store or a shopping centre. You can only bring your card with you if you are planning to pay off an item through an installment plan.

Image Credits: pixabay.com

Leaving these plastics behind will help you avoid the temptation of impulse purchases.

#4: SETTING SHORT-TERM FINANCIAL GOALS

As you alter your spending habits, setting realistic short-term financial goals is a great way to stay motivated. Having these goals will remind you of the reasons why you are making several sacrifices at the moment. It is important to be specific when it comes to thse goals as it will be easier to aim for. Instead of saying that you want to decrease your coffee budget, you may say that you will “decrease your monthly coffee costs from S$200 to S$100”.

#5: THE OPPORTUNITY COST

Lastly, re-frame your thoughts by looking at the brighter side of your goals. The technical term for this is opportunity cost. Opportunity cost is defined as “the loss of potential gain from other alternatives when one alternative is chosen.”

Image Credits: pixabay.com

Saving money and cutting back will give you an opportunity to reach your goals!

Technically speaking, all the monetary value that the deceased left behind belongs to his or her estate. This estate includes bank accounts, investments, and properties. The only exceptions are the assets held in the trust and the individual’s CPF money.

All the assets will be frozen once a person passes away. The professional assigned to go through the departed’s Will is known as an executor. An executor is usually a family lawyer or a trusted relative. He or she applies to be granted probate, which is a court order empowering the executor to settle all the remaining assets.

Say that the deceased did not make a legitimate Will and has an estate of about S$50,000. The surviving family members may go to the Public Trustee for them to divide the assets according to the Intestate Succession Act.

Image Credits: pixabay.com

This is why it is recommended to write your own Will while you are still alive. In fact, a straightforward online tool that can help you with that is called the WillMaker. It costs about S$89.

WILL YOU BE LIABLE FOR THE DECEASED’S DEBTS?

After the funeral costs are sorted out, the executor will liquefy the estate to pay off the deceased’s outstanding debts. Outstanding debts encompass the unpaid taxes, mortgages, credit card bills, utility bills, and so on. When the court is satisfied with all the debt payments, the remaining assets can be distributed to the beneficiaries according to the Will.

You are fortunate to know that the surviving family members are not legally responsible for the debts left behind by the deceased in Singapore. A surviving family member will only be held liable for the debts, if they have a joint loan account with the deceased.

Image Credits: pixabay.com

Now, let us move on to the HDB flat left behind. HDB homeowners have a signed a mandatory insurance known as the Home Protection Scheme (HPS). This insurance protects families from losing their HDB flats in the event of death, total permanent disability, and terminal illness. HPS insures members up to age 65 or until the housing loans are paid.

Though created differently, all credit cards have a limit. The credit limit dictates the maximum amount an issuer allows a borrower to spend on a single card. Ideally, your balance should fall below the limit. You see, maximizing your credit card can hinder you from making additional charges.

Employ these tips to ensure that you spend less than your credit card limit.

#1: TRACK YOUR SPENDING

It goes without saying that awareness of your spending habits will help you control your credit card usage. Monitor your billing statements by checking your balance in the bank’s online app or website. Staying on top of your spending will help you foresee any event leading up to going beyond your limit. Thus, you must adjust your expenses accordingly.

#2: CHECK YOUR BALANCE REGULARLY

Before making a purchase, check your available credit balance using your bank’s mobile app. If your credit card issuer does not have an online app, call the bank instead. You can find the contact details at the back of your plastic card.

Image Credits: pixabay.com

Doing so lets you determine whether you should postpone your purchase or to pursue the checkout counter on the spot.

#3: DO NOT INCREASE YOUR LIMIT RIGHT AWAY

Say that you have been constantly spending beyond your credit card limit. You may think that the logical step to take is to ask for a limit raise. However, asking for a limit raise within six months of receiving it can indicate that you are having financial difficulties. Issuers may be less willing to trust you with more credit.

Waiting for bank to automatically increase your credit limit is the best option. This way, you will be able to employ strategies dedicated to spending within your means.

#4: STICK TO THE THIRTY PERCENT

The easiest way to stay within your credit card limit is to provide a cushion. Keeping a cushion of about 30% of your actual credit card limit helps you avoid going overboard. For instance, Mary has a credit card limit of S$5,000. She must not swipe her card after hitting the S$3,500 mark.

Image Credits: pixabay.com

This threshold must apply to all of your credit cards and not just the banks you owe huge money too.