Gold prices have been on an amazing run in 2020. It has surged from USD 1,550 to reach USD 1,800 (Source: goldprice.org) in November 2020. Increasingly, investors also recognise the importance of having gold in their portfolios. When it comes to gold investments, investors are spoilt for choice since there are various platforms available in the market. We researched across the various platforms to determine the most cost-effective and efficient way of investing in gold.

Comparison of Various Platforms for Gold Investments

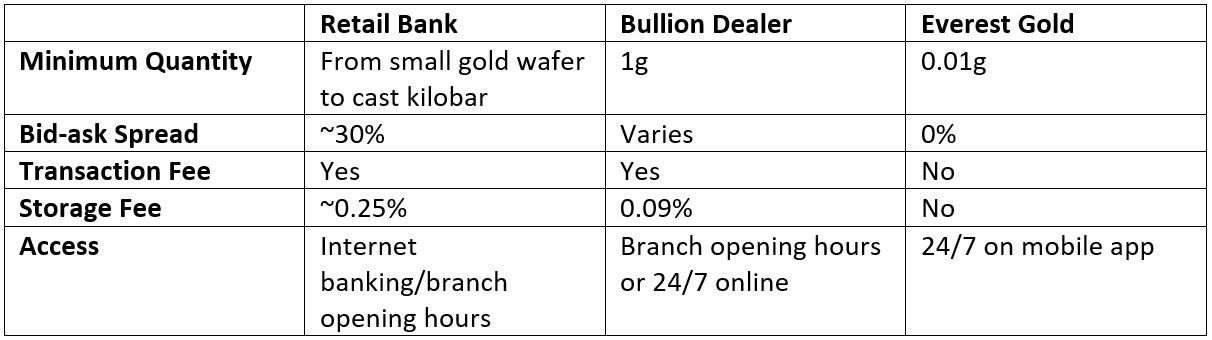

Here is a comparison of the common platforms available for gold investments on key metrics such as transaction fee, storage fee, etc.

Everest Gold

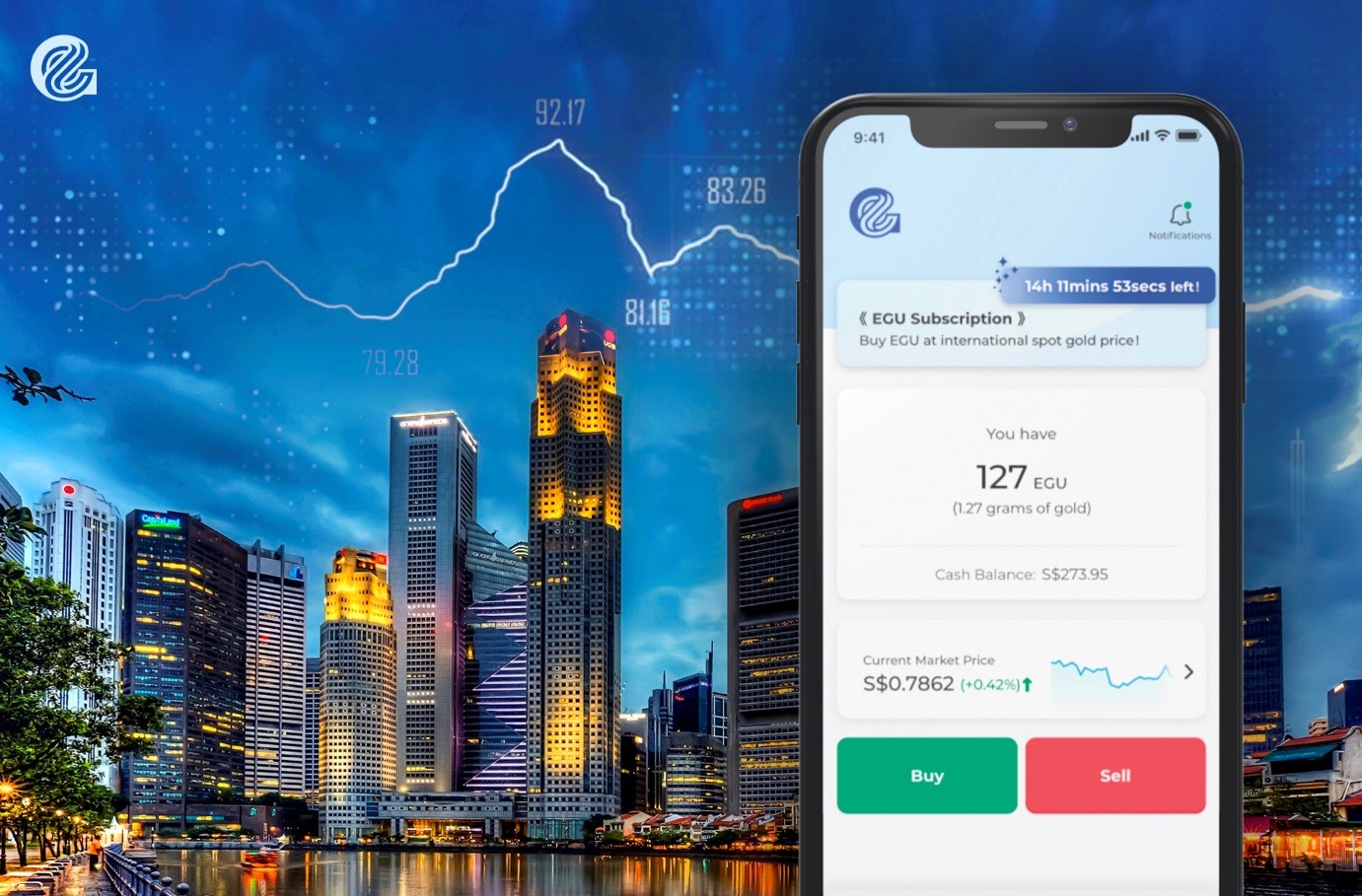

Everest Gold’s digital trading platform is the first-of-its-kind to introduce real gold bullions broken down into digital gold units called Everest Gold Units (EGUs), that allows gold investors to trade from as low as 0.01grams. Every EGU is 100% backed by real gold and matched on a 1:1 basis. Investors can accumulate their EGUs and exchange them for physical gold.

The minimum capital to trade starts from USD 0.60, the equivalent of 1 EGU, making it highly affordable for everyone. Moreover, its users enjoy fairer prices without paying high premiums commonly levied by retail banks. Fees are non-existent since there is no transaction fee and storage fee. The combination of no fees and fair price offers investors the chance to maximise their profits. This stands in steep contrast to transaction and storage fees typically charged by retail banks and bullion dealers.

Everest Gold platform is also highly accessible and allows investors to trade gold 24/7 on the mobile app. Such instantaneous liquidity is another attribute not usually offered by traditional retail banks and bullion dealers.

Everest Gold is available for download on Android, iOS and accessible from desktop.

Monopoly is a board game that has been causing family feuds since 1935. Monopoly was first marketed in 1935 during the Great Depression. It was an instant success and became a best-selling game in United States. Since then, over 275 million game sets were sold worldwide.

What is amazing about Monopoly is its ability to mimic financial scenarios in real life. On that note, here are four valuable real-estate and finance lessons that you can reap from the game.

#1: ALWAYS HAVE CASH ON HAND

In Monopoly, having cash enables you to purchase properties and pay fees for unlucky turns. You may need to shell out some cash to pay an opponent or to pay for a “Chance” card. It is important to always have cash on hand whenever you play. Do not spend all your money in one go!

In a similar way, you must spare some cash for unforeseen situations. The game teachers us about the importance of budgeting and saving money. You need to save enough money to cushion the blow of rough times, such as during this pandemic. Establish your emergency fund by identifying your current financial standing. It is best to build a fund that can cover about six months’ worth of your living expenses.

#2: DIVERSIFICATION IS IMPORTANT

Let us go back to the game itself. If someone lands on your property, you will earn money. Players usually buy multiple spaces or properties around the board to increase their chances of earning money. Chances of earning are slimmer if you only have a few properties on the board. The same can be applied in real life.

You need to diversify your portfolio and scatter it throughout the different possibilities in order for you to maximize your earnings. Instead of putting everything in a single basket, make sure to diversify your portfolio with bonds, stocks, and so on.

#3: PLAY THE LONG GAME

Being patient is essential whenever you play Monopoly. You see, the game continues until there is a last man standing (i.e., the other players have gone bankrupt). Much like the game, you are playing for the long haul. Meeting your financial goals is a journey and not a sprint.

Whether you are saving up for your 2021 vacation or your upcoming retirement, you need to be patient. There will a be a few bumps and celebrations along the way. For instance, you may pay off your student loans first before purchasing a car. Setting up a new business venture will also take time and involve a lot of ups and downs. Ultimately, your hard work will help you achieve your goals.

#4: EXPENSIVE IS NOT ENTIRELY THE BEST

The most expensive assets may not always be the best decisions. Most Monopoly players want to earn the Park Place and the Boardwalk since they have the biggest payouts. However, they are also the most expensive pieces to maintain. Many people lose at Monopoly by using this strategy because they do not pay attention to the overall cost. Instead, they only pay attention to the cash flow.

Image Credits: pixabay.com

Those who win at Monopoly are the ones who focus on the value gained for the price paid. You will not win by merely owning the most expensive assets. You will win by making the most money. In investing your money in the real world, you will win by selling high and buying low. Zeroing your attention to the most expensive assets may set yourself up for losses.

Aside from the explosion of rock music and big curls in the 80s, we were introduced to the cashless payment method called the General Interbank Recurring Order (GIRO). GIRO enabled its users to make convenient payments to billing organizations through their bank accounts. Since then, the digital cashless payment options have evolved dramatically. Nowadays, we can purchase items on online stores with a few taps of a button!

Let us get to know the nature and the examples of the e-wallets in Singapore.

HOW E-WALLETS WORK

Electronic wallets, e-wallets, digital wallets, or mobile wallets have taken over our lives in the previous months due to the effects of the global pandemic. E-wallets are virtual wallets, which are in collaboration with financial institutions (e.g., UOB or DBS), mobile service providers (e.g., SingTel), and international companies (e.g., Apple, Google, and Samsung). Many people have turned to cashless transactions to avoid carrying money or to avoid trips to the ATM.

E-wallets allow its users to store credit cards, debit cards, and loyalty cards into your device. Payments are made hassle-free as long as they are connected to your bank accounts or cards. Some e-wallets let you send and receive money through paperless transactions.

THINGS TO CONSIDER BEFORE USING AN E-WALLET

1. Which e-wallet do you want to get?

2. Does your preferred e-wallet have a maximum value that can be stored inside?

3. What is the expiry date for the money inside your potential e-wallet?

4. How much is the maximum value you can transfer out from an e-wallet per transaction?

5. Are there fees involved in top-up and other services?

POPULAR E-WALLETS IN SINGAPORE

1. Apple Pay

Apple Pay handles secure payment transactions between contactless terminals and Apple iOS devices. It can be used in 7-Eleven, Breadtalk, Giant, FairPrice, Uniqlo, and so much more.

2. SingTel Dash

Dash allows you to top-up your Singtel prepaid account or other Dash accounts to pay partner merchants in Singapore, Thailand, and Visa payWave partner merchants worldwide. You may pay online purchases through the Dash Visa Virtual Account and transfer funds within Singapore and to India, Indonesia, Philippines, China, Myanmar, and Bangladesh.

3. GrabPay

As the name suggests, GrabPay can be used to pay for Grab rides, GrabFood deliveries, and selected merchants with the GrabPay QR code. You can also use it with the GrabPay Card where MasterCard is accepted.

4. FavePay

FavePay is a quick and easy way to pay your favorite merchants and get instant cashback. FavePay accepts debit or credit cards (e.g., Visa, MasterCard, and American Express), GrabPay, Paypal, Boost Payment, and Air Asia Big Points. You can use the FavePay for selected merchants with the FavePay QR code.

5. AliPay

AliPay is a global payment platform with over 400 million users around the world. It is backed by the Chinese tech giant Alibaba and uses advanced encryption technology to ensure personal information and online payments are secured. It can be used to cover payments to ComfortDelGro and Prime taxis, Resorts World Sentosa, Metro, Singapore Zoo, Universal Studios, and more.

6. Google Pay

Google Pay is an online payment system developed by Google. It enables its users to pay for transactions with Android devices in-store and on supported websites. You can use it in-store at more than 80,000 checkout counters such as Cheers, Cold Storage, 7-Eleven, NTUC, McDonald’s, and Uniqlo.

7. DBS PayLah!

DBS PayLah! is a personal virtual wallet, which allows you to perform transactions such as Scan and Pay (NETS), funds transfer, QR Code payments, online purchases, and bill payments on-the-go. Discover its functions through the DBS PayLah! app.

8. NETSPay

NETSPay enables you to register your POSB/DBS ATM Card digitally. Once you have stored your cards, you may leave it at home and start paying with your smartphone. You can use this digital wallet to pay selected merchants in Singapore and Alipay Connect-enabled merchants in Japan.

9. EZ-Link Wallet

EZ-Link Wallet is personal mobile wallet within the EZ-Link app. You can use it to make payments conveniently at retail outlets domestically and overseas by scanning a QR Code or at an Alipay Connect-enabled merchant. Moreover, you can earn EZ-Link Rewards points for your transactions.

Image Credits: unsplash.com

Use these information to make thoughtful decisions when it comes to your e-wallet and online payment transactions.

This month, the Monetary Authority of Singapore (MAS) announced that it plans to discontinue the issuance of the S$1,000 notes from January 1, 2021. A limited quantity of this note will be made available each month from now until December 2020.

How will this affect you? What are the implications of this decision?

#1: SAFETY MEASURE TO REDUCE THE MONEY LAUNDERING RISKS

According to MAS, this is a pre-emptive measure to mitigate the higher money laundering and terrorism financing risks associated with large denomination notes. Large denomination notes allow people to carry significant values of money anonymously. The anonymity attached to these notes can be used to facilitate money laundering and other illegal activities.

#2: ELECTRONIC PAYMENTS ARE HIGHLY ENCOURAGED

To reduce your health and financial risks, it is best to use electronic payments whenever possible. MAS encouraged the use of electronic payments. Moreover, National University of Singapore’s Associate Professor and CGIO director Lawrence Loh highlighted that electronic payment systems are more secure than cash, despite the cyber-risks associated with online payments.

He said that: “You are able to secure two things with e-payments. Firstly, in terms of technical security, you can trace where your money is going, and secondly, you have physical security because you don’t have to carry large amounts of cash.”

#3: EXISTING S$1,000 NOTES IN CIRCULATION WILL REMAIN LEGAL TENDER

According to MAS, existing S$1,000 notes in circulation can still be used as a means of payment. They will continue to remain legal tender and can be used by the banks. To adapt to the upcoming demands of other denominations (particularly the S$100 note), MAS will make sufficient quantities of other denominations available.

#4: THE SELLING PRICE OF THE S$1,000 NOTE WILL LIKELY INCREASE

Currency collectors and dealers acknowledged that the selling price of the S$1,000 note will likely increase due to the limited supply of this note in the upcoming year. However, the currency dealers and collectors interviewed by TODAY have predicted that it will not increase dramatically.

You see, most people gravitate towards collecting notes of smaller denominations. For instance, a S$1,000 note from the orchid series (issued from 1967 to 1976) is worth around S$2,000. In contrast, a bundle of 1,000 S$1 notes from the same series is worth about S$12,000. It is amazing how these items have a S$10,000 difference in its selling prices!

#5: THIS MOVE IS ALIGNED WITH INTERNATIONAL NORMS

Renowned economists, including those from the International Monetary Fund, have advocated the phasing out of notes with large denominations to deter financial crimes such as corruption and tax evasion. This move by MAS is aligned with the international norms. For instance, European authorities stopped the printing of the 500-euro banknote last year.

The Supplementary Retirement Scheme (SRS) is a voluntary scheme to encourage individuals to save for retirement. Unlike the Central Provident Fund (CPF), it is not compulsory to participate in the SRS scheme. A key benefit of SRS is that members can enjoy dollar for dollar tax relief, capped at $15,300 per annum for Singaporeans while saving towards their retirement goals. As a tax deferral scheme, when you subsequently withdraw from your SRS after the statutory retirement age, only 50% of the amounts withdrawn will be subject to tax. Individuals who would like to open an SRS account can do so with either DBS, UOB or OCBC bank.

Don’t leave your funds in SRS un-utilised

After transferring funds into your SRS account, don’t leave it un-utilised! According to Ministry of Finance (2019), over 28% of SRS contributions sit idle as cash balances, earning a low interest rate return of only 0.05% p.a.

There are many ways that you can utilitse your SRS contributions to grow your retirement funds, such as investing in unit trusts, ETFs, stocks, bonds (including Singapore Saving Bonds and Singapore Government Securities) and single premium insurance. A particular affordable and convenient way is to invest your SRS funds with MoneyOwl to boost your future retirement fund. Here’s why you should do so.

Invest your SRS with MoneyOwl

Investing your SRS funds with MoneyOwl starts from as little as S$50/month or $100 as a lump sum. This means that it is possible to start early without waiting for your SRS funds to accumulate to a substantial level. Besides, there is no platform fee so that more wealth is generated for the you in the long run. With MoneyOwl, you gain access to a globally diversified portfolio of companies with good growth potential at value prices.

This promotion is only valid from 9 November to 31 December 2020.

This promotion is only open to the first 500 people who successfully invest their SRS funds with MoneyOwl.

Promotion is valid for one-time top ups using SRS funds only. Regular savings plans/ monthly SRS investments are not eligible.

Promotion is not valid for cash investments and investments in WiseSaver portfolio.

You need to stay invested and not withdraw your funds for at least 2 months after the promotion period is over (i.e. till end-February 2021). Vouchers will be sent to you in March 2021.

Only new MoneyOwl clients are eligible for S$50 voucher redemptions.

Both existing and new MoneyOwl clients are eligible for the $100 or $200 voucher redemption.

MoneyOwl reserves the right to change these terms and conditions from time to time.

About MoneyOwl

MoneyOwl empowers and fulfils lives by helping people make wise decisions to achieve their financial goals. With one of the lowest fees in the market, invest your SRS funds with MoneyOwl today to boost your future retirement income.