The Singapore dollar has hit an all-time high against the euro yesterday (Jul 12).

The Singapore dollar reached a record high of S$1=€0.71 (or €1 = S$1.41) on Tuesday, up about 9% since the start of the year. Fear that an energy crisis in Europe and the war in Ukraine will plunge the region into a recession has caused the euro to depreciate. The slide of the euro also saw that it reaches parity against the US dollar in two decades.

Source: European Central Bank

According to historical data, the last time the Singapore dollar hits €1 = S$1.41 was back in February 1985.

To fight inflation, Singapore has adopted an aggressive monetary policy by appreciating the Singdollar. The stronger Singapore dollar also saw that it strengthen against several currencies in the region including the Malaysian ringgit (S$1 = RM3.15), Thai baht (S$1 = THB25.72) and the Indonesian rupiah (S$1=10,637 IDR).

Retirement may make it tricky to adjust to life in general, notably if you have always been on a tight budget.

You don’t automatically have to stop paying your bills and keep up with house maintenance just because you’ve entered the next phase of life. In fact, it’s more crucial now than ever to allocate additional expenses for outings to the country club or for relaxing holidays.

Now’s the perfect time to employ your knowledge in personal finance if you’re thinking of retiring! Here are several tips to help you stay frugal during your golden years.

Define your goals and budget

First, you need to define your goals and budget. What do you hope to achieve in retirement, and how much money do you need to make that happen? Once you have a firmer idea of what you’re working with, you can start brainstorming ways to save.

Next, take a look at your regular expenses and see where you could cut back. Maybe you don’t need that expensive subscription plan anymore, or maybe you can start brown-bagging your lunch instead of eating out every day. Paring down your expenses will free up more money to save for retirement.

Bonus advice: One of the smartest things you can do for your retirement savings is to invest them. Investing allows your money to grow over time, so you can comfortably retire without having to worry about finances. There are many diverse types of investments available, though, so talk to a financial advisor to figure out which one is best for you.

Invest in quality over the price tag

When it comes to spending your money during retirement, it’s essential to invest in quality over the price tag. Sure, you may be able to save a little bit of money by buying the cheapest version of something, but in the long run, you will be much better off if you spend a little bit more and purchase something that’s going to last.

For illustration, instead of buying the most inexpensive watch available, invest in a quality timepiece that will last for years. Likewise, rather than opting for the most affordable clothing options, choose well-made pieces that will resist wear and tear. By spending a little bit more upfront, you will avoid having to constantly replace items and will be able to stick to your budget much more efficiently.

Seek free or relatively low-cost activities

Image Credits: lionraw.com

When you retire, it’s important to find ways to stretch your dollar. One way to do this is by seeking free or low-cost activities. There are several things you can do to keep costs down.

For example, you can take complimentary online courses, visit museum exhibitions with free admission or participate in meetups and group activities. You can also save money by cooking at home and avoiding expensive restaurants. Whatever you do, make sure that you’re budgeting wisely and that your retirement expenses don’t put too much stress on your budget. Retirement should be a time of joy and relaxation, not financial worry.

Get creative with your living situation

One way to save money during retirement is to get clever with your living situation. For instance, consider downsizing to a smaller home or moving to a less expensive neighborhood. You could also consider sharing a home with a friend or family member or renting out a room in your house.

Another way to save money is to be mindful of your spending habits. Try to avoid buying unnecessary items and be conscious of the things you do spend money on. There are many ways to be economical without having to deprive yourself of the things you enjoy. It just takes a little bit of restraint and inventiveness.

Learn to cook and enjoy meals at home

Image Credits: straitstimes.com

One of the wisest things you can do to save money during retirement is to learn to cook and savor meals at home. Not only will you save a ton of money on delivery food, but you will also have the satisfaction of knowing that you made your meal from scratch. Here are a few suggestions to help get you started:

Try no-frills recipes that are effortless to follow and don’t require a lot of ingredients.

Browse cooking blogs for inspiration, or take a cooking class at your nearest community center or a cooking school.

Invest in some quality kitchen utensils and equipment. A fast blender, for example, will make cooking much more pleasurable.

Be creative and experiment with distinct flavors and ingredients. You might be pleasantly surprised at what you can come up with!

Being thrifty and living within your means is more paramount now than ever when you’re retired. But keep in mind that a thrifty way of living values conserving money as effectively as possible and is cost mindful. It’s critical to assess your financial situation in retirement and determine whether being frugal is a good match. It should not be thought of as a punishment to be thrifty since it can be financially empowering in the long run. Strive to maintain your retired lifestyle while keeping within your budget by considering the advice provided in this article.

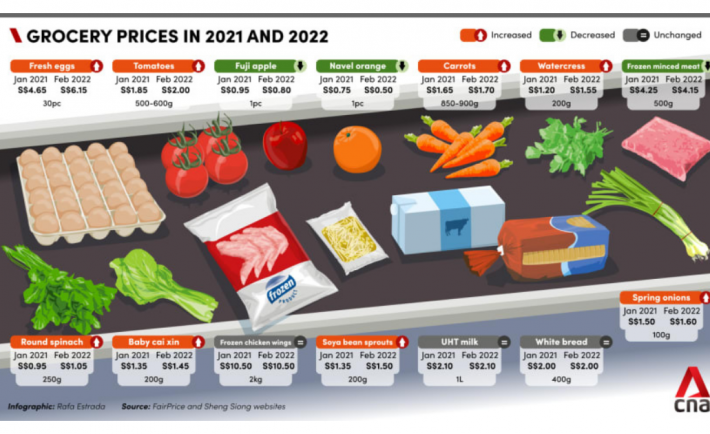

You may have noticed prices going up for the everyday items you buy. This is because we are now experiencing inflation.

For folks who have been following the news, you would have come across the revelation that core inflation in Singapore has reached its highest level in more than 13 years in May 2022, driven mostly by increased food and utility prices. While some people may be struggling to get by, there are ways to thrive during times of inflation; you just need to know what they are.

In this post, we will share with you tips on how to thrive during times of inflation.

What is inflation?

Inflation is an economic term that refers to rising prices of goods and services in a country. This can be caused by a variety of reasons, such as an increase in the money supply or an increase or decrease in the value of the currency. If you’re feeling the effects of inflation, don’t worry – you’re not alone. Keep reading for tips on how to thrive, not just survive, during these challenging times.

How can you thrive during inflation?

There are a few key ways to thrive during inflation.

Get the best value for your money. Compare prices before you buy and avoid purchasing things on impulse. If you can’t afford something, wait until you can.

Use your money in the most efficient way possible. Make a budget and stick to it, even if it means making some sacrifices. Try to save money wherever you can, and invest in things that will hold their value over time, like gold.

Diversify your income. If all of your eggs are in one basket, you’re going to be in trouble if that basket starts to wobble. Spread your money out into different investments, and always have a backup plan in case of emergencies.

What are some things to avoid during inflation?

Image Credits: todayonline.com

There are a few things you should avoid doing during inflation to make the best of the situation. For one, don’t overspend. Just because prices are going up doesn’t mean you have to buy everything that’s in sight. Try to be mindful of your budget and only buy what you need.

Also, avoid taking on additional debt. When prices are rising, it’s easy to get swept up in the hype and go into debt buying things you don’t need. But remember that you will be paying back that debt with inflated dollars, so it’s important to stay away from high-interest loans and credit cards.

Finally, avoid hoarding. It can be tempting to stock up on things when you know they’re going to become more expensive soon, but this can do more harm than good. Not only will you end up spending more money in the short term, but you will also be sacrificing storage space at home.

What should you do if your income doesn’t keep up with inflation?

If your income doesn’t keep up with inflation, you’re not alone. So what can you do to make ends meet? Here are a few tips:

Ask for a raise at work or find a new job that pays more.

Live within your means and don’t succumb to social media pressure.

Review your expenses and see where you can make adjustments. Maybe you don’t need that expensive subscription anymore or you can start cooking at home more often.

You may be feeling the effects of inflation in your everyday life. Prices for utilities, groceries, and transportation continue to go up, and it sometimes feels like there’s nothing you can do about it. But don’t worry, the tips we’ve put together in this article will help you thrive during these tough times. Hopefully, you will be able to manage your expenses better and make the most of your money. So what are you waiting for? Start putting these suggestions into action today!

Congratulations on starting your financial journey! Creating a budget and sticking to it is no easy feat, but it is the best way to manage your finances and ensure that your money is going toward the expenses that matters most to you and your family.

Start by determining why you want a budget. Deciding on a budget can help you make informed decisions. Budgeters are almost twice as likely to report no financial worries compared to spenders. Moreover, budgeters are less likely to struggle with finances. Common reasons to create a budget include: to save more money, to reduce overspending, to eliminate couple financial disputes, to get out of debt, to break the paycheck-to-paycheck cycle, and to achieve goals.

After determining the reasons why, you want to create a budget, you must go deeper into your current spending habits. What are your spending habits as an individual and as a family? If your budget is not realistic, it is useless. Most experts recommend tracking your spending for about a month to get a clear picture of your spending habits.

The next step is to identify your financial goals. A great framework to use is the SMART method. It stands for Specific, Measurable, Achievable, Relevant, and Timebound. For instance, you want to save S$3,000 for home renovation within six months. You will need to save about S$500 per month. Thanks to your budget, you already know that you will have an excess of S$750 per month. This will help you with your goal!

Once you have your financial goals down, decide how much you need to save (per month or per year) for each goal. Bigger expenses such as home renovation and debt repayment can take a longer time to build. You can also incorporate building an emergency fund into your budget.

The basic phases are done, and it is time to make a budget. There are many types of budgets, so you will have to choose the one that suits you best. Options include zero-based budget and 50-30-20 budget.

A zero-based budget is an approach popularized by Dave Ramsey. It involves making income minus outflow equate to S$0. With a zero-sum budget, every dollar you have is assigned a task, with some of those going into savings or other spending categories. This type of budget can be restrictive, which is not ideal for everyone.

Image Credits: pixabay.com

The 50-30-20, on the other hand, divides your budget into different percentages. 50% of income is allocated toward needs, 30% to your wants, and 20% to your savings. Do your research to help you decide which budget method will make sense for you.

Starting a family requires careful planning. With a clear idea of what it entails and the schemes available to help ease new parents’ financial load, you will be able to embrace one of life’s greatest blessings.

As you allocate your budget, you must consider both your childcare expenses and your retirement fund. Prioritizing these two is easier said than done. A 2021 study by AIA Singapore revealed that young families in Singapore have deprioritized planning for their retirement to give way for the monthly expenses on their children.

The participants of the study (i.e., parents) were found to be spending 2.5 times more money on their children’s monthly expenses, rather than taking charge of their own retirement planning. These Singapore parents spend almost 20% of their income on their children’s needs and allocate less than 7% on their retirement fund. Furthermore, 70% shared that they intend to either increase or maintain the amount of income allocated to their children’s expenses. The increase of allocation to the children’s expenses is affected by the higher childcare costs amidst the pandemic.

Apart from this, the pandemic also affected their savings. One in three Singaporeans’ savings was negatively impacted in 2020, with a median amount of between S$251 to S$500 set aside monthly for retirement. It is challenging to find a balance between all the primary categories of your budget, but you must not overlook the importance of retirement planning.

“Retirement planning is an essential part of securing our longer-term financial security, not just for parents, but for the entire family, so everyone can look forward to a brighter future with peace of mind,” said Melita Teo. Melita Teo is AIA Singapore’s Chief Customer and Digital Officer.

As parents, you want to support your children by giving them the best opportunities to secure their future. Hence, you must consider creating a retirement plan to help navigate your seamless transition to the golden years. With this retirement plan, you will not need to fully rely on your children.

Start by reviewing your financial situation and financial plans. Establish a fresh budget for your household that will accommodate both your childcare costs and your retirement fund.

Talk to professionals, your trusted friends, and family members to have an idea of what it costs to pay for your child’s needs and your personal retirement needs.

Image Credits: pixabay.com

Research on various government schemes such as Enhanced Baby Bonus, Enhanced MediSave Grant for Newborns, and other subsidies for center-based infant and childcare. Newborns who are registered as Singapore Citizens at birth are automatically insured under MediShield Life. These schemes and benefits can help free up some of your expenses to boost not only your childcare budget, but also your retirement fund.