(Photo Credit: Alan Cleaver, via Flickr)

(Photo Credit: Alan Cleaver, via Flickr)

Congratulations. You have just tied the knot, moved into your new house and plan to start your own family. What’s next?

You have also acquired the debts and liabilities of having a mortgage to service and a family to feed.

Now the most important question daunt you. What happens if an unfortunate event renders you and/or your spouse incapacitated? Imagine a pillar that gave way and cause the entire building to collapse. It will be a disaster for that to happen.

How do you address that then?

You need another pillar to support the building. Insurance is the key – the third pillar. Getting yourself covered is the most responsible thing you can do for the family.

What are the different type of insurance?

There are many types of insurance in the market and knowing which is the most appropriate for you is an important financial decision. There are two main types of life insurance.

1. Term Insurance

2. Whole Life Insurance

Term insurance, as the name suggests, covers you for a term period you define. It can be as short as a yearly renewable term or it can cover you all the way until you become a centenarian.

Whole life insurance covers you for the entire life. The key difference is there is no cash value for a term plan as compared to whole life insurance.

The question now boils down to if you should get term or whole life insurance or a combination of both?

Term versus whole life insurance

Whole life insurance might seem attractive with a guaranteed cash value being paid out should you decide to surrender the policy later in the policy years. It seems like a no-brainer then – to get whole life insurance rather than a term policy that expires with no cash value. At least, that’s what many financial planners out there are advocating. Why pay to rent a house (in this case, purchasing term insurance) when you can afford to pay for the house and own it (purchasing whole life insurance)?

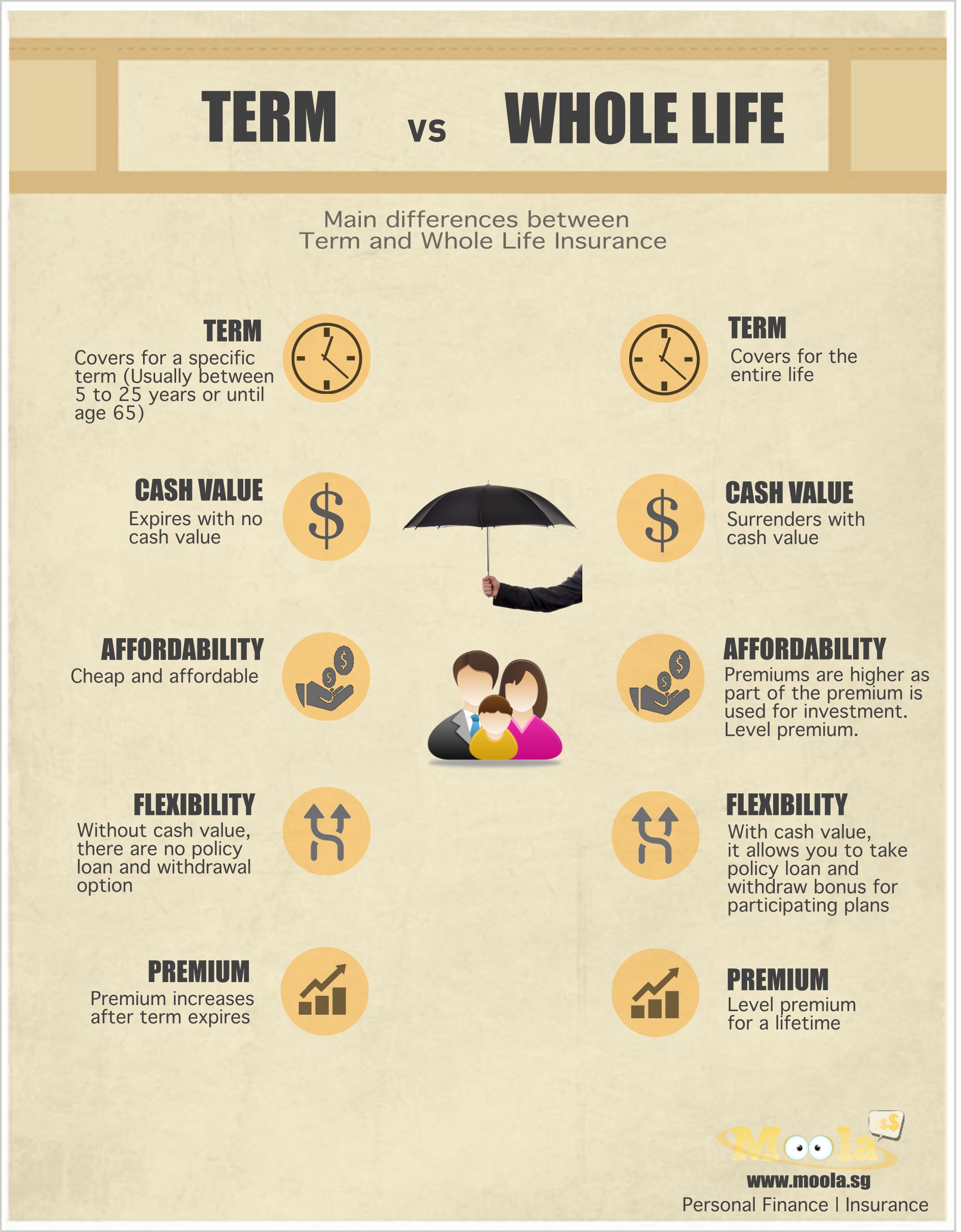

First, here’s a nifty infographic that put them side by side to show you the main differences.

Now after understanding how both products work, let’s place both of them side by side and examine them.

Let’s assume the following scenario:

Paul, a 25 years old male who wishes to get covered at $100,000 sum assured for death, terminal illness and disability. He also wants to accumulate some cash for retirement.

There are two options he can consider:

1) Buy a whole life insurance that can meet both needs; or

2) Buy a term insurance and invest the difference in other assets

1) Buying a Whole Life Insurance

It will costs him $112/month to get a $100,000 cover for death, terminal illnesses and disability. Should he retires at 55 years old (30 years later), he can choose to surrender the policy with a guaranteed cash value of $28,646 together with a non-guaranteed portion of $30,142 (using a bonus rate of 4.75%) – having paid $40,170 in premiums altogether.

Not too bad isn’t it? Even if the economy has taken a beating and Paul doesn’t get the guaranteed portion of $30,142, he still gets back $28,646. Then the outlay for his protection would cost him $11,524 over 30 years. Well, no free lunch in this world, so the question is if it is justifiable for him to pay that amount for insurance?

a) Yes, it is reasonable to pay $11,524 for protection over 30years. Furthermore, it only costs him around $384/year.

b) Some may also argue that there is still a possibility of him getting some of the non-guaranteed portion and even have the chance to make a ‘profit’ of $18,618.

Wait..

Let’s take a look at the second option and see how it matches up.

2) Buying Term Insurance and investing the difference

A similar term cover for Paul would cost him $12.80/month under the SAF Group Term Life insurance. That adds up to $153.60/year. It covers Paul for 30 years and it expires without cash value when he is 55.

The difference of $99.20 as compared to the first option can be invested into other assets such as STI ETF which has return 7-8% for the past 30years.

Assuming a 8% growth, Paul would have accumulated approximately $147,843.66 when he is 55 years old. Now contrast that with the first option of a guaranteed $28,646 plus a non-guaranteed of $30,142. The difference is huge.

Even if Paul is more conservative and expect a growth of 4%, he should be expecting a cash value of $68,849.90 after 30 years.

Wait, isn’t it non-guaranteed as the first option? But hey, Paul has the full control and flexibilities on when he can liquidate his invested assets should rainy days come.

We have our winner: Buying term insurance and investing the difference is the way to go!

And if you are still not convinced, Suze Orman says it all.