Say you are a breadwinner to a family of three. You are happy to sustain the needs of your family. Suddenly, you caught the coronavirus bug. What will you do? You can no longer go to work! You cannot fulfill your work from home duties either.

Fortunately for you, you decided to purchase a life insurance policy prior to this event. Your critical illness is covered. Apart from that, how can life insurance help you in the future?

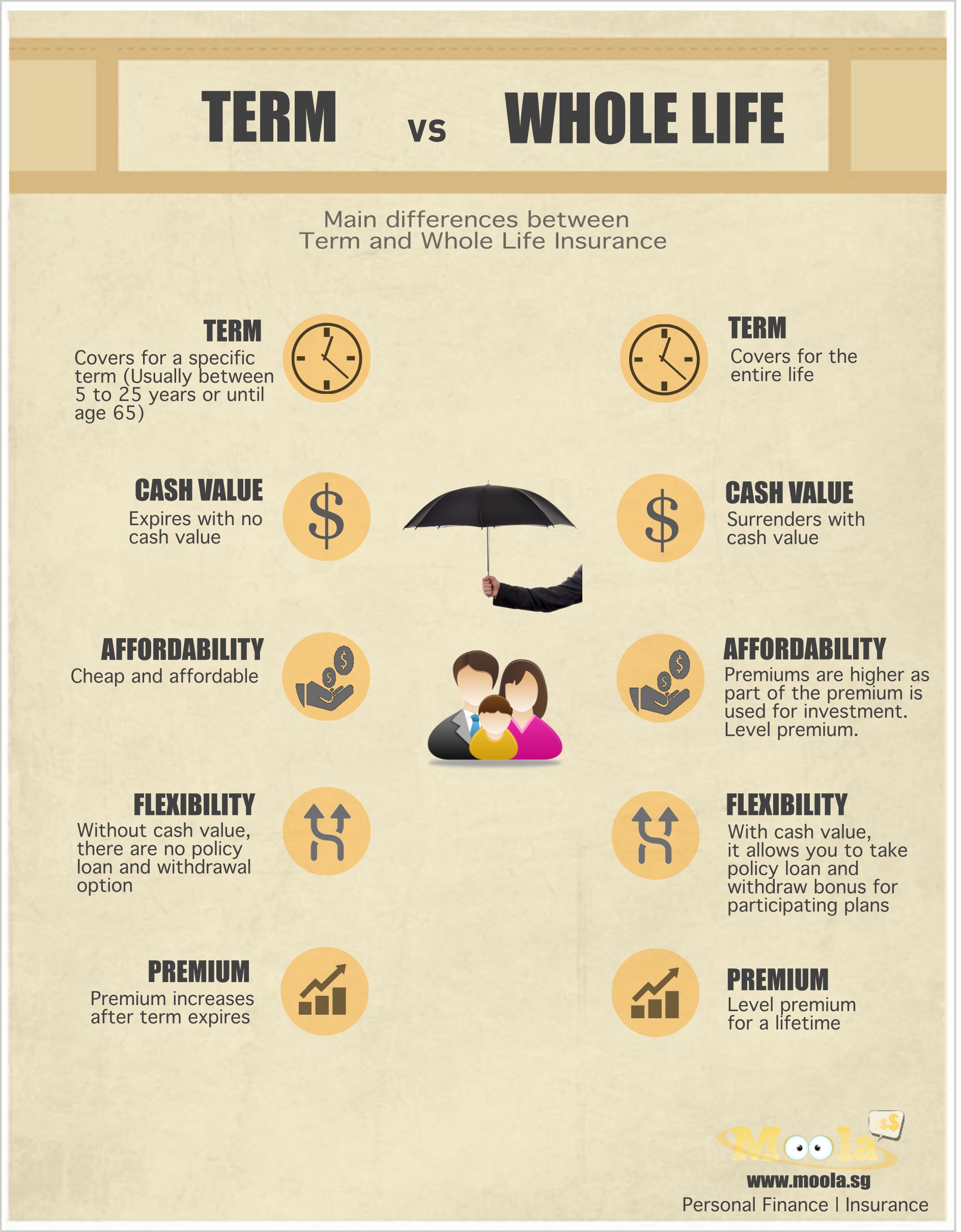

Firstly, there are two types of insurance such as whole life and term insurance. The latter is cheaper than the former. I will get to that later. Nonetheless, life insurance serves as your protection for unforeseen events, your shield for medical emergencies, and your extend relief after retirement.

The difference between whole life and term insurance is the amount of money you will have to put inside and the amount of money you will get back. Both policies provide protection in the event of total permanent disability and death.

Term insurance, true to its name, provides you with protection only for a fixed period of time (such as 20 to 30 years). The plan expires after the given term. If nothing happens to you and you do not make the claim, you get nothing. On the other and, whole life insurance covers you until you die. This is as long as you pay your premiums.

PROTECTION FOR UNFORESEEN EVENTS

Ensure that you will be able to support the needs of your surviving family with life insurance. When the income earner dies, there is a significant impact for the surviving family. There are possibilities when a survivor can provide for the rest of the family’s needs as well, but it is better to be prepared.

Keep the impact of death to minimum and provide your surviving family members with a source of income by arranging your life insurance plan.

SHIELD FOR MEDICAL EMERGENCIES

Whether you are single or married, having an emergency fund is vital to your life. You will never know when bad events such as this pandemic will occur.

Getting life insurance and having emergency funds are the best way to be ready for any emergencies. It will not only assure you but it will also prevent you from having an empty pocket when you drown in an unfortunate situation.

Some people might say that getting life insurance is like getting ready for your funeral. However, you may look at it as a means to prepare yourself for survival.

RELIEF FOR RETIREMENT

Using the cash value of your life insurance policy allows you to have an additional financial support once you retire.

Image Credits: unsplash.com

You may also use this money to indulge yourself, after you retire. Just ensure that you work within your means.