There is a huge difference between being late due to family emergencies and being late because you were queuing at Starbucks. Your constant trips to your “coffee haven” can drain your wallet. So, how do you keep your thirst for the daily coffee grind? With clever planning, of course! Try these tried-and-tested hacks to satisfy your coffee addiction:

#1: SHARING IS CARING

While I was chatting away with a friend of mine, our conversation drifted to her pleasant date. She and her mom shared a Venti cup after countless hours of shopping. You see, splitting a Venti cup is cheaper than purchasing two Tall or two Grande cups. Let us take the “Frappuccino” as an example. A Venti frap costs about S$7.60 while, a Tall frap costs about S$6. Splitting the bill with a friend can help you save up to S$2.20 each! Isn’t that what friendship is for?

Image Credits: pixabay.com

If you are planning to kill time in Starbucks, it is better to opt for the largest size available. Situations such as working on a school project with your classmate or finishing a business proposal call for this strategy!

#2: REAP THE REWARDS

One of the quickest ways to enjoy discounts and freebies is by joining the Starbucks Rewards Program. Upon entering, you will be eligible earn a star for every dollar spent. These stars equate to specific benefits such as a free slice of cake or a free drink. To get started, you must acquire a gift card. Register it thru the Starbucks website or thru the mobile app.

Use the app to stay updated with the latest promotions. What I like most about this loyalty program is the value given to one’s birthday month (i.e., by giving a free slice of cake, a free drink, or a free drink upgrade). Furthermore, you can get a personalized gold card. It is an ultimate Starbucks addict collectible, if you ask me!

#3: BRING A CONTAINER

An easy way to save at least 50 cents on your next order is by bringing your own container! Take out your favorite mug, tumbler, or water bottle from the shelf. Then, confidently offer your own container to the Starbucks barista.

Getting S$0.50 off your bills may seem minuscule at the moment but, these savings add up. Furthermore, you are helping save the environment by conserving the resources.

#4: ASK FOR TEA

I am not a heavy caffeine drinker. This is why I prefer drinking tea over coffee. Have you ever considered exchanging tea with a friend? Purchase two different tea bags and ask for hot water. In most cases, you may refill a cup for at least three times to savor its flavor. Do not worry about asking the staff for a refill as it is free!

Image Credits: pixabay.com

For tea connoisseurs, it is best to avoid steeping your tea twice. Stick to your drink preference instead of wasting money.

#5: MAKE YOUR OWN

Whether you want to believe it or not, you can make your own iced latte while saving money in the process. Order a triple espresso over ice and head over to the condiment bar. Fill up the rest of your cup with the complimentary milk. Voila! You just made your own iced latte!

Lastly, you can make your own Chai Tea Latte. Instead of spending S$5.70 for a Tall-sized Chai Tea Latte, you may ask for a hot Chai Tea (about S$4.20 for a Tall cup). Fill half of the cup with steamed milk. Not only will this recipe save you a dollar but, it will also contain lesser calories than the Chai Tea Latte.

Many of us know the importance of personal financial planning, but do not know how or where to get started. Some of us are hesitant to approach a financial consultant for advice, in fear of being pressurized to commit to a financial product. Some of us may seek out advice or recommendations from our friends, family members, and colleagues, but the advice may not always be suited to our personal needs. Many of us are put off, or even intimidated, by hearing all the unfamiliar financial jargon.

These are just a few of the many difficulties that we encounter in personal financial planning. What if we could remove these challenges and get free, easy to understand, and personalised financial advisory at our fingertips?

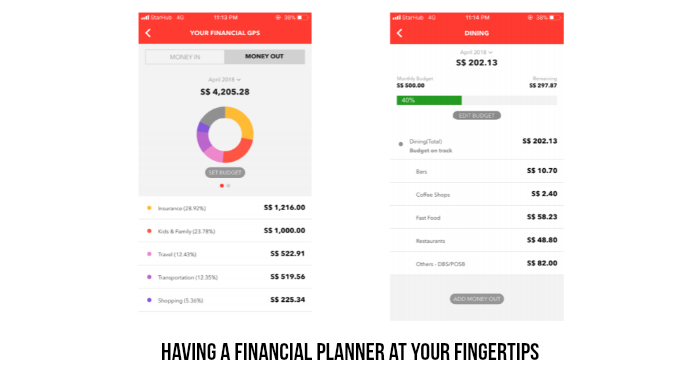

Introducing Your Financial GPS

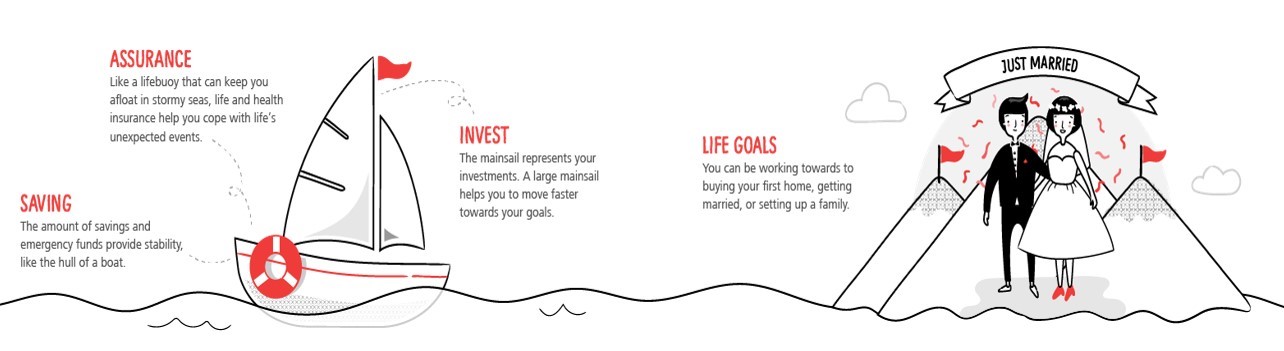

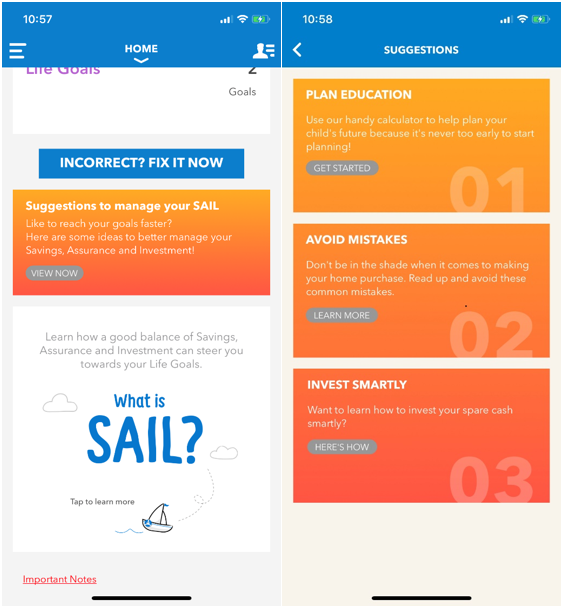

Here’s introducing NAV -Your Financial GPS, a digital financial advisor that helps people like you and me navigate through personal financial planning effortlessly. Your Financial GPS makes the principles of personal finance easy to understand using the acronym ‘SAIL’, which stands for Saving, Assurance, Invest and Life Goals. Starting with Life Goals as the destination for our journey, the other ‘SAIL’ components act as the mainsail, lifebuoy and hull of the boat to help us move towards our destination. For the boat to weather through storms and successfully reach its destination, all ‘SAIL’ components must be looked after, and well-balanced. Thus, this helps to simplify the process of financial planning for many.

Your Financial GPS At A Glance

Your Financial GPS is available to all DBS and POSB customers through the DBS/POSB iBanking and digibank app. When you log into your DBS/POSB iBanking or digibank app, you will see a tab for Financial GPS, which provides a personalized snapshot of your financial health. Your Financial GPS allows you to check your monthly spending across different categories, set budgets, and provides personalized insights based on your saving and spending information.

As a digital financial advisor, Your Financial GPS also provides a snapshot of your current SAIL status. It provides insights on the areas in which you can work on, and suggestions on how to work on these areas to achieve your life goals.

For me, personalizing Your Financial GPS for myself was a breeze. Most of my spending was linked to my DBS Live Fresh card, which was automatically categorized into different categories under spending. For spending that I have incurred using cash or on other banks’ credit cards, I could easily add in the amount as expenses so that Your Financial GPS has a comprehensive picture of my total finances.

I also set up my first Life Goal, which was to pay off my home down-payment of $300,000 by age 40. Your Financial GPS immediately calculated the amount of money which I would need to set aside monthly to achieve this goal. This helped me realise how unrealistic my goal was, which was similar to key insights of how many do not know how much they need for their goals. This was one of the insights that DBS had learnt from its intense and rigorous research to understand customers’ financial planning needs. Besides that, Your Financial GPS also came up with a list of suggestions tailored to my life goals, one of which was very relevant advice on how to avoid common mistakes as a first-time home buyer.

DBS NAV Hub: Free Personalized Financial Consultations

Want to do even more for your personal finance? Book an appointment with the dedicated NAV Crew at the DBS NAV Hub for a free personalized financial consultation. During the private one-on-one session, the crew will help you to assess your financial health and answer any money-related questions you might have. You will receive a free report on your financial health, with absolutely no product or sales pitches involved.

Ready to Sail?

Here are three ways how:

Your Financial GPS

DBS Nav Hub

DBS Nav Website

Available on DBS/POSB iBanking

and Digibank

Click to download the DBS Digibank SG app on iTunes

or on Google Play

The Romanian job market might be difficult for expats that want to work here. The salaries in Romania are pretty low and the competition is very high. Still, if they manage to find a job here, non EU citizens must have a valid work permit, while the EU citizens need to apply for a residence permit. Usually, the employer should take care of all details regarding the application for the work permits, since it is strictly related to the specific job. Moreover, for a company to be able to employ a foreigner, it needs to first demonstrate that there are no fit candidates from EU that can fill in the role, since EU candidates have priority.

Romania has an increasing economic potential, still, there are a lot of large areas that are dedicated to agriculture or undeveloped. On the other hand, the tourism has increased consistently since Romania has a natural beauty and lots of cultural attractions making this industry interesting for investors and development. The most popular domains in which expats can work are the energy and resources industries, but also the manufacturing and industrial sectors. Also, in the services sector the country offers a great potential of new jobs, since there is a high and growing demand for qualified expats with experience in: retail, finance and business services. Moreover, the human resources sector is growing as well, as a lot of HR agencies are looking to hire for executive positions for multinationals and lager companies, such as Dacia, Rompetrol, Romstal, Birdefender, Mobexpert or Petrom. Romania’s main export partner is Germany, importing rubber tyres, car parts, insulated wire or even cars.

For those expats that don’t want to work a corporation there are a lot of NGO choices or even teaching. No matter the industry, most expats works in Bucharest. As experience demands, most companies require fluency in French, German, English or Italian, and IT certificates. On the other hand, the factor that makes it hard for expats to find jobs here is that most companies prefer to hire local citizens, instead of having to deal with the entire process of hiring foreign citizens and obtaining work permits for them. Therefore, the Romanian Government tries to find new ways to attract foreign business owners to establish a branch or subsidiary here and invest into the Eastern European economy. Ever since the communist regime has ended, Romania has had a sustained economic growth that has also continued after 2007, when Romania joined the European Union. In the past few years, even though the country was affected by the global economic recession, it managed to keep modest levels of growth.

Therefore, Romania has a lot to offer for expats looking to work in the country. When an expat outside EU finds a job here and the company manages to prove that there was no EU candidate fit for this position, the company must also prove that the candidate has the necessary experience and qualifications for the job. In order to obtain him a work permit, the employer must attach to the file the resume, criminal clearance, medical checks and reference letters from the candidate. The process of getting the work permit can take around 45 days. After the employer obtains the work permit and gives it to the expat, he must apply for a long-term visa at the embassy from their country.

After getting to Romania, non-EU expats must get a CIF (fiscal identity code) by registering at the Romanian Ministry of Finance. In order to submit their request, they will need to present a copy of the employment contract, alongside their work permit, visa, passport and a proof of residence. The long-term visa and CIF are needed in order to obtain a stay permit from the General Inspectorate for Immigration, and it must be done 30 days before the long term visa expires. In addition, the expats will need to provide medical clearance, proof of residence, identification and salary.

In conclusion, non-EU expats have to go through a more complex process of getting their rights to work in Romania than EU expats. It is highly recommended to get legal advice if you encounter any unclear things, in order to be sure that everything is according to the Romanian law regarding your employment.

Whatever your reason may be for buying yourself a car, you should take out car insurance immediately afterward. After all, you wouldn’t want to face legal repercussions for driving without any car insurance. But if it’s your first time to purchase car insurance, it’s easy to do it wrong, especially with so many insurance companies out there offering protection for both your car and your finances. To make taking out car insurance easier for you, here are some key tips to consider:

1. The state where you’re residing would require you to purchase third party cover as a bare minimum

There’s no telling at all when your car might accidentally hit a person or a piece of property no matter how defensive you are with your driving. The person your car hit might get injured or even die. The piece of property that your car had crashed into might become unusable or beyond repair.

Worse, the entire balance of your savings account might not be enough to cover the medical or funeral costs of the person that your car had hit. It might also not be enough to cover the repair or replacement costs of the property that your car has damaged. As a result, most states would require you to buy third party cover as part of the car insurance that you’ll be taking out from your chosen provider.

Unfortunately, third party cover won’t be able to shoulder any damages that your car had sustained as it only covers costs associated with a person or piece of property that your car had hit.

While not a state requirement, you might want to purchase comprehensive cover as well.

On the other hand, if you want any damages that your car had sustained shouldered by your chosen insurance provider, you should buy comprehensive cover instead. This will help with any repair costs associated with your damaged car.

Your car insurance’s comprehensive cover can also act as a third-party cover since the former allows for a wider coverage compared to the latter as evident in its name. The said type of cover can also shoulder you financially in case your car is consumed by fire, stolen, or hijacked.

You might want to include some extra features on top of the car insurance that you’re planning to take out.

Having a third party or comprehensive cover might not be enough once you take out car insurance as it might not sufficiently cover any highly specific damages that your car may sustain at any given time. Thus, you might want to have some extra car insurance features so that you can still get protected no matter what unfortunate situation might happen to your car. Some of those additional features that you can consider including in your car insurance are as follows:

Windscreen cover – useful for when your car’s windshield, side windows, or rear window gets broken or cracked, and you want to recover the cost of having any of them either repaired or fully replaced

Fire and theft cover – as the name implies, useful in case your car either gets burnt to a crisp by fire, stolen by burglars, or hijacked and you haven’t taken out comprehensive cover as part of your car insurance policy

Zero depreciation cover – aims to add value to your car insurance’s comprehensive cover by excluding costs associated with your car’s depreciation in value due to age, wear and tear, etc.

You might want to consider looking into other types of car insurance coverage as well.

As both third party and comprehensive cover of your car insurance might not be enough to help you financially, you might want to consider including the following additional types of car insurance coverage in your car insurance:

Collision coverage – covers repair costs associated with your car after you’ve gotten involved in an accident with another driver regardless if the said incident was your fault or theirs, though you’ll want to add this one only if you’ve bought your car new and not used

Uninsured and underinsured motorist protection – useful if an uninsured or underinsured driver had hit your car since they’re unable to pay any repair costs associated with it but you wouldn’t want to pay those costs out of your pocket at the same time

Personal injury protection – Pays for all medical expenses and lost wages that you or any passengers that you’ve brought along with you in your car would incur after you’ve gotten involved in an accident

The amount of your car insurance premiums depends on the amount of risk that you’re posing to your chosen insurance provider.

Your car insurance premium is the amount of money that you’ll have to pay for the car insurance that you’ll be taking out from your chosen provider. How much your car insurance premium will amount to is proportional to the degree of risk that you’re carrying with you as a driver.

Your chosen car insurance provider would gather information about you including but not limited to your age, criminal record, and residence’s location to determine the degree of risk that you’re posing to them. The higher the risk that you’re posing to your chosen provider, the more expensive your car insurance premium would get.

Thus, if you want to pay an affordable car insurance premium amount, you’ll have to lessen your degree of risk.

Ask your chosen provider if the car insurance would cover you in certain situations other than driving your car or not.

There might be some situations where your car had gotten involved in an accident, but you weren’t the one behind the wheel at the time when the incident had occurred. Or you might have been driving somebody else’s car or a rental vehicle when you’ve gotten involved in an accident.

In cases such as this make sure the provider covers this prior to taking out the insurance to make sure you’re fully covered.

Pay your car insurance premium either as a lump sum or in installments depending on how much money you’re willing to give to your chosen provider.

As already mentioned earlier, the money that you’ll pay is known as a premium. You can pay your car insurance premium in one go covering an entire year and even get a discount from your chosen provider while at it. But if that’s too heavy of a financial burden to you, you can pay your car insurance premium in two, four, or 12 installments instead. However, you should take note that the higher the number of installments, the higher the additional fees that you’ll have to pay as well aside from your car insurance premium amount.

When the policy period expires, they’ll automatically renew it unless it isn’t eligible for renewal anymore.

Right now, there’s no such thing as multi-year car insurance. In fact, the longest car insurance policy period is only a year followed by six months and one month. However, car insurance with a policy period of only one month is usually reserved by providers only for those drivers that they’ve assessed as high-risk. Thus, the car insurance that you’ll be taking out from your chosen provider may have a policy period of either six months or one year.

Once your car insurance’s policy period comes to an end, your provider would automatically renew it, especially as your car insurance is most likely to have an auto-renewal clause included in it. But if your provider didn’t automatically renew your car insurance’s policy period either because you’ve become a high-risk driver or you’ve moved to a different state, you’ll have to take out car insurance from another provider instead.

Conclusion

All 50 states in the U.S. require every car driver passing by the nation’s roads to carry car insurance. Thus, unless you want to break federal and state laws, you should look into car insurance after successfully purchasing a car. However, as you may be clueless about buying car insurance, the above-listed key tips to consider should make taking one out an effortless process for you. After all, better safe than sorry.

Frugality is an admirable trait, in most cases. Frugal people are typically prepared to tackle the bumps ahead. They are also able to cut down their environmental wastes. However, giving a reaction is essential if the frugality of your boss pulls down your productivity and lowers your workplace morale.

Keep these things in mind before approaching your boss:

WHEN DISCUSSING ABOUT MONEY

As most of the things in life, timing is everything. Choose the appropriate time and place to approach your boss. For instance, you must not discuss about the loss of a major account after your boss got into a car accident. It is not appropriate to discuss serious matter over a phone call either. Remember to equip yourself with respectfulness when discussing money matters.

Image Credits: unsplash.com

Be polite when asking your boss for what you need or want. Be prepared to graciously accept whatever his or her answer is. Do not whine!

WHEN RUMORS CIRCULATE

It goes without saying that the portability of social media influenced how gossips can circulate on a wider scale. With rumor mills running on hyper-drive, people rarely invest their time into validating each one.

Say that there is a rumor about how your supervisor’s errors plummeted the sales of your company. Without adequate research and lack of communication, you can easily make negative assumptions. This is why learning the full story is important.

WHEN ASKING FOR GROWTH

Loyalty is a two-way street. There is a fine line between sacrificing for a company that you love and recognizing that you are taken advantaged of. If you are offering your continued loyalty to an employer for over 5 years then, you deserve to be compensated.

When a cheap boss fails to recognize your value, it can stroke a sizzling fire of discontent.

WHEN YOU FEEL UNDERPAID

If it seems as though your employer is exhausting you in unnecessary proportions then, you may approach him or her for a pay raise (or a better schedule at the very least). You do not need to let your emotions get in the way! You will only sound conceited and demanding. Instead, start the conversation on a positive note. Praise how well the company is doing in the past quarter or the recent months. Afterwards, you may ask how this affects the employees.

Image Credits: pixabay.com

The next step is to do your research. Be prepared to show your employer how your salary stacks up in comparison with people with similar jobs. You are more valuable than you think; otherwise, they would have fired you a long time ago!