(Image credit: Moyan Brenn via Flickr)

(Image credit: Moyan Brenn via Flickr)

I just got back from Hong Kong.

While i love the amazing skyline from Victoria Peak, what got me excited were not the insta-worthy photos i took or the dim sum i gobbled down at Lung King Heen.

It was the fact that i actually travel for free.

Free? Does it means that i won a free trip to Hong Kong or had my travel sponsored by a company?

Good guess, but nope!

Well, the trick here is about planning my own finances. I couldn’t have included Hong Kong into the list of places to visit without exceeding the budget i set aside for this year.

A few years ago when i was still a student, i didn’t care too much about my own finances since i was spending within my means. Like many others, I had my money stashed away in a POSB’s saving account. Who care about interest rates when we hardly have five figures in our possession? The returns were pittance that it hardly warrant any extra attention.

My attitude changed when i had friends who were boasting about how much money they were making. I told myself i wanted to be like them — to be rich, in the shortest amount of time.

It seems then that the only way is to invest venture gamble into the stocks market. I had no idea where to start until one day i was approached by a financial adviser when i was exiting the MRT station. And being a ambitious and impulsive young adult, i was persuaded into buying a saving plan that invests into the market with some kind of insurance cover that comes with it.

It felt good even though i had no idea what i was buying into – the feel good factor that i am now investing like an adult.

I call in to check on the policy every month, but apparently i was told that it is still in the early stage and had little or no cash value.

After a few months i gave up because it hardly grows and sadly i was told that if i were to terminate the plan, i would end up with almost nothing.

The change

From then on, I told myself that no one else can manage my own finances except myself. I need to take the responsibility or i will be the one suffering down the road.

I spend months reading up on books, forums, MoneySense and any resources that i could laid hands on. I begin to understand the importance of budgeting, investing and how to manage my own finances.

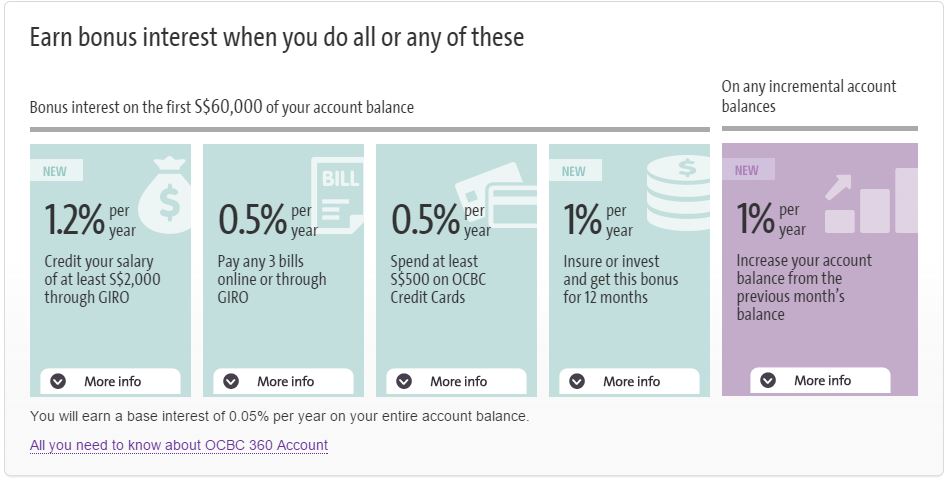

I started by switching my funds to a higher interest-bearing account such as the OCBC 360 where customers could potentially earn up to 3.25% as at 1 May 2015.

It was also then that i realized that previously i was holding on to an investment-linked plan which comes with high fee and charges. It is not cost-effective to achieve my goals and i had to take the hard decision to surrender and make a loss.

A better way that i learnt is to buy term insurance and invest the difference. Term insurance is cheap and affordable although it does not have cash value. But the difference i could potentially save could be put into better investment vehicle such as the low cost fund that tracks the Straits Time Index (STI) which has a historical return of around 8 per cent in the long run.

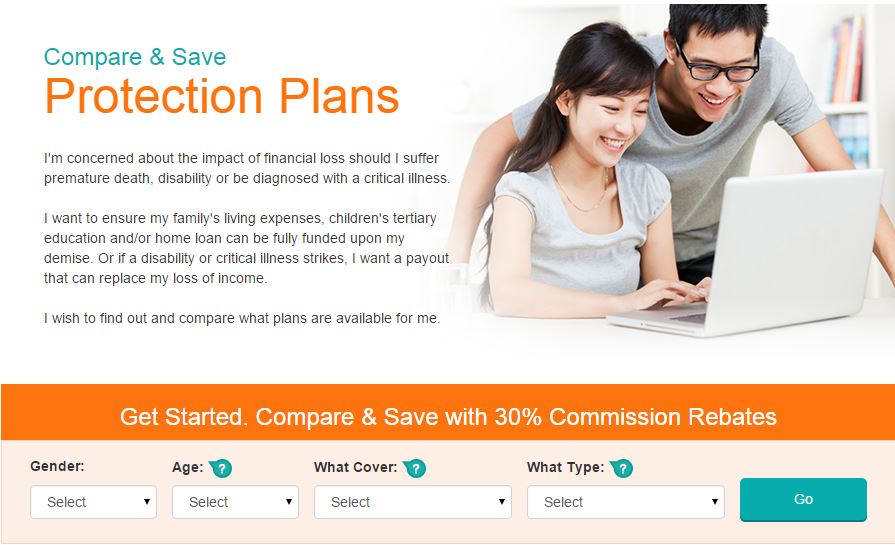

I was introduced to the online platform DIYInsurance — a portal which allows me to compare the different term insurance plans out there. What appeals to me is that they rebate 30% of the commission back to the customer and at the same time still make an effort to go through the planning process, making sure that the person is on the right track.

They have a live chat system where i can ask any questions on how to use the online platform, as well as clarifying with the client services manager on the semantics of insurance definition. It was fuss free and it beats the inconvenience of holding on to the line when you call in to financial institutions for enquiries.

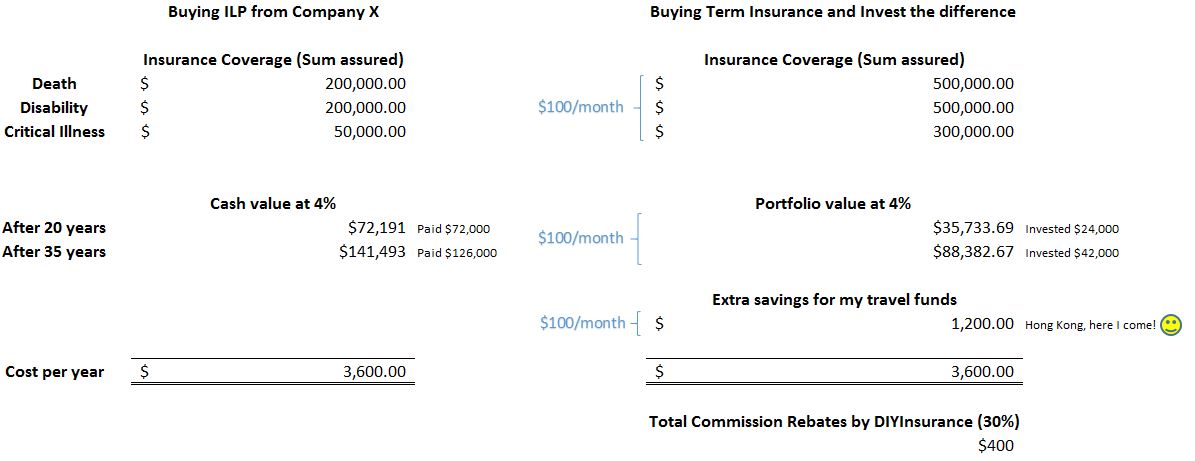

If you are wondering how much money i save using the DIY method, i have done up some numbers for comparison.

(Click to enlarge)

As you can see, i was previously paying $300 a month for a $200K cover on death and disability and a $50K rider on critical illnesses. If the funds grow at 4%, it will take me 20 years to break even and 35 years to make a small profit of $15K. (calculate the ROI)

If i were to employ the alternative strategy of buying term and investing the difference, i’d be merely paying $100 a month for a $500K cover on death, disability and $300K on critical illnesses. The other $100 will be channeled to a low cost fund, and assuming it grows at the same rate, my portfolio would be sitting at a value of $35K after 20 years or $88K after 35 years. (note that i’m contributing 2/3 of what i’d have otherwise contributed to the ILP and i have pegged its growth at 4% for comparison purposes)

As a result, i managed to put away $100 a month into my travel funds and this adds up to a significant amount of $1,200 a year. A sum that is sufficient for me to pay for the return air ticket to Hong Kong which including hotel and shopping expenses incurred during the trip. I am also getting $400 worth of commission rebates from DIYInsurance which i can either re-invest or spend it on my next trip. (I have re-invested it)

In conclusion

By taking charge of my own finances, i am now enjoying a higher returns of 2.25% (excluding the 1% bonus to insure or invest) from the money sitting in the bank as well as future incoming funds. I have also manage to cut down on unnecessary fee and charges slapped on expensive insurance products by switching to a more affordable term cover and investing in a low cost funds.

I have lost some money in the investment linked product but at the same time i have took home valuable knowledge and wisdom of managing my own finances, and as a result, created more wealth from it.

Well, perhaps a road trip to Australia next?

(Article contributed by Cheryl, a Marketing Executive working in Singapore.)