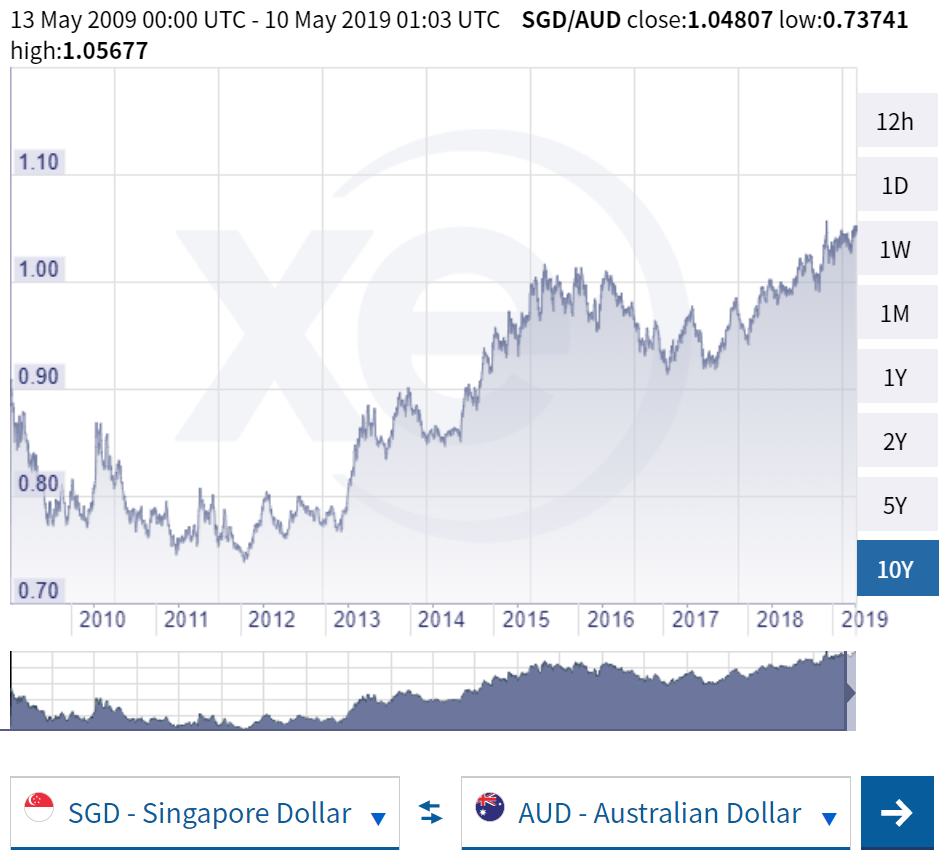

1 Singapore dollar can now get you 1.05 Aussie dollar

Planning for a trip to Australia? This is a good time to visit the money changer.

The Singapore dollar rose to a 4-month high against the Australian dollar since the last time it hits S$1.00 = A$1.051 in January this year.

If we look at the 10-year chart, you can see that it is near its peak.

The decline of the Australian dollar is probably due to the result of the trade war between China and US. Australia’s economy is dependent on exports of its natural resources and a dampen China’s growth prospect will definitely affect the dollar.

If you are a prospective student going to Australia for your studies, good for you.

Whether you like it or not, you are expected to know what you want to do for the rest of your life the minute you graduate from secondary school. It is understandable to strive for the highest paying field or job possible. However, that is not always the case.

If you were to invest money at a young age, you can build a nest that is enough to sustain a comfortable lifestyle in your adult years. This may lessen the pressure you feel when choosing a career path. To begin your investment journey, you must read books aimed at young investors.

PERSONAL MONEY MANAGEMENT

Cary Siegel put an interesting twist to money management with the book entitled: “Why Didn’t They Teach Me This in School? 99 Personal Money Management Principles to Live By”. To Siegel, proper money management in accordance to the economy is an important lesson that the youth shall know. He imparts this knowledge by dividing his lessons into 99 principles. Said principles include investing, housing, spending, debit, credit, and budgeting. I, for one, am curious why these practical life skills are not taught in today’s curriculum.

You will get a sense of how to handle the financial aspects of your life as you read along. By combining solid advice on money and adulthood, your curiosity will be widened.

COMMON SENSE INVESTING

Looking for the perfect investment book for young adults? Search no further as John Bogle’s “The Little Book of Common Sense Investing” details the fundamentals of investing! It describes a plain approach that anyone can implement to achieve above average returns.

For people who are risk-takers, his methods may seem too simple. Consider studying further. After all, Warren Buffett included this book on his recommended reading list.

THE WARREN BUFFETT WAY

There is a reason why Warren Buffett’s name cannot be erased in the list of legendary investors. You see, he adapted his own investing style that lasted throughout the years.

It goes without saying, his results have been extraordinary!

His strategy was encapsulated in a book entitled “The Warren Buffett Way”. This books highlights how he invested in the past and in the present. For the young adult who wants to invest in businesses, the insight into Buffett’s thought process is of tremendous value.

MAKE MORE MONEY THAN YOUR PARENTS

Before Christmastime, a financial book from The Motley Fool entertainment was released to serve as the perfect Christmas gift for young adults. First and foremost, The Motley Fool is a “multimedia financial services company that has made investing fun and easy for millions of people since it was founded in 1993”. It aims to share information on how to efficiently manage your money.

David Gardner’s “The Motley Fool Investment Guide for Teens: 8 Steps to Having More Money Than Your Parents Ever Dreamed Of” is not as funny as it sounds. It is a piece of literature that gives you a guide to outperform your parents’ current professional success. It provides teens with a road map for sketching a financial journey from investing to saving or from budgeting to spending. Ultimately, it reminds the youth that every money spent is an investment. You have to make it count!

Image Credits: pixabay.com

The books listed above offer practical and understandable suggestions, solutions, and hacks about finance. I hope that these books may serve as an inspiration when you start your investment journey. Good luck!

Congratulations on becoming a new parent! Welcoming another human being into this world can change your life in many ways. Most of these changes are for the better. While, some changes are challenges too.

I am referring to the hefty price tag attached to child-bearing and child-rearing. You have to spend about S$8,000 to S$18,000 a year for that.

You read that right! You will be spending five figures on groceries, clothes, toys, diapers, hospital visits, and daycare. With a growing list of expenses, you must rethink how to manage your financial life after having a baby. Here are some tips to help you out:

SHAKING THINGS UP

You and your partner have had a working budget for years. And this household budget seem to work fine. However, you have to reset your budget once the baby comes. Your pooled incomes, savings, and investments shall cover your child’s expenses.

Begin by saving for the delivery by taking up Medisave’s Maternity Package. Using Medisave for childbirth can help offset the cost of your hefty delivery. Roughly, you can claim about S$450 per day on hospital stay, S$900 on prenatal expenses, and S$750 to over S$2000 on surgical procedure.

For instance, you wife had a Cesarean delivery and was hospitalized for two days, you will be able to claim about S$900 on prenatal expenses, S$900 on hospital stay, and S$2,150 on surgical procedure. This sums to about S$3950 worth of claims.

FILLING THE PIGGY BANK

It comes as no surprise that education will take a huge toll in your expenses for the years to come. Thus, setting up an education fund for your beloved can help you in the long run. While taking up an education loan is always an option, the cost of schooling gets higher each year. You must start saving money along with the arrival of your little one.

A scenario close to my heart is the effects of my uncle’s death. My uncle is the breadwinner and his son has not yet finished his schooling. As he continue his secondary education, he finds it difficult to fuel his financial resources. If only my uncle set up an education fund beforehand!

Saving up for your child’s education can cushion potential financial bumps. This way, your child will not have to compromise his or her education.

SETTING UP A CAPSULE WARDROBE

Along with the trends of minimalism and sustainable living comes the existence of the capsule wardrobe. A capsule wardrobe enables to the owner to keep key pieces that he or she can mix and match in the years to come. The only challenge when it comes to toddler is that they grow up so fast!

Matching outfits or assorted clothing can be adorable to look at! However, your infant does not need twenty sets of outfits! He or she will grow out of these clothes faster than you can post about it on Instagram. Thus, you must limit your child’s wardrobe. Allow a set of basic items with interchangeable colors and patterns to full your drawer. You do not want to spend on designer clothing that your child will surely ruin with stains and other mishaps!

Image Credits: pixabay.com

Here are just some ways to save money as a first time parent. Make it a habit to check children’s websites and forums for ways to create your own baby food or to conduct your own reading class. Nothing is impossible with a little determination from a parent!

Frequent travellers rejoice! In an industry first, Allianz Global Assistance is launching an EXCLUSIVE Allianz Assist Card that comes with S$28 worth of EZ-Link value stored inside. Simply purchase an annual travel plan from Allianz to qualify for this attractive promotion. *Learn more about terms and conditions

Besides getting on-the-go travel companion, purchasing annual travel insurance may save your money and hassles compared to buying a single trip plan. More details below:

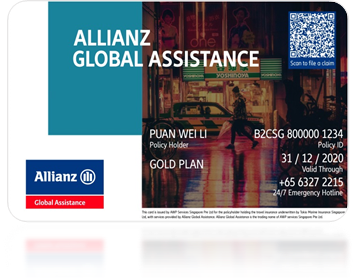

Personalized Allianz Assist Card

Upon purchasing an annual travel plan from Allianz, you will receive a personalized Allianz Assist Card as your travel companion that comes with your own name, your policy ID and the policy Type. It will also contain details such as the validity of your travel policy so that you know whether you are still insured when planning your next travel. Your Allianz Assist Card will be delivered free to your registered address and can be used immediately for Singapore public transport rides with no activation of the card required!

Greater Travel Protection At Your Fingertips

Allianz Global Assistance provide greater travel coverage such as overseas medical expenses, luggage loss, and travel delay coverage.

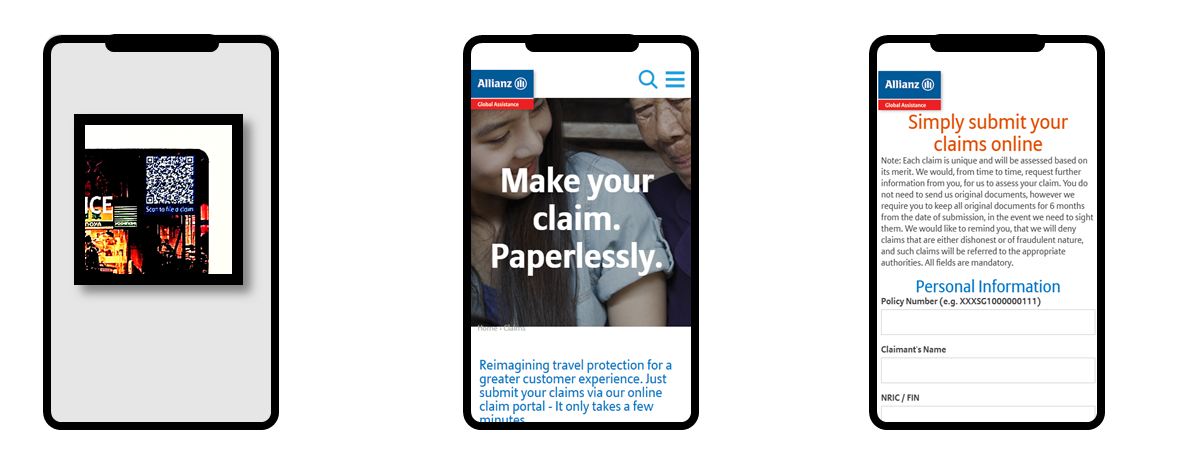

Besides all details listed above, Allianz Assist Card contains a 24/7 Emergency Hotline (+65 6327 2215)where you can and get assistance globally. Most importantly, it contains a QR code which allows you to file your travel claims in a seamless experience. After scanning the QR code on your Allianz Assist Card, you will be brought to Allianz Global Assistance’s online claim portal. Simply follow the instructions, fill up the necessary information, upload softcopies of supporting documents and submit your travel claims! With the Allianz Assist Card, you have greater travel protection at your fingertips!

Purchase Now To Save 45% On Your Annual Travel Plans

For a limited time only, Allianz Global Assistance is launching Allianz Assist Card with a HUGE 45% discount. To receive your personalized Allianz Assist Card (which comes with $28 EZ-Link value), simply purchase your annual travel insurance policy from now till 16 June 2019! Hurry and go online to purchase your Allianz Global Assistance annual travel insurance policy here.

Many investors may find investment in Peer-to-Peer (P2P) lending attractive due to its potential benefits, such as higher returns and shorter tenors. The barrier to entry is also one of the lowest amongst all types of investments, from just $20.

First-time investors who are not yet familiar with the details of P2P lending may be hesitant to start this investment. We have compiled a list of 4 things you should look out for when investing with P2P platforms to help you avoid common mistakes made by first-time investors.

1. Investing only in loans with high returns

Investors may often be incentivised to participate in P2P investments due to the high returns they potentially provide. To receive greater returns, some investors may end up only picking loans with higher interest rates. However, interest rates are priced based on the credit risk and higher interest rates are an indication of higher risks. Interest rates should not be the only determining factor for investing in a loan. As an investor, you would be better off diversifying you investments across loans with varying interest rates.

2. Not diversifying your investments

In any type of investment, it’s crucial to diversify your portfolio so that you won’t end up putting all your eggs in one basket. When you concentrate your investments and don’t diversify them, your portfolio may go south quickly if there are non-performing loans.

Expanding on the first point, a balanced mix of high and low interest rates is a way to diversify your investments. Additionally, you can also invest across different SMEs, industries, products, loan tenors as well as investment amounts.

An easy way to diversify on Funding Societies’ platform is to set up Auto Invest. The Auto Invest bots can be customised based on your investment preferences. That said, you have the flexibility to opt out of loans in which you are not interested before the crowdfunding starts.

Secondly, you can diversify across different types of investment assets that align with your investment risk profile. This can include savings, insurances and the traditional investment vehicles such as bonds and stocks.

3. Withdrawing returns when you receive them

It may be tempting to withdraw your returns once you receive them. However, experienced P2P investors typically don’t do that to potentially benefit from the compounding effect from re-investments. You can re-invest your monthly repayments to potentially receive a higher compounded interest. Your returns (in the form of interests) also start to form part of your capital which you can utilise to re-invest in upcoming loans.

By leaving the repayments in your account, you are ensured that you have funds which can be readily invested when opportunities arise, even without pumping in fresh funds.

4. Not being familiar with P2P lending platforms & the details

While the concept of P2P lending is not difficult to understand, it is important to equip yourself with knowledge of the P2P lending platforms that you wish to invest with. Investing with a stable and responsible P2P lending platform will help you minimise unnecessary risks and inconveniences. Ensure (and expect!) that the platform is responsive, transparent in its processes and stable to carry out its operations and duties for investors.

A good platform to consider is Funding Societies, the largest P2P lending platform in Southeast Asia that holds the Capital Markets Service Licence issued by the Monetary Authority of Singapore (MAS). As of March 2019, it has crowdfunded more than $450 million in the region across more than 300,000 loans. This statistic also reflects the number of opportunities for investors.

Understanding the details of each investment will also allow you to make informed investment decisions. At Funding Societies, a loan fact sheet will be provided on every investment opportunity. It contains details of the loan, its repayment schedule, a summary of the company and guarantors, the company’s financials, and comments from Funding Societies’ very own credit team.

What’s the ONE thing you should do?

Seriously consider P2P lending as part of your investment portfolio! 😀

P2P loans are a form of alternative investments that hold many benefits, especially for new investors that would like to start small or with experienced investors looking to diversify their portfolio. An investment with Funding Societies starts from just $20.

By watching out for these 4 listed things that you should not do when investing on P2P lending, we hope that you’ll be able to have a smooth and successful P2P investment journey!

Ready to start your P2P investment journey? Sign up with Funding Societies today, or live chat with their Customer Experience team to understand this investment better.

Disclaimers

This article is contributed by Funding Societies and is adopted from this blog article.

It should not be construed that Moneydigest is endorsing this article or any of the products and services provided by Funding Societies.

Nothing in this article should be construed as constitute or form a recommendation, financial advice, or an offer, invitation or solicitation from Funding Societies to buy or subscribe for any securities and/or investment products. The content and materials made available are for informational purposes only and should not be relied on without obtaining the necessary independent financial or other advice in connection therewith before making an investment or other decision as may be appropriate.