Living barely within your income is not a laughing matter. When you are living paycheck to paycheck, you live a life of constant stress, worry, and dread that you might be stuck in an unfortunate debt. It is a struggle to gain control of your money and your commitments. So, here are 3 Simple Tips To Stop Living From Paycheck to Paycheck…

1. CREATE A SYSTEMATIC FINANCIAL OPERATING SYSTEM

In order to cease your worries, a huge turnover can be money flow management. You must give conscious effort to know about where your money flows in and out. Once you have control over your money flow. Then, you will be able to create a systematic financial operating system that consists of: money flow management and budgeting.

Money flow management is accomplished by using a ledger or an app. There are a couple of efficient yet free apps that can help such as: EXPENSIFY, EXPENSE MANAGER, MONEYWISE, POCKET EXPENSE PERSONAL FINANCE, and MINT.

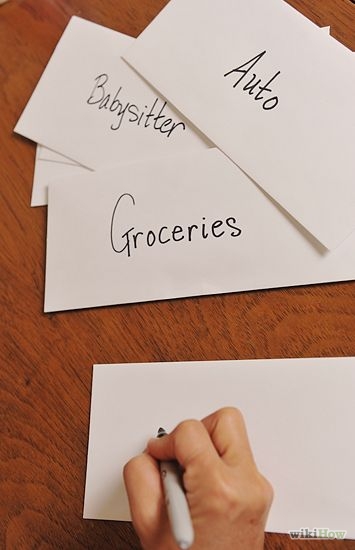

Image Credits: wikihow.com/Do-Envelope-Budgeting

Likewise there are a couple of budgeting such as STATIC or FLEXIBLE budgeting. For personal finances, I highly recommend a simple technique called ENVELOPE budgeting. It starts by storing the cash into separate categories of household expenses that are allocated in separate envelopes.

Budgeting will surely help you gain clarity and control. Start by writing down your monthly income, followed by your monthly expenses, and then subtract the two. Plan and search for a suited technique.

2. PREPARE MONEY FOR YOUR BILLS ACCORDINGLY

Some bills are due frequently while some are semi-annually. Prepare money for your bills accordingly by noting them down. If you have a monthly bill, you may try a trick called half payments. For half payments, you prepare the payment for the bill by subtracting half of the bill’s amount to your bank account per two weeks (bi-weekly).

3. BOOST YOUR EMERGENCY FUND

Prepare for the unforeseen events and financial failures by saving at least 8% of your income per month. You shall call this category your “emergency fund”. It is better to save a certain amount of money than to have nothing save at all.

When you are young, in your 20s or 30s, retirement feels like a looooong way ahead.

Typically in your 20s, the only person you have to spend for is yourself. In your 30s, you will have new financial priorities such as the wedding, child’s schooling, house loans, etc.

If you consider all the aspects of your finances and fast-paced life today however, you will realize that it is the best time to start saving for retirement before you hit 35. Even the strategies to save for retirement are in-lined with the ideal to start saving while you are young.

Here are the 4 strategies to save for your retirement before your mid-30s…

1. PAY OFF YOUR DEBTS

It makes sense to pay off your debts or at least your high-interest debts before you save for your retirement. Since not all debts are equal, pay off your high-interest debts first followed by the lower ones.

2. SET UP A BUDGET

Systematically allocate your income onto different categories and stick to that budget. Do not spend beyond what your budget is for that month. This allows you to save regularly rather than arbitrarily.

3. SEEK FOR AN EMPLOYER THAT SUPPORTS YOUR GOALS

Image Credits: American Advisors Group via Flickr

As much as possible, look for an employer that supports your long-term goals. If your employer offers Retirement or Pension Plan then embrace this company benefit.

4. TRACK YOUR RETIREMENT SAVINGS

During your…

a. 20s

It is best to start saving at least 5% of your income or sign up for your employer’s Retirement Plan. Avoid debt as much as possible and get educated about your finances.

b. 30s

Invest your money and check whether it is in lined with your goals. Increase your contribution to your Retirement Savings while preparing for your child’s school fees.

c. 40s

Make thought-through decisions about your expenses and cut down the unnecessary. This is when you hit your savings to the maximum. By this time you should have at least S$80, 000 to your Retirement Savings.

d. 50s

During your 50s, you must prepare for the unexpected. Seek the financial experts’ help if you must. Then, plan your exit with glee because you are well prepared for it.

Note: This is just an ideal time frame for your Retirement Savings. Contemplate and reconsider the realistic measures that are suited for you.

Some people struggle to make ends meet while others succeed in their finances. Have you ever wondered why? The answer may be a combination of different factors that play a significant role and one of them is repeated behavior. An individual’s repeated behaviors or habits are learned from young and affects the person’s decisions in the long run.

So, understanding the value of money and being taught at an early age to save your allowance, watch your spending, and note down your expenses can really boost your finances throughout your life. As the saying goes, old habits are hard to break. Without further ado, here are the Secret Habits of Financial Savvy People That You Must Adopt…

1. WATCH YOUR SPENDING

The first step is to be aware of your spending patterns and exactly how much you are spending per month and per annum. This will help you decide how much you shall save and help you to highlight the unnecessary expenses.

Recording all your expenses, no matter how big or small they may be, can help you plan your budget wisely. Find the perfect (and Free) money management app for you here.

Lastly, stop buying useless stuff that you do not need. Rethink if buying overpriced coffee rather than making your own coffee at work saves you more. Instead of buying lunch, pack your own lunch for at least 2 months. It may seem simple, but these unnecessary expenses add up.

2. SET SMART FINANCIAL GOALS

Develop a habit of financial goal setting to know where you are going and to plan how you can get there. Write down your financial goals with a witness (e.g., spouse or a close friend) and contemplate the monetary milestone you would like to accomplish in the next 2 to 5 years. Track down your monthly progress.

This habit is practiced in businesses that have quota system or in fundraising events, but it surely works for personal finances too!

3. ACCOUNTABILITY AND INDULGENCE

In most cases you must you shall practice the habit of being accountable and owning the responsibility in your spending. Be accountable of your spending by managing it and by following your financial goals. It is an important habit if you want to maintain consistency and progress.

Image Credits: TaxCredits.net via Flickr

In order for a habit or a behavior to be repeated, it must be rewarding. Set aside at least 3-5% of your income to a category called “incentive or shopping money”. I personally do this through the envelope budgeting system (learn about it here). Giving yourself a well-deserved treat after the whole month’s work will surely keep you going.

For questions like “What to buy?” requires fundamental analysis. But when someone asks, “When to buy?” This is when technical analysis comes into play. Technical analysis is the other approach of investing. When you talk about technical analysis, you’re looking at things like charts, chart patterns, technical indicators, etc. It gives you a visual information about how the stock price moves for the minute, the hour, the day, week and even month! This information is useful because it can give you a better sense of how the stock is doing right at the moment. Fundamental analysts usually have to deal with information that isn’t updated because company reports would only come out quarterly, or even annually! Many things happen in between the quarters but you could possibly be trading based on the previous quarter’s results which may no longer be relevant.

Pure technical analysts are not interested in the research of a company’s fundamentals because the way a stock price moves would have indicated how much everyone thinks the stock is generally worth. When an undervalued stock moves because it was uncovered by a fundamental analyst, it wouldn’t be missed by technical analyst who watch price-volume action of a share price. As long as a stock moves, the technical analysts will be there watching it as well! Price movements can give a technical analyst a lot of information such as breakouts, psychology of the market players, trend, reversal patterns, etc. These days, there are a lot of people relying on charts when buying a stock. You would only be putting yourself in a disadvantaged position if you choose not to avail yourself to the same information they are receiving. With more and more speculators in the market, fundamentals might be ignored for short moments and only technical analysis can help you for the moment to be profitable.

Here’s an example:

A pure fundamental analyst would not know where the support or the resistance is. He would know what the company should be valued at but he may not know when is the best time to enter. For example, NOL is down-trending from $2.30. A fundamental analyst values it at $1.50 based on Price-Book ratio, P/E ratio, or other metrics available to him. When NOL sells down to $1.50, the fundamental analyst would make the purchase because he thinks that is what it is worth. However, from a technical analyst point of view, he would wait to see if $1.50 is supported or not. If the price is not supported, he waits for the share price to continue falling and test the next support level at $1. When share price eventually gets to $1 and shows that it is supported with a high volume, the technical analyst buys it.

At the end of the day, both analysts got NOL, but the technical analyst got a better price because he knows that from past price movements that $1 is a strong psychological support and buys it at a support instead of simply buying it because he thinks that is what it is worth. Past price actions can give you a hint about the future price movement because of many reasons, largely psychological support and resistance levels. The fact is that many people are relying on such information, and if you aren’t, you will lose out and the market will not make sense to you. Having a visual image of how the stock market is going will be very much easier for you to find support levels such as in the case above.

Of course, this is not to say that technical analysis is 100% accurate and gives you pin-point accuracy. What it can provide you is more information that opens up your eyes to more opportunities for buying entries. There is always a time an investor will face where he says “I’m waiting for the right time to enter”. It could be a fundamentally sound company but simply trading too expensively and this is when technical analysis will tell you when the right time is. Or rather, give you a hint of when the right time is. Of course, hindsight is 20/20 and the chart above could have gone in a totally different direction and crashed through $1 rather than stay supported on 2 more counts on Nov 2011 and May 2012. I used an old chart for the purpose of effectively sending my point across rather than try to teach based on current prices where even I don’t know where the future is. No one can predict how the future price will move, they can only get a vague idea of it. By effectively utilising both fundamental and technical analysis, you would put yourself in a profitable position where the odds of a profitable trade is higher.

Important Disclaimer

The above chart is for teaching purposes only and is not a recommendation to buy/sell.

According to DEBTSteps.com, envelope budgeting or envelope system is a popular way of maintaining a budget. It starts by storing the cash into separate categories of household expenses that are allocated in separate envelopes.

1. TRACK YOUR LAST MONTH’S SPENDING PATTERNS

One of the first steps that you have to take is to analyze your spending patterns, variable expenses and fixed expenses (i.e., monthly electric bills).

Fixed expenses remain the same every month (e.g. Hand Phone Plan, or HDB Rent). Variable expenses include food, entertainment, clothing, and other expenses that may change every month or year. The challenge now is for you to choose on which expenses you can reduce.

2. DEVISE A BUDGET PLAN

Recording all your expenses, no matter how big or small they may be, can help you plan your budget wisely. Categorize your expenses 7 or more sections such as Rent, Utilities, Electricity, Groceries, Gas, Entertainment, Savings, Loan, Childcare, Tax, Travel, etc.

For example if you are Fresh graduate living in your parents’ house and you earn S$1600 a month. Allocate your money with the fixed expenses first.

Rent- S$700

Utilities- S$150

Electricity- S$80

Student loan- S$100

Fixed Expenses Total: S$ 1,080

Then your variable expenses…

Savings- S$170 (transfer it to your bank account)

Groceries- S$100

Travel- S$100

Entertainment-S$100

Emergency- S$50

Variable Expenses Total: S$520

3. PUT YOUR INCOME IN SEPARATE ENVELOPES

Image Credits: wikihow.com/Do-Envelope-Budgeting

Use your marker to assign each category to each envelope. Use whatever size is best for you. It shall be able to fit easily in your purse or wallet. Follow the budget plan and allocate your money accurately. Spend only from the designated envelope and stop spending once you’ve emptied it. This practice of discipline will help you save a great deal of money.

Watch this simple video tutorial of the envelope budgeting or envelope system by NCNBlog: