Not all life insurance agents are trusted advisors. So, the simplest way to prevent being exploited is to seek for an independent agent that will save you time and money. Here are the other secrets that your Life Insurance Agent may be keeping from you…

1. THEIR INCOME IS BASED ON COMMISSION

The agent’s income is solely compensated from the commission. It is one of the possibilities for the agent to have a personal interest that leads to you buying the highest premium possible equating to their highest commission possible. Thus, it may change his/her perspective of things, as well as the type of products clients are introduced to.

2. CASH VALUE WILL NOT BENEFIT YOU RIGHT AWAY

Yes! Cash value will build-up. But it takes about five years to have the cash value equal to the amount you paid for the whole life insurance.

3. BUY TERM AND INVEST THE DIFFERENCE

The term insurance is significantly less expensive than the whole insurance. This is why you can buy term then invest the difference on mutual funds. In fact, the combination of term and your investment for mutual funds may be less costly that the whole life insurance.

4. YOU MAY NOT NEED CHILD LIFE INSURANCE AFTER ALL

Renowned experts namely: Dave Ramsay, Suze Orman, and Neal Frankle are on a arguing against buying life insurance for kids.

“The only reason you need life insurance is if anyone is dependent on your income…please, you new parents, do not let anyone talk you into buying a life insurance policy on your child.” said Suze Orman.

Image Credits: State Farm via Flickr

According to them, if your child is not at the risk of a serious illness and you are financially stable to cover foreseen medical bills then, you are better off without it. Instead, save up for your child’s education until tertiary level.

The vow of “for better or worse…for richer or for poorer” entails an important promise to live in a financially able home. Managing your money on your own can be challenging enough so adding your spouse’s finances may be overwhelming at times. With that in mind, here are 7 Insurance Tips for Newlyweds…

1. DISCUSS YOUR FINANCES AND SET YOUR GOALS

Discuss your finances with your new spouse as soon and as open as possible. You will need to communicate about your bank accounts and about your debts. Set up goals together in order to see which insurance suits your intentions.

2. LOCATION IS EVERYTHING

Housing insurance often pays for destruction, damage, and theft of your possessions. In the event of fire, your insurance will help pay to repair and replace your expensive belongings. Homes close to fire hydrants and fire stations cost less to insure. This is why location of your house is important.

3. TRY THE LUCKY SEVEN

If you are wondering how much life insurance coverage you need, then seek the experts help. Some experts suggest multiplying your annual income by seven so that your spouse is covered for at least 5 to 10 years.

4. CONTINUE DRIVING RED CARS

It is a myth that car insurance companies charge more for red cars. Higher charges come from the age of the client, client’s claims history, and age and model of the car.

5. CONSIDER FLOOD INSURANCE

Housing insurance cover damage caused by pipe overflows but, natural disaster flood are covered by flood insurance. Findings suggest that almost 25% of flood insurance claims are made from low-risk areas, so consider this policy.

6. HOME IS YOUR BIGGEST INVESTMENT

Your home is your biggest investment because unlike cars that depreciate its value the minute you drive them, your house increases its value over time. Houses that are less than 10 years old or those that are renovated within the last 10 years cost less to insure. What’s more? If the house is made of fire-resistant materials such as brick, you can save even more money.

7. BE FIT TO SAVE MORE

Live a healthy lifestyle that includes regular exercise and a balanced diet. Hop on the scale to see if your body weight is the ideal BMI for your age. This is because life insurance companies charge more for people who are overweight since they develop more health problems as time passes. So, stepping on the gym will not only give you a sexy body but it will also help you save more insurance money.

Life insurance is an important tool for an individual’s financial plan. Because you don’t have a crystal ball to predict what will happen to you tomorrow and the day after, you need to transfer this risk to a life insurance company – by paying a premium.

Fortunately, you don’t need any divination to find out how much life insurance cover you need. Since this article is penned in the year 2015, i have reasons to believe you belong to the Gen Y’s population and is knowledgeable enough to work out your own insurance needs by following the steps below. That is also the reason why very soon you will be able to purchase life insurance cover directly from the company without the need of financial planners. (If you belong to the Gen X’s, i don’t see why you need any life insurance besides your Medishield or Medishield Life)

Working out how much you need is no rocket science. It’s as easy as sitting down with a calculator on your hand and asking yourself a few questions.

1. Do i have any dependants?

This should be the first question you ask when you buy life insurance. You want to provide for your loved ones should something untoward happen to you.

Let’s assume Michael has a wife and a 3 years old son that he need to take care of. He is also providing allowance to his aged parents who have retired and not working.

2. How much do they need?

Finding out how much your dependants need is important to determine how much life insurance cover you should be looking at.

Now Michael contributes $2,000 a month to household expenses which include paying for the bills, foods, daily necessities and children expenses. His wife is also working and contribute the other half of the household expenses amounting to $2,000 a month.

If something unfortunate happens to Michael tomorrow, his wife would have to shoulder the responsibility of paying for Michael’s share and may not have enough to cover a monthly household expenses of $4,000 a month.

So Michael wants to protect his share of liability.

He needs to provide for 20 years of household expenses until his son graduates from university and starts working.

He will need to cover himself sufficiently such that the large sum of money paid out can be invested to generate a passive income of $24,000 a year. Let’s assume a modest 4% rate of return, Michael simply divide $24,000 over 4% to work out $600,000. That is the cover he needs to provide a passive income of $24,000 a year for his family.

Once they no longer need this passive income, the bulk of this money could be used to purchase a home for Michael’s son.

3. What about mortgage, other loans or even children’s tertiary education?

For mortgage you would have taken up a mortgage decreasing term assurance to take care of that.

if you look into loans and children tertiary education, you could have factor those into your monthly expenses. That is also to say i am assuming you would have set away a portion of your monthly salary into a portfolio that gives at least 8% of growth to your children education fund.

4. Does that means i don’t need any insurance cover if i have no dependent?

You would hope so. But you might want to look into replacing your income should you become disabled or get critically ill. That is when you should consider getting yourself covered for total permanent and disability until the age you retire.

As for critical illness, a simple rule of a thumb is to cover for 5 years of your income because of the prognosis of cancer (or the survival rate of cancer, being the most common critical illness in Singapore) You can basically go without income for 5 years since you will be focused on recuperating and going for chemotherapy and other cancer treatments.

For hospital cover, don’t forget you have your Medishield or Medishield Life to take care of them.

What’s next?

We should be expecting a web aggregator to be rolled out in the first quarter of 2015. Now that you know how much you need to get yourself covered, most consumers can actually skipped the middleman to pay a lower premium and make use of web aggregator to find the most suitable product at the most affordable price.

Do you know the feeling when walking from the closest MRT station towards your house and it simply takes forever? Driving around the island of Singapore is a true pleasure. One hardly ever encounters a traffic jam and generally gets quickly to any desired place. There isn’t any problem with pollution or a high car density. However, driving and owning a car in Singapore can be a costly undertaking. It is not only the car and its license that is expensive, but also the car insurance can weigh heavy on one’s finances. No matter how much money one has – there isn’t any chance that one can lower the government-imposed charges for the usage of the car. Therefore, it is even more important that one finds a beneficial deal for the car insurance.

The first trick to safe money is the oldest one in the book – drive safely. However, many people are not aware of the system that car insurances around the world use. If one has a car accident, the rate one has to pay monthly or yearly is instantly increased. If you are driving safely around Singapore over a long period of time, your car insurance will remain the same or even shrink slightly. Those people, who tend to crash their car, will not only pay for the reparation, but also for the continuously increasing car insurance. Many car insurances offer a no-claim discount (NCD). This allows for a 10% discount for every year in which you haven’t claimed anything. If you for example have only a minor dent in the car, you may want to consider not claiming it from your insurance, as you can possibly save more with the discount. The NCD can reach a maximum discount of 50%, with which one can safe potentially thousands of hard-earned dollars.

Not only being a safe driver, but also being a law-obeying driver can help you with the insurance. Fancy and fast cars are extremely attractive in Singapore, but even if you have one of those racecars, you are still subject to the speed limits. If you have a clean license over an extended period of time, you can earn a further discount instead of another ticket. After three years driving without committing a traffic offence, you can get the Certificate of Merit (COM), which brings you a further 5% discount on top of NCD. Using all this saved money, one can buy a ticket for the Formula 1 Race in September and enjoy proper racing.

When you are arranging a new car insurance policy, then pay attention to what you actually commit. Many policies often include unnecessary points. Go through them and use your commonsense. It can be that your car insurance also covers you for something that you are already covered for. A personal injury policy within your car insurance is very good, but a total waste of money if your health insurance already takes care of you in the case of an accident. Being covered twice for the same cause will not bring you double money and doesn’t mean you can claim it twice. Furthermore, one should check exactly what policy covers what points. When renting a car, one might be already covered in the case of an accident through another insurance. Different policies might have different names, but cover actually the very same thing. A rental-car insurance might include the same points as a collision policy. Therefore, it is very important, if one wants to save money, to double check the covered points in a insurance. Furthermore, one should eliminate all unnecessary points.

Car and accident statistics aren’t the best friends of young drivers. Unfortunately, an inexperienced young driver has the tendency to crash a car more often than older and more experienced drivers. This results in a higher insurance policy for younger drivers in general. Even if you are driving perfectly, you are paying more by default. Therefore, it is advisable to let your experience on the road be reflected in your policy. If you have been driving for more than ten years without any accident, then you should make a point of it in your new insurance. Not everybody has the possibility to do so, but there is another trick. One can for example insure the car on another person or include a driver with more experience into the policy. Mixing a high risk and a low risk profile will in most cases reduce the insurance. Therefore, one should check who is a low risk profile. Statistically older or female drivers will fall in this category. Listing such as the main driver in one’s car insurance policy, can save some money.

Each car is categorized with a certain amount of insurance money that the owner has to pay. It is generally known that the bigger the engine of the car, the higher is this amount. The reasoning of the car insurance companies is the higher risk. Statistically cars with a higher engine are more likely to crash. For obvious reasons insurances are all about statistics. So if you can beat the statistic, you will save some money. Most people will not modify their car, however there are car enthusiasts that do. A simple engine tweak or any other car modification can quickly become very expensive. What seems like a body shop bargain, can become a killer within the insurance policy. Therefore, it is worthwhile to check with your car insurance whether an upgrade is necessary.

Of course one could say that the insurance company doesn’t have to know. This is however an extremely risky undertaking. In case you do have an accident with your modified car and you haven’t notified your insurance about it, you can loose your cover immediately. Even if you haven’t caused the accident, the insurance company can refuse to pay anything. Hence, one shouldn’t modify outside the regulations of the Land Transport Authority (LTA) and definitely not keep it a secret. Handling your car insurance correctly doesn’t take too long and can award you with some extra cash.

“Do you want travel insurance?”, a sentence has become so common that it is now included in the menu of tour packages and online travel booking. While some of us may be guilty of travelling without getting covered, travel insurance has now evolved into a need rather than a want.

Ask yourself these questions:

Who will evacuate you when you are injured on top of Mount Fuji?

Who will bear the cost of cancelled air tickets or tour package during the protests in Hong Kong? A flood in Australia? Or if you and your travel companion is hospitalized days before your travel?

Who will be the one you call when you are terribly ill in Europe? Or when your rented car has crashed into a monumental sculpture?

Who will cover the cost of your essentials when you lost your baggage or your travel documents?

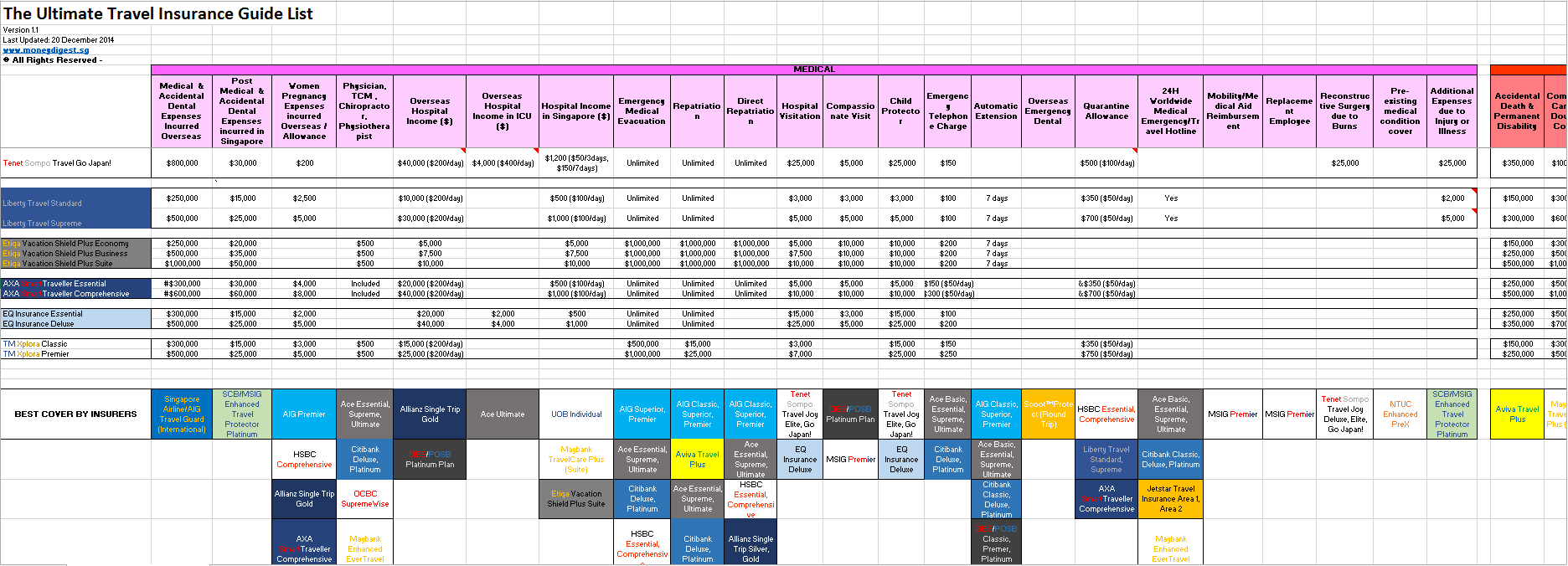

The list can go on but instead of trying to spoil your holiday planning, we have come up with a guide for you to compare travel insurance plans in Singapore.

We had compiled the data across different insurance companies so that you can have an idea of which offer the best cover for each risks you identified as well as getting the cheapest travel insurance in Singapore.

Let us first examine a few common benefits that you should be looking at when purchasing a travel insurance.

Medical treatment and emergency evacuation

(Image credit: Phalinn Ooi, via Flickr)

Sure, you can be as healthy as a horse but you can’t avoid getting hit by someone skiing down the mountain or prevent a dengue mosquito that wants to sting you. Shit happens, and that could cost you ten or thousands of dollars when you are overseas. It is not too bad if there is a hospital nearby but what if you are trekking on the remotest part of the island? Emergency medical evacuation could easily set you back between $75,000 – $300,000.

You don’t want me to add the medical expenses, do you?

From our list, Singapore Airline Travel Guard offers the best cover for medical and accidental dental expenses when you are overseas. You can claim unlimited benefits from their International plan underwritten by AIG. For emergency evacuation and repatriation, there are many companies that offer unlimited cover, including AIG’s own flagship Travel Guard plans. The word ‘unlimited’ is equivalent to a peace of mind that is important to all travelers, including myself.

Accidental death and permanent disability

(Image credit: Dominik Golenia, via Flickr)

Should the most unfortunate event that results in death and permanent disability, there is an additional payout to you and your family members. Aviva offers the highest coverage of up to $2million to protect you and you family from the liability of you suffering from permanently incapacitatation or premature death.

Hospital income

(Image credit: aenri05, via Flickr)

Whether you are hospitalized overseas or in Singapore, it may take weeks or months for you to recuperate. If you are still employed, you may end up having to take no-pay leaves and this could come in handy when you receive a daily income for your stay in hospital. It makes sense when you still have you bills and mortgage to pay and a parents to support. DBS TravellerShield and Allianz Gold plan has the best overseas hospital income benefits with the highest limit of $50,000, with the latter paying you $250 a day. (vs $200 a day from DBS)

However, if you are hospitalized in Singapore, a plan from UOB, Maybank’s TravelCare (Suite) and Etiqa’s Vacation Shield Plus (Suite) make more sense as they have the highest limit of $10,000.

So which should you choose?

Besides comparing the premium amounts, take the destination you will be travelling to into consideration and if it is located far away from Singapore. That is to say if you are travelling to Europe or the US where it may be difficult to transport you back to Singapore for local treatment, then overseas hospital income should be your priority. Whereas if you are travelling to a country in South East Asia, you should be looking at a higher hospital income limit in Singapore.

Travel cancellation, curtailment and disruption

(Image credit: Ross G. Strachan, via Flickr)

When you have spend thousands of dollars booking your tour package or air tickets months in advance, you may well want to get this covered. Some airlines offer a non-refundable air tickets and should you have a last minute cancellation due to serious illness, riots or flash flood, your month-worth of paycheck would be down in the drain.

Allianz Gold plan beat all other plans hands down as it tops the list of benefits with a $25,000 limit for travel cancellation, postponement, curtailment and interruption.

Delay or loss of personal baggage

(Image credit: donuzz, via Flickr)

Most people buy travel insurance to protect their baggage and belongings as it seems to be the most common mishap that could happen on a trip. Again, Allianz has outshone the rest with a $15,000 cover on personal baggage and a $10,000 cover on travel documents. However for baggage and travel delays, Etiqa Vacation Shield Plus Suite is a better option with a $5,000 limit.

Other benefits such as golf benefits, home cover, car rental excess and more

If you are planning to go on a green trip, golf benefits may be more attractive as you are covered from things such as loss or damage to your golf equipment to getting an incentive for getting a hole-in-one. With up to $3,000 cover limit for your golf equipments, golf junkies look no further to HSBC Comprehensive and AXA SmartTraveller plans. If you on your way to become Tiger Woods, Ace Ultimate plan will offer the highest bounty for a hole-in-one, currently at $750.

Insurance companies has gotten more creative over the years. From offering you cash incentive such as a hole-in-one, you can get covered at almost anything you can think of such as reimbursement for pet medical care to protecting your home from any damages. Besides taking into account of the benefits offered by insurers, you should also compare the premiums to make sure you get the most value for the cover.

Read the fine prints of the policy as some insurers define each benefits differently. For example, some insurer requires you to seek medical advice or treatment when you are overseas to be eligible to claim for your medical expenses incurred in Singapore, while some allow you to claim if you seek medical advice within 48 hours of returning to Singapore.

In short, some of the most common benefits are highlighted below:

Benefits

Recommended plans

Overseas Medical Expenses

Singapore Airline Travel Guard (International)

Medical Expenses in Singapore

SCB Enhanced Travel Protector Platinum

Overseas Hospital Income

Allianz Single Trip Gold, DBS Platinum Plan

Hospital Income in Singapore

UOB Individual, Maybank TravelCare Plus (Suite), Etiqa Vacation Shield Plus Suite

Emergency Medical Evacuation/Repatriation

AIG Travel Guard Superior/Premier, Ace Essential/Supreme/Ultimate, HSBC Essential/Comprehensive, Allianz Single Trip Silver/Gold, Tenet Sompo Travel Joy Deluxe, AXA SmartTraveller Essential/Comprehensive

Pre-existing medical conditions

NTUC Enhanced PreX

Child education grant, family assistance

MSIG Premier

Accidental Death & Permanent Disability

Aviva Travel Plus

Travel cancellation, postponement, etc

Allianz Single Trip Gold

Travel baggage delay, overbooking and misconnection

Etiqa Vacation Shield Plus Suite

Golf benefits

HSBC Comprehensive, AXA SmartTraveller Comprehensive

Visit our Travel Insurance Guide for a full list of benefits and the respective premiums of each insurers.