DIYInsurance (Do It Your way Insurance) is Singapore’s First Life Insurance Comparison Web Portal launched in June 2014.

As its name suggests, you can now purchase insurance based on your own agenda and not the insurance agent’s agenda. Besides having the option to compare different kind of insurance plans across various insurers, they also rebate 30% of the commissions back to you. That’s an added bonus for making conscientious effort to take care of your own future financial needs!

Good news for every responsible adults out there!

DIYInsurance has unveiled a first-of-its-kind insurance packages last month to provide a more holistic cover to two groups of people that require protection the most — Baby and Young Working Adult.

For every parents, the birth of your baby signifies happiness and it also means assuming greater responsibility.

As parents, we want to give the best to our children. Besides giving them a memorable childhood, we want to give them a good education and adequate medical treatment if they fall ill or get injured.

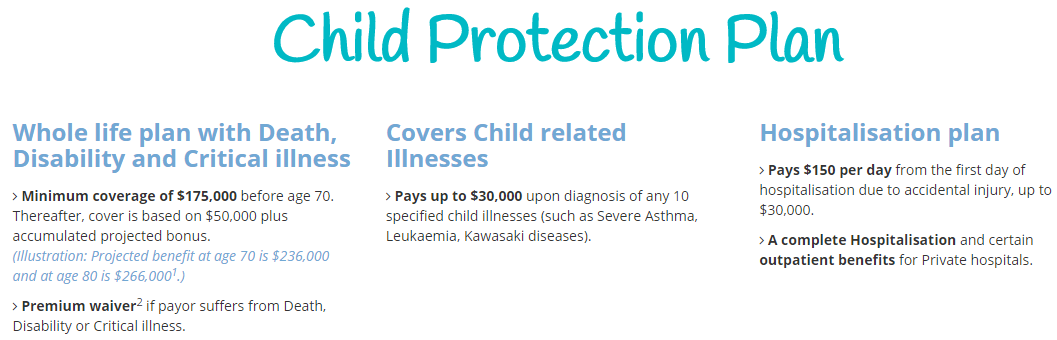

The Child Protection Plan is an insurance package that protects your newborn from day one and it covers everything from child-related critical illnesses to death and disability. A complete hospitalization plan is also included to ensure that their hospital bill are taken care of.

Premium can be as affordable as less than $100 a month, depending on your needs. For more info, visit DIYInsurance here.

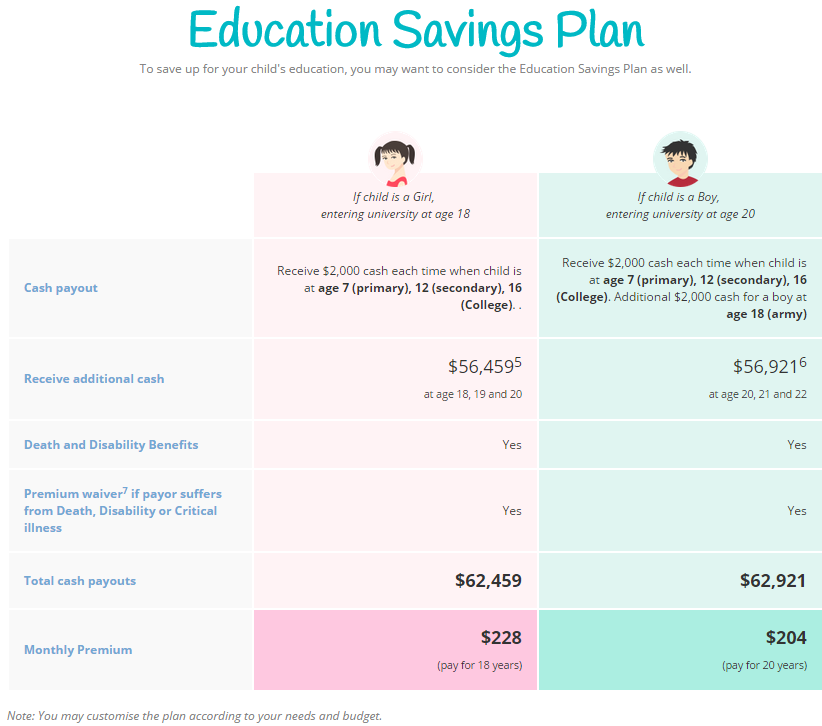

As responsible parents, we want our children’s education to be well taken care of and if your budget permits, the Baby Package also offers an Education Savings Plan that provides cash payout each time when your child reaches the next education milestone. Imagine how grateful your child will feel when they receive a cash payout of $2,000 each time they progress from Primary School to Secondary, and then to College?

An additional lump sum payment will be paid out when they turn 18, 19 and 20 (If your child is a girl) or 20, 21 and 22. (If your child is a boy)

Get rewarded for being responsible. You are entitled to cash rebates of around $300 for signing up for the Baby Package. A $50 shopping voucher will also be thrown in if you sign up for both the Child Protection Plan and the Education Savings Plan.

Enquire more about the package on DIYInsurace’s website here.

* Nobody like being shortchanged, and they understand that. DIYInsurance has also launched the Price Beater option which guarantee to offer you the best insurance deals out there. Got a better quotes from other insurers? Contact them and they’ll beat the price you have been offered and in addition they will give you up to $50 in shopping vouchers to spend! [Until 31 Dec 2015]

According to Investopedia, insurance is a binding contract or policy in which an individual receives reimbursement or financial protection against losses.

When purchasing for an insurance policy in Singapore, look for the best-priced deal that is suitable for you because prices can vary from one company to the next. Furthermore, the policies these companies offer are different. So, beyond the price, it is important to consider other factors as well.

1. FIND THE APPROPRIATE TYPE OF INSURANCE

Determine the situation you are in then, decide what type of insurance is appropriate for you. For instance, you are flying to the other side of the world for 30 days and you are worried that you might fall sick there. Do you get a medical insurance or a travel insurance? Well, if you must know, most travel insurances cover emergency medical bills during your trip too. This is why it is important to make sure you know what you want and you know what the insurance policies entails.

The easiest way to know if you qualify for the insurance policy is to check the age limits placed. If you do not then, you should ask the insurance company if there are flexible steps you could take if you do not meet the age criteria.

Age criteria determine the price and size of the premiums as well as the validity of your claims. Therefore, you must see to it that the policy terms can work for you and your dependents in the long run.

3. STUDY THE POLICY’S EXCLUSIONS AND INCLUSIONS

Before purchasing the insurance product, you need to study what the policy covers and what it does not. For instance, if you are going to buy a life insurance for your family, ask about the beneficiaries. Can you include your children and your spouse but not your parents? Again, flexibility of the policy is a factor to consider here.

4. SAVE MORE WITH ADDITIONAL BENEFITS

You can save more money if there are additional benefits attached to the insurance policy. For instance, MSIG Insurance Singapore is offering an additional 10% discount if you purchased a Travel Insurance as a group of 6-10 persons while you will get up to 15% off as a group of 11-20 persons (Terms & Conditions apply). Isn’t that amazing?

5. EXAMINE THE WAITING OR DEFERMENT PERIOD

Waiting period is the period of time before you can receive the insurance compensations after you made your claims. For example, if your motorcycle is crashed during the lengthy waiting period, you will have to find other methods of transport until it is replaced.

While, deferment period is the period of time you cannot make a claim because the insurance company has yet to make payments. For example, you fall ill in the midst deferment period then, you will have to fork the payment yourself.

Image Credits: Alan Cleaver via Flickr

These situations highlight the essence of examining whether you are comfortable with the waiting or deferment period set by the insurance company.

An insurance resource that exists for one sole purpose: to empower you to make informed decisions about your insurance purchases based on no one’s agenda except your own.

Here’s how they stood out from the rest:

30% Commission Rebates

In addition to promotions, you will receive 30% commission rebates back in cash when you purchase any product through DIYInsurance for greater cost savings to you. Learn more about commissions rebate here.

Independence

All staff from DIYInsurance are paid a fixed salary and do not participate in sales-based compensation or incentives of any kind. Not being remunerated on a commission-basis means DIYInsurance is independent and are able to focus on doing our best to fulfill your needs. There is no hard-selling and no over-selling.

DIYInsurance Rating

The DIYInsurance rating system helps you find the product which is of the best value that suits your needs. The Specialist Consulting Group with expertise insurance knowledge, compiles, analyses, compares, updates and research products distributed by insurance companies based on features and price. Based on the product’s value, it is converted to the number of stars as displayed in the comparison platform.

My house has got a whole new look – thanks to the interior designers which put the furniture and fittings in place. The family car which has served us well for months has just went for a major servicing after running for another 40km. And i just had my dinner in a restaurant – a bento set prepared by Japanese chefs.

The services sector is paramount to the Singapore economy and as we get more innovative, it is not uncommon to see businesses offering different value added services to meet the demand of its people. Think Uber and Helpling.

That being said, i never let a financial planner handle my finances. Why, you might ask, since they are all services that help make the life of the common folks easier?

True. We are human beings after all and we tend to follow the path of least resistance. Why burden ourselves with the technicalities on how to fix a car or the myriad ways of where to place my sofa sets? I can definitely make my own meals, but i probably can’t dish out the the Xiao Long Bao at Din Tai Fung or to enact the perfect ambiance in a fine dining restaurant.

And if things goes wrong, the most i probably have is an upset stomach or a house that looks like a hostel. (which can be easily remedied without much repercussion)

My finances? There is more to just switching to the next better plan – my future is at stake.

Taking responsibility of my own finances

As Dave Ramsey aptly put it,

Personal Finance is only 20% head knowledge. It’s 80% behavior!

Don’t get me wrong. Personal finance can be complicated if you put the dynamics of investment and financial risk into the equation. Financial planners like the insurance agent or the bankers have their place in today modern society.

But if you are the ordinary man or woman on the street, like myself, chances are you are qualified to make your own decision. The word here is qualified and by that, i don’t mean you need to be educated in the area of Banking or Finance. If you have manage to chance upon this article, you are probably savvy enough to hook yourself onto the World Wide Web. With the internet, you can do wonders with the vast amount of information and knowledge out there – from learning how to cook a Shepherd’s Pie to planning your solo trip to Europe.

Can you manage and plan your own finances using the internet? You bet!

A website with useful resources would be MoneySENSE, a national financial education programme in Singapore. It has almost everything you need to become a financial literate – from the theoretical aspect to the nifty calculators.

Financial planning involves a few steps, and while you can budget and plan for your retirement the way you want it, there is one important factor that many have overlooked. Risk.

You can craft yourself an ingenious financial plan, but it can never be perfect should something unfortunate happen yesterday and ruin it. And that’s where insurance comes into play – to transfer the risk of loss to another party (the insurer in this case)

Encounters with insurance agents

Why would i not consult the insurance agents then? Well, i did, few years ago.

After several sessions with 3 financial advisers from different companies, i have had umpteen reminders that i need to save for retirement since i’m in my twenties. Spot on. We should always start accumulating wealth early and take advantage of the effect of compounding, where returns are reinvested to generate their own earnings.

But that’s not what i’m looking for. As i already have some money invested in the Straits Time Index Exchange Traded Funds, or STI ETF, i’m looking at covering myself with term insurance to hedge the risk of loss from unexpected events.

However, I was informed that i need to diversify my investment and/or to have another account to grow my wealth so i was recommended a whole life insurance and endowment products on the basis that i need another saving plan. I was also informed that term plans has no cash value and i’m just throwing my money into the drain.

Being the skeptical me, i was not sold to their recommendation and furthermore i have just started working with not much funds for any other products.

Online Insurance Aggregators

Only recently when i came across the news that there were websites out there that actually helps you to compare the different insurance plans from different insurers, i know it’s about time to reconsider my options.

Both are similar as they serve as a platform for consumers to compare the different insurance policies out there. They also provide handy calculators for you to work out the amount of coverage you need without consulting the insurance salesperson.

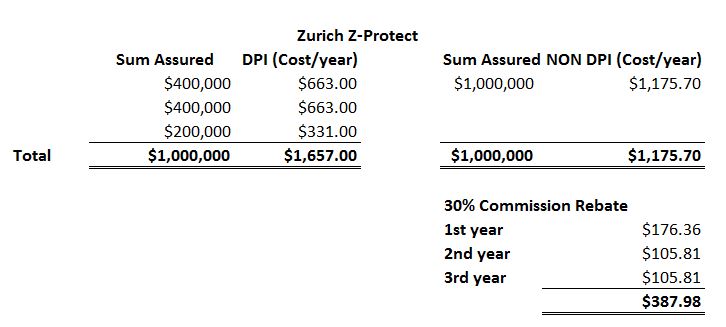

compareFIRST has a comprehensive list where you get to compare different insurance companies in Singapore. It even allows you to compare Direct Purchase Insurance (DPI), which is purchased directly from the company without any commission charged. The limitations of DPI is you can only purchase up to $400K of sum assured with a fixed term of 5 years, 20 years and up to age 65.

As i have calculated my need to insure myself up to $1 million, i could not take advantage of the more affordable DPI. I could have purchase two policies of $400K and one policy with $200K sum assured, but that is not cost-effective than if i were to purchase a single jumbo term insurance from a company.

Usually, insurance companies offer a substantial discount if you were to purchase a large term plans. I have used quotes obtained for Zurich Z-Protect in this example and as you can see, i end up paying $481.30 more a year if i were to purchase 3 separate DPI policies than a single non-DPI policy.

As its name suggest, you have to do your own planning and calculate your own needs and because of that they rebates 30% of the commission from non-DPI policies back to the customer. That works out to be a saving of around $387 (good enough to purchase a pair of Scoot economy tickets to Bangkok.)

If you think that you probably get little or no services because of doing it yourself, you are wrong.

Mr Christopher Tan, CEO of Providend said:

Instead of asking our insurance specialist to work out the insurance recommendations for you, we put that advice on the portal by way of the comparison tool. But anytime you need help or advice, you can always email, call or web chat our licensed and trained client service managers. Having said the above, when you come in for documentation, we will still do a final check for you to make sure your planning have been sound and we will still provide you with product advice, meaning, we will explain in detail the insurance you are buying.

That is basically saying you are getting your insurance with services – for less. Don’t worry about getting into sales talk with their client service managers because they are remunerated a fixed salary with no commission, so independent and transparency is the key here.

In conclusion

By taking responsibility of your own finances and doing it yourself, you not only save money but you also have a clearer picture of your own future – which means more flexibility to adapt to changes in different life stages. Would you rather be dependent and scramble to look for your insurance agent many years down the road when you get married, have your first child or buy your first apartment?

Not all life insurance agents are trusted advisors. So, the simplest way to prevent being exploited is to seek for an independent agent that will save you time and money. Here are the other secrets that your Life Insurance Agent may be keeping from you…

1. THEIR INCOME IS BASED ON COMMISSION

The agent’s income is solely compensated from the commission. It is one of the possibilities for the agent to have a personal interest that leads to you buying the highest premium possible equating to their highest commission possible. Thus, it may change his/her perspective of things, as well as the type of products clients are introduced to.

2. CASH VALUE WILL NOT BENEFIT YOU RIGHT AWAY

Yes! Cash value will build-up. But it takes about five years to have the cash value equal to the amount you paid for the whole life insurance.

3. BUY TERM AND INVEST THE DIFFERENCE

The term insurance is significantly less expensive than the whole insurance. This is why you can buy term then invest the difference on mutual funds. In fact, the combination of term and your investment for mutual funds may be less costly that the whole life insurance.

4. YOU MAY NOT NEED CHILD LIFE INSURANCE AFTER ALL

Renowned experts namely: Dave Ramsay, Suze Orman, and Neal Frankle are on a arguing against buying life insurance for kids.

“The only reason you need life insurance is if anyone is dependent on your income…please, you new parents, do not let anyone talk you into buying a life insurance policy on your child.” said Suze Orman.

Image Credits: State Farm via Flickr

According to them, if your child is not at the risk of a serious illness and you are financially stable to cover foreseen medical bills then, you are better off without it. Instead, save up for your child’s education until tertiary level.