Micro-investing has emerged as one of the most accessible ways for Singaporeans to enter the financial markets without the stress of committing large sums. The idea is straightforward. You invest small amounts at regular intervals, often through mobile apps that automate everything from deposits to portfolio allocation. With fractional shares and exchange traded funds available for as little as S$1, even the smallest contributions begin to take shape as a genuine portfolio over time.

Its appeal lies in simplicity and confidence building. Micro-investing eliminates the belief that serious investing requires substantial capital. User friendly apps guide beginners at their own pace and budget, making the learning curve far less intimidating. The automated nature of these platforms also encourages discipline. When contributions occur quietly in the background, saving becomes habitual rather than aspirational. Over time, these habits compound and can meaningfully influence long term financial health. Even with limited funds, investors can achieve diversification by spreading small amounts across sectors, markets, and asset classes.

However, micro-investing is not without its drawbacks, particularly when it comes to cost. Round up apps may be convenient, but they often charge a flat fee regardless of account size. Some popular platforms start at about S$4 per month, which translates to roughly S$37 per year. This may not seem significant, but if you are investing only S$7 to S$13 a month, the fees can quickly outweigh your early returns. Many platforms operate on similar fixed fee structures, which can erode gains until the portfolio grows large enough to absorb these charges. Growth potential also remains modest unless contributions increase steadily. Small amounts will yield small results in the early years, which means micro-investing alone might not support major long term goals such as retirement or home purchases. Volatile markets can also feel more discouraging when account values are still small, as fluctuations appear more pronounced.

Image Credits: unsplash.com

Despite these limitations, the true value of micro-investing lies in habit formation and long term discipline. Small recurring contributions serve as early training for future investment behavior. They introduce new investors to market movements while reinforcing consistency. A simple projection illustrates the impact. Investing S$27 per month at a ten percent annual return grows to about S$339 after one year from S$324 in contributions. After ten years, it becomes roughly S$5,531. After thirty years, it surpasses S$61,033 from just S$9,720 in total contributions. These figures show how time and compound interest can turn modest amounts into meaningful progress. Micro-investing may start small, but it builds momentum. As contributions rise alongside income and confidence, it can become the gateway to a stronger, more resilient investment journey.

Investors of any age would do well to revise their current portfolios when they take age, risk appetite, retirement goals, understanding and correlation to other assets in the portfolio into consideration.

The rise of fintech now adds alternative assets like peer-to-peer lending, cryptocurrencies and microloans to the sheer variety of investment options. No longer do investors contend with just commodities, stocks, bonds and real estate.

Investors who accept that there isn’t a one-size-fits-all solution to building a diversified portfolio stand to do better. Here are general principles on finding the asset class that’s right for each investor portfolio.

1. Age and investment horizon

Assets behave as they should when given the time to do so. For example, it’s a well known saying that stocks outperform bonds; which is more likely to be true over a longer investment horizon.

Stocks will almost certainly outperform bonds over the next 30 years, for example, as fundamental facts like inflation make this outcome the most probable. But no one knows for certain if stocks will outperform bonds next year, or the year after, especially with the current Sino-US trade war.

As such, when considering the performance of any asset class, it is important to understand that the more time you give it, the more likely the asset will perform as expected. Wealth managers may tell clients to reallocate from equities to bonds when they get older.

In general, older investors will want to favour fixed income securities, be they perps or simple annuities, while younger investors can be more aggressive. Given their longer investment horizon, younger investors can pursue long-term capital gains, and expect their assets to behave more or less planned.

2. Financial goals, risk appetite and capacity

Personal financial goals is as much about psychology as mathematics. An asset class must meet the risk appetite, or “sleeping point”, to prevent stress or impulsive moves.

For example, there may be many good reasons why cryptocurrency fits a particular investor’s portfolio. She is young, affluent, and such an investment would make up only 5% of her portfolio. But if she is risk-averse and uncomfortable with volatility, the sleepless nights and stress may outweigh the value of the asset, regardless of what the numbers suggest.

If the risk is beyond the investor’s appetite, there is also an increased likelihood that an investor will derail their long-term financial goals. A news report on falling cryptocurrency prices, for example, could set off a panic that results in offloading the asset and incurring a loss.

In general, monthly obligations, inclusive of a home mortgage and premiums for an endowment plan, should not exceed 40% of an investor’s monthly income. Any asset class that pushes beyond this limit is likely taking them past their risk capacity.

3. How the asset class fits within quantified retirement goals

When deciding to invest in an asset class, investors should have quantifiable goals and ways to measure outcomes.

For example, an investor should have a clear idea on how much they need by the age of 65 to retire, with an income replacement rate of at least 80%. Only then is information about an asset class’ historical returns useful.

Investors should also note that every asset class rises in value over time. They need to ensure the returns are sizeable and fast enough to meet quantified retirement goals.

Some examples include microloans tailored towards invoice financing for small businesses. These commit capital for terms of at most 12 months, which limits what investors can lose while ramping up returns to make up for the shorter investment horizon. Late starters with 20 years or fewer to retirement, can consider these alternatives to conventional assets, such as stocks or bonds.

4. Education and understanding of the asset

Investing in a poorly understood asset means ignoring risk appetite, as the investor tends to overestimate or underestimate the risk involved. Without proper education and understanding of the asset, there are also important subtleties within asset classes that investors may miss.

For example, investing in peer-to-peer lending is often perceived as being high risk. But this varies greatly based on the jurisdiction and platform. While China is struggling with it as a shadow banking problem, peer-to-peer lenders in Singapore and Malaysia have seen default rates of less than 1%, even lower than the default rate suffered by some commercial banks.

Many investors in Exchange Traded Funds (ETFS) may have also ignored that a partial replication ETF does not include smaller stocks by market cap. In the event of a small-cap led bull run, this can result in the ETF yielding lower returns than the benchmark.

5. A low correlation to other assets in the portfolio

Before introducing a new asset class, it is best to confirm that there is a low correlation to other assets in the portfolio. Strong correlations might mean a lack of diversification.

For example, an investor who already owns commercial retail properties might reconsider investing in a commercial Real Estate Investment Trust (REIT) that is heavy on malls. A downturn in the retail industry would impact both the REIT and real estate.

The correct mix of assets varies for each individual. But as a near-universal principle, investors should avoid banking too heavily on the same interlinked group of assets. A qualified wealth manager should be consulted on the right mix for each portfolio.

Looking beyond conventional assets

For a truly diversified portfolio, investors should think of asset classes beyond stocks, bonds and real estate. The emergence of fintech has given rise to peer-to-peer loans and microloans which offer unprecedented opportunities for high growth in a low interest rate environment.

Some new asset classes are also structured in a way to mitigate risks found in conventional assets, such as long maturity periods, opaque structures, and high initial cash outlays.

By taking various factors into serious consideration, investors of any age would do well to revise their current portfolios and look for new alternatives that can complement or replace older asset classes.

About the contributor

X.Y. Ng is VP, Brand and Digital at Validus Capital, a leading growth-financing fintech platform that connects accredited investors with growing SMEs across Southeast Asia.

The world is seemingly getting smaller every day. Online platforms, newspapers and financial television stations usually monitor events happening in one country that can have effect on other countries worldwide. People are now updated and interconnected compared to any other time in the history. It is without doubt that globalization has its own advantages, but when economic crisis, global recession, war and trade imbalances occur, it suddenly leads to the idea of making safer investments and working on government deficits. The occurrence of such uncertainties can even confuse experienced investors.

Uncertainty

Every time an individual risks his money for a chance to make profit, there is always a level of uncertainty. When fresh threats such as political unrest, recession and war arise, levels of uncertainty increase rapidly as organizations can no longer correctly predict future trends and earnings. As a result, influential investors will cut their holding in stocks significantly where they consider it unsafe and transfer their funds to other sectors such as government bonds, precious metals and money –markets ventures. The results of the sell-off when large portfolios are repositioning themselves, causes the stock market to be unattractive for both small and big investors.

Effects of uncertainty

Uncertainty can be termed as the inability to predict future trends and events. Investors cannot be able to predict the possibility of a recession, how much it will cost, when it going to start or end or which organizations will be able to make it through without being affected. Most organizations usually make predictions of productions and sales trends to give public the confidence to invest in normal market conditions, but changing uncertainty levels can result in inaccurate prediction. Uncertainty can affect economic situations both at macro and micro levels. At micro level, uncertainty focuses on particular companies within an economy that is faced with recession or war, whereas on the other hand, uncertainty on the macro level focuses on the economy as a whole.

On a micro- level company perspective, uncertainty is a major concern for companies that deal with consumer goods and services on daily basis. Consumption can fall rapidly if there is a threat of recession as customers refrain from buying goods and services. As a result, uncertainty can cause organizations to lay off some of its employees in certain sectors to reduce the effects of lower sales. Uncertainty levels that surround company sales also affect the stock market.

On macro level perspective, uncertainty is expanded when the countries at recession or war are major consumers or suppliers of goods and services. For example, a country that supplies huge amounts of oils goes to war, uncertainty concerning the levels of globe oil reserves would increase significantly.

Another macro- level event that brings in uncertainty is the devaluation of exchange rates. Countries that are faced with recession and war are deemed to be unstable. Therefore, investors tend to move their currency and investments away from these countries.

How to react

When uncertainty situations heighten, the best weapon is to be well informed about all the events occurring worldwide. One can research individual companies, read newspapers and watch financial televisions to keep updated. It is also critical to analyse sectors that are likely to gain more and the ones that are going to lose during the crisis and choose a long term plan to invest. In addition, uncertainty times are also a good opportunity for investors who position themselves to take advantage of the situation. Brilliant investors will search for companies that provide goods and services that will be in high demand when the situation normalizes. However, it is very hard to commit investments in uncertainty situations, but one can reap huge benefits in the long run.

Online Forex traders such as CMC markets and their clients are good example of investors who should be updated about uncertainty. CMC markets operate in many currencies and therefore it is critical to monitor the performance of every currency. When a certain currency becomes weak because of a various uncertainties, it is advisable for traders to change and trade with other stronger currencies. Where a possibility of situations normalizing, traders can take the risk and hang on to reap the huge benefit that’s come along with such situations.

Singapore investors love their dividend stocks. According to the Investment Trends Singapore Broking Report 2015, 75% of investors polled stated that they usually invest in dividend stocks when trading on the Singapore market. And they are spoilt for choice! Many companies that list on SGX pay dividends. But with so many dividend-paying stocks out there, which stock would you consider?

A High Dividend Yield Stock: Better than a Low Dividend Yield Stock or?

That is the question. The stock with the highest dividend yield in the industry may look attractive now, but is a stock with 10% dividend yield better than one with 3% in the long run? Does a high yield stock always outperform a low yield stock?

High dividend yield should not be taken at face value. It always pays to dig deeper and find out the real story behind certain attractive numbers before deciding to invest.

Companies with a high dividend yield compared to the market average may not necessarily equate to companies with good financial performance. The high dividend yield could be the result of declining share price due to weak fundamental such as inconsistent earnings, high debt etc. Besides, high dividend yield may not be sustainable. If earnings fall, the management may cut dividends or eliminate the pay-out altogether. Hence, investors should also look at companies with consistent dividend payouts and with the cash flows coming from actual core operations.

A Dividend Growth Strategy

If a stock with a high dividend yield is not necessarily the best choice for long-term investors, then what other strategies are there? A dividend growth strategy for one, is something you might want to learn more about.

To clarify, dividend yield is the dividend amount divided by the share price. Dividend growth meanwhile is how much the dollar-amount of dividends given out increases each year.

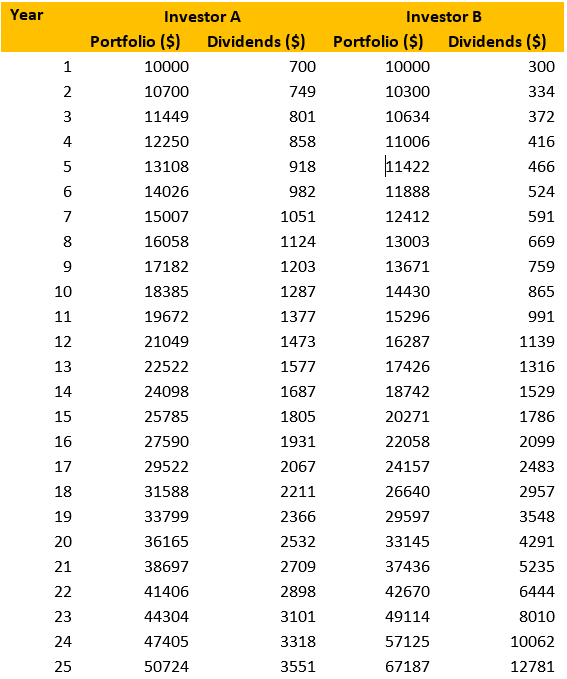

Take this hypothetical example which compares the performance of two investors (based on certain assumptions where indicated).

Investor A: Invests in ABC Company which pays 7% dividend yield at the outset and every year after that.

Investor B: Invests in XYZ Company which pays 3% dividend yield at the outset.

XYZ Company has a lower dividend yield because they choose to reinvest some of their earnings into the business. The business grows, and so does their dividend pay-out – to the tune of 8% every year (e.g. $0.03 dividend per share in year 1, $0.032 in year 2).

Assume that the share prices for both of these companies remain unchanged for 25 years and both investors reinvested their dividends every year. Their performance can be found in the table below.

The Results Investor A, the high yield investor, beats Investor B during the beginning years but the dividend pay-out and portfolio value of Investor B caught up in year 16 and 22 respectively. In the end, the total dividends received by Investor B are more than 3 times that of Investor A.

So, while Investor B received low pay-outs initially, he was rewarded with future growth. This is the underlying principle of the dividend growth investing strategy. Length of the period of investment would also affect the total dividends received.

Finding Dividend Growth Stocks

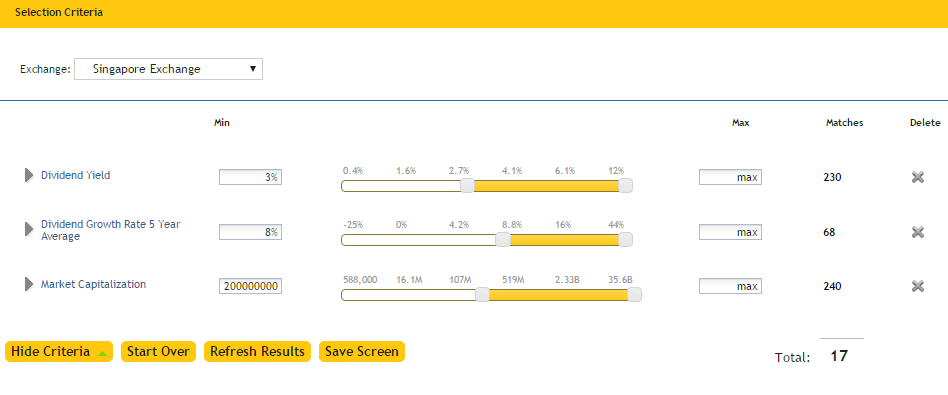

That will be the next question on your mind if you want to explore using a dividend growth strategy. Stock screeners come in useful here. A stock screener allows you to choose certain criteria, and to find stocks that fit the criteria you have selected.

Here is a set of criteria that could be used to pull dividend growth stocks:

Dividend yield>3%

Market capitalisation>200 million

Dividend growth rate (5-year average)>8%.

The stock screener below, for example, has found 17 stocks that match the above criteria. This provides a good starting point for investors to do further research into these specific stocks. Try to come up with your own set of criteria and see how it works.

Source: Recognia Strategy Builder on Maybank Kim Eng’s KE Trade platform as at March 2016

Disclaimer: This message is for general knowledge or information only. It is not an offer or invitation to buy or sell securities, futures or other products or services. Our products or services vary in different jurisdictions, subject to their respective terms and conditions and the licences our affiliates and us hold. This message is not an advice or recommendation for any financial planning, investment, legal, tax or other purposes and, accordingly, no responsibility or liability is assumed by us or our affiliates, whether directly or indirectly, from any person taking or not taking action

A wealth manager offers a high-level professional service which combines investment advice, accounting services, tax services, retirement planning, and legal planning. Generally speaking, wealth management is more than just about investments as it encompasses all the areas of one’s financial life.

Because of the pervasive nature of wealth management, a crucial factor affecting its success is your personality. Understanding your own personality toward money will help you identify the factors that are beneficial and harmful to your wealth. Start identifying which personality category you belong to. This can increase your self-awareness as well as take the right wealth management plan.

THE IMPULSIVE BUYER

A prey to bargains and sales, an impulsive buyer is a person who hates shopping lists and likes to go with the flow. He or she achieves psychological gratification through spending money on things that are often unnecessary. The urge to spend is usually regretted.

Image Credits: pixabay.com (CC0 Public Domain)

Solution: Remove the immediate ability to spend by keeping all your credit cards at home and by bringing nothing but a substantial amount of cash.

THE UNCONTROLLABLE DEBTOR

Falling under the umbrella of spenders, the uncontrollable debtor borrows money that he or she will readily spend. They are at risk of incurring high amounts of debts, impaling their credit score, and bankruptcy itself. With an outstanding amounts of debts, no successful wealth management can take place.

Image Credits: pixabay.com (CC0 Public Domain)

Solution: Identify all your debts and rank them according to interests. Start by ceasing the debts with higher interests and progress from there.

THE CAUTIOUS MANAGER

Unlike the two personalities mentioned above, the cautious manager likes lists and plans. People in this category also love to spot the greatest deals for their money.

Personally, I consider myself as a cautious manager. I keep track of my monthly expenses in order to analyze my spending habits. In terms of my wealth management efforts, I am very conservative that I invested my money on Mutual Funds (Bonds) alone.

Image Credits: pixabay.com (CC0 Public Domain)

Solution: As you take lesser risks, look for the savings account that offer the highest interest rates.

THE SMART INVESTOR

The smart investor is capable of managing his or her own money well. People under this category have a clearer understanding of their financial situation and they are actively putting their money to work.

Solution: Improve your knowledge on in-depth topics on investments and wealth management through several resources such as books and online articles.