The magical story of a young wizard named Harry Potter has captured the hearts of fans of all ages and with a good reason. In fact, I am wearing my Hufflepuff shirt while I am writing this.

Despite being in a fictional world, the Harry Potter characters’ financial problems cannot be solved with a wave of a wand. They also have to struggle with the challenges of saving, spending, and growing money throughout the series. Here are just some of the personal finance lessons that you can learn form the wizarding world of Harry Potter:

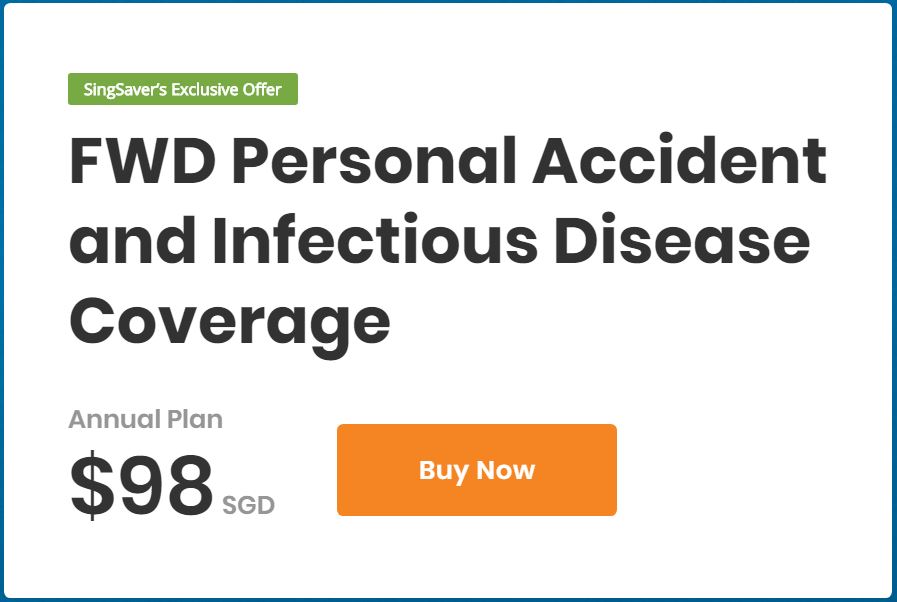

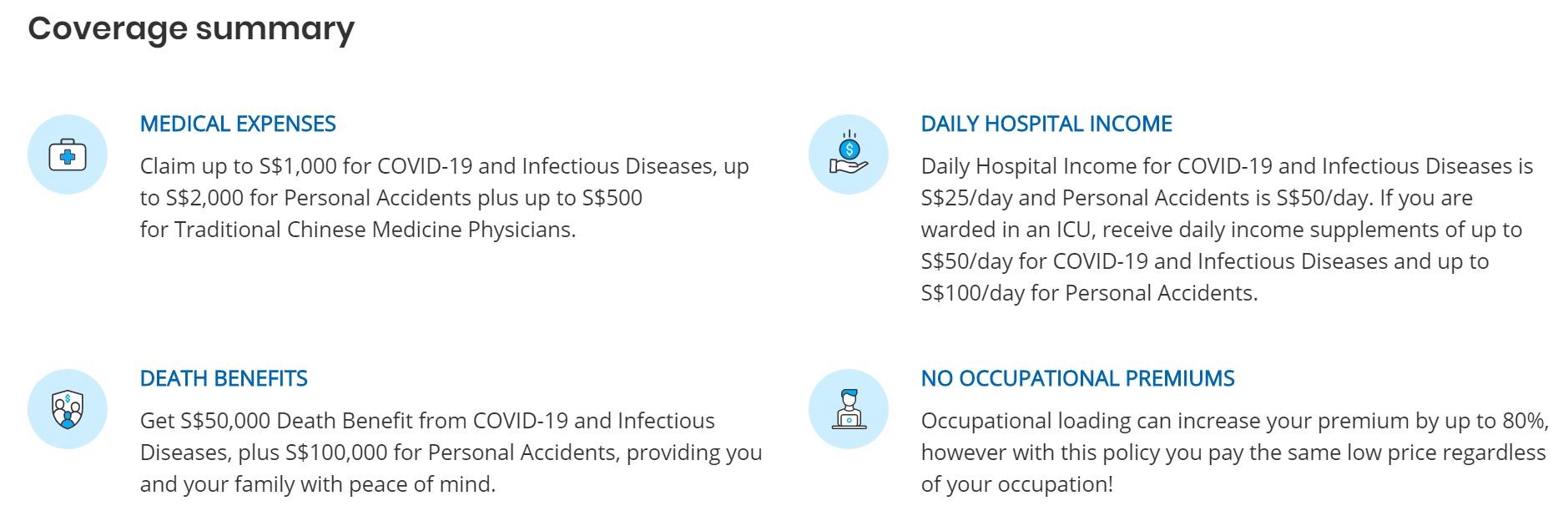

GET THE A DEPENDABLE AUTO-INSURANCE

In the “Harry Potter and the Chamber of Secrets” book, Ron and Harry crashed a car into a tree. It caused an irreparable damage to a car that they do not own. This scenario taught us the importance of having a car insurance.

In Singapore, it is mandatory to have your car insured. Examine your options and look for an auto-insurance that suits your needs and your budget. Some of the plans that you may consider are the FWD, Aviva, and NTUC Income auto-insurance plans. FWD has three auto-insurance plans from Classic to Prestige. Its annual premiums start from S$731.38. Aviva offers three auto-insurance plans too from Lite to Prestige. Its annual premiums start from S$883.12. Lastly, NTUC Income has Drivo Classic and Premium plans. Its annual premiums start from S$$970.35. Annual premiums are usually based on the driver’s profile and the car itself.

SORT OUT YOUR WILL

After living in an uncomfortable cupboard under the stairs for eleven years, the book’s main protagonist Harry Potter found out that he was a wizard and that his parents left him a considerable amount of money. His family’s wealth was beyond what he can imagine! Although his parents died at a very young age, when he was just a baby, it was clear that they a robust financial plan in place. They left all their wealth to Harry. This helped him secure his school supplies and daily needs throughout the years.

Unforeseen events can strike at any moment. It is important to save up for your retirement as soon as possible. Moreover, you must create a will that ensures the list of beneficiaries on all of your savings and investment accounts.

SEE THE POWER OF COMPOUND INTEREST

Harry not only benefits from his parents’ wealth, but also reap the rewards of compound interest. His money was untouched for eleven years. When he opened his vault for the first time at the Gringotts Wizarding Bank, he discovered the amount of gold and money that was in his vault. Despite having this wealth, he did not lead a lavish lifestyle.

Like Harry, you may benefit from compound interest by leaving your money untouched for years in a bank or by investing your money for the long haul.

APPRECIATE WHAT YOU HAVE

As I said above, he did not lead a lavish lifestyle. Harry was humble. In fact, he wore the same glasses for seven years. He appreciates what he has and exemplifies this trait the most in the first book. When Hagrid gifts him Hedwig the owl, he was amazed and accepted it wholeheartedly. He was also very grateful when he was gifted the Nimbus 2000 by Professor McGonagall.

In our world, it is easy to be caught by all the sale items and designer brands. However, you must remember to strike a balance between your needs and wants. Appreciate what you have and live within a realistic budget that you set.

SECURE YOUR MONEY IN A SAFE PLACE

Harry’s immense fortune was stored in the Gringotts Wizarding Bank, located in the heart of London. The bank is operated and guarded by goblins. These goblins serve as the gatekeepers to the underground vaults. It is often described as the safest place in the Wizarding World.

Image Credits: unsplash.com

While you cannot keep your wealth within the protection of magical spells and goblins, you can secure your money in other ways. Firstly, you may set up an auto-deposit scheme to send a portion of each paycheck to your savings account. Secondly, you may store your emergency fund in a place where you will not be tempted to spend it frivolously. For instance, you may set up a different account exclusively for that. Lastly, secure your online banking apps through Two-Factor Authentication.