As Central Provident Fund (CPF) marks its 70th anniversary, several key policy changes are being rolled out in 2025 to strengthen long-term financial security for Singaporeans. While many of these updates target older workers and retirees, younger adults are encouraged to understand these changes early to plan effectively for the future.

CPF CONTRIBUTIONS FOR SENIOR WORKERS INCREASED

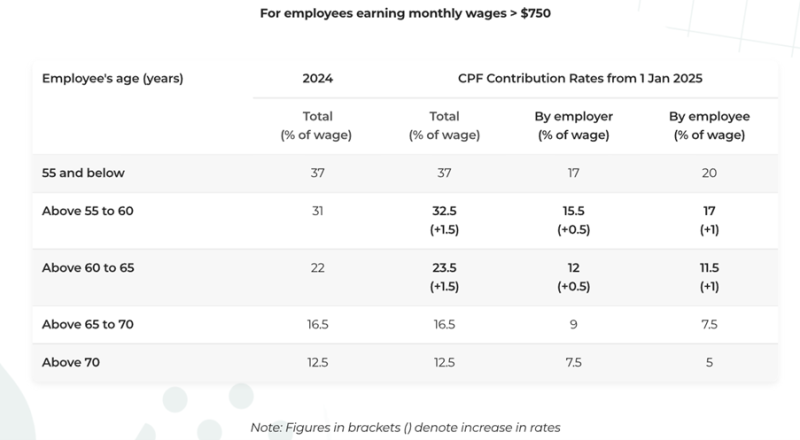

Since earlier this year, CPF contribution rates for employees aged above 55 to 65 have gone up by a total of 1.5 percentage points. This includes an additional 1% from employees and 0.5% from employers. The aim is to help senior workers build stronger retirement savings as more choose to work beyond age 55. For younger workers, this underscores CPF’s commitment to retirement adequacy for all age groups.

Image Credits: cpf.gov.sg

CPF SALARY CEILING HAS INCREASED

The CPF monthly salary ceiling has increased to S$7,400, up from S$6,800 previously. This change means that a larger portion of higher earners’ wages is now subject to CPF contributions. The ceiling will be raised again to S$8,000 in 2026. Although this change primarily affects those with higher salaries, it benefits long-term savings by increasing CPF contributions over time. This is something younger professionals can factor into their career and income growth.

SPECIAL ACCOUNT CLOSURE AT AGE 55

CPF members turning 55 this year will see their Special Account (SA) automatically closed. Funds are first transferred to the Retirement Account (RA), up to the Full Retirement Sum (FRS), where they continue to earn attractive long-term interest. Any remaining withdrawable balance is moved to the Ordinary Account (OA) and earns a lower interest rate.

Members can still transfer OA savings to their RA, up to the Enhanced Retirement Sum (ERS), to enjoy higher CPF LIFE payouts. Investments under the CPF Investment Scheme-Special Account are not affected and can be retained. Upon maturity or sale, the proceeds will first go to the RA, and any excess will be credited to the OA.

ENHANCED RETIREMENT SUM NOW S$426,000

The Enhanced Retirement Sum (ERS) has been increased to S$426,000, or four times the Basic Retirement Sum. Members who top up to this new limit at age 55 could receive CPF LIFE payouts of approximately S$3,300 per month from age 65, compared to around S$2,500 previously.

Even for those still far from retirement, it’s useful to understand how topping up early can maximize compound interest. CPF’s online tools like the Retirement Payout Estimator and Retirement Dashboard help members plan based on their age and financial goals.

EXPANDED MATCHED RETIREMENT SAVINGS SCHEME

Improvements have also been made to the Matched Retirement Savings Scheme (MRSS). There is no longer an age cap, and eligible members can receive government matching grants of up to S$600 per year for five years, totaling S$2,000.

Young adults can also support older family members by topping up their RA, helping them qualify for these matching grants while enjoying personal tax relief.

70TH CELEBRATION OF CPF

At CPF’s 70th anniversary celebration on July 5 and the launch of its commemorative book “Save & Sound: 70 Years of CPF”, Senior Minister Lee Hsien Loong reflected on CPF’s key role in every Singaporean’s life (i.e., from home ownership and family support to retirement). He also noted that Singapore’s CPF system is internationally recognized as one of the most effective in the world.

Image Credits: unsplash.com

For younger Singaporeans, this is the time to stay informed, track contribution limits, plan top-ups early, and help family members maximize their CPF benefits. To learn more, visit cpf.gov.sg or follow CPF’s official platforms.