In the hustle and bustle of the city life, Singaporeans are exposed to the high economic pressures. What makes this concrete jungle thrive? Money, of course. Putting matrimony into the mix makes things more complicated.

Managing money is a complex task fraught with emotion. It is natural that conflicts can arise from time to time. To keep your marriage and finances in tact, open communication and teamwork are essential. If only more couples are having regular conversations about money issues before and after walking down the aisle then, we will less likely to have divorces.

MONETARY IMBALANCE

What will happen when there is a massive earning gap between partners? Or, when a spouse comes from a wealthy family and the other came from humble beginnings? More so, living in a single-income household is not uncommon. Sometimes, the imbalance between two people creates power play.

When power play occurs, the person who earns the most dictate the spending habits of the other. He or she will have personal spending priorities in mind. The other partner simply complies.

Handling this situation is tricky. You can either make a pre-nuptial agreement or open a joint account. Nonetheless, marriage should be founded by cooperation in all aspects.

OPPOSING PERSONALITIES

In the list of reasons why couples divorce, money is among the top answers. Friction brought by money can be due to the opposing personalities of two people. Personality towards money plays a vital part in a couple’s marital bliss or the lack thereof.

Imagine living 24/7 with a hoarder when you are a spender yourself. Or, living with someone who is a risk-avoidant when you are a risk-taker yourself. To the extreme, you may live with someone who believes that the person who dies with the most money wins. These opposing personalities can be mediated by empathy. Walk in the other person’s shoes to understand where he or she is coming from. You may also adopt your spouse’s money habits for a month to see how it works. Paying attention to money habits before and during matrimony can be beneficial. Talking about your financial views and feelings can help put both of you at ease.

OVERWHELMING DEBT

From school loans to shopping addiction, many people come to the altar bearing a financial baggage. If one partner has an outstanding mountain of debt and the other does not, this situation can spark a conflict.

In such situations, people often take solace in knowing that debts are not carried over thru the marriage. However, it is understandable to share the responsibility over housing and child care debts.

Knowing what you are getting yourself into can help you decide how to deal with it. Both partners have to be honest and non-judgmental when discussing about their financial habits and bad records. Apply several payoff strategies soon after. And, seek professional help when needed.

Like most people, you are searching for the best way to fall on the right money management track. Falling behind your money-saving goals can feel discouraging, but it’s never too late to start learning some money-saving strategies. Throughout our lives, the relationship we have to money is dynamic. We have different needs and different spending habits. If you were never paying attention to your money-making and money-spending habits, this is the right time to start.

To organize your strategy, follow the tips below. They have been tested and proven to work on multiple occasions.

Keep a closer eye on your expenses

You know how much money enters your accounts monthly, but are you fully aware of how much you spend? Keeping a closer eye on your expenses will help you identify areas where the money is spent unnecessarily. You want to know how much money you spend monthly, and you want to keep tabs of your expenses. If you’re reluctant to keeping tabs manually, consider downloading one of the numerous expense trackers online. Alternatively, you can create your own expense spreadsheet.

Still, tools like Mint.com or Tink are amazing starting points in your expense tracking journey. Some apps can even offer you small synopsis of your spending patterns. With all that information, you will be able to make better money-management decisions in the future.

Once you get deeper insights on your money spending habits, you can start to outline a budget plan. Monthly budget plans will offer you a clearer idea of how your financial situation will look like in different stages of the month. When you notice discrepancies between your plan and actual budget, adjust the first. This will ensure you are in touch with the financial reality of your household, not the theory in your plan.

To outline an accurate budget plan, include your fixed monthly expenses: utilities, cell phone bills, car insurance, rent, or mortgage payments, and so on.

Take into account variable expenses, as well. Things like gas, personal care items, and one-time expenses are also important when creating a monthly budget plan.

Don’t forget about your savings account! If you don’t have one, this might be the perfect time to open one!

Establish a clear list of financial goals

Without clear financial goals you want to achieve by creating better financial habits, you are unlikely to work things out. Your financial goals can be anything, from saving up for a home down payment to paying off a debt, to saving up for a car or for a retirement fund.

Maintaining a clear list of goals will make you focus more on achieving them. It will also help you handle your finances more carefully. Being fully aware of your financial goals will also contribute to making better financial decisions. You will be more balanced between your spending and saving habits, and you will be more motivated to find extra income streams.

Invest

Investing is a clear way of making extra money. When the money coming from a single income source is not enough to pay your monthly expenses and saving, additional streams of income can help. Financial advisors come with several investment suggestions that are proven to work. The most efficient seems to be Forex trading. Before starting your trading journey, research Forex low spread brokers. As expert traders explain, they are the most advantageous for rookie traders. Low-spread brokers are those offering the smallest difference between the Bid and Ask price. This means you can buy currencies at lower prices and sell them for higher amounts. The benefit of choosing such brokers is obvious here. Your profits will be higher, in this scenario.

Have an emergency fund

Financial emergencies are not pleasant, but they can appear at all times. Having an emergency fund for such situations will help you keep your savings untouched. Medical visits or car emergencies involve huge amounts of money.

Establish how much you want to put in your emergency fund. This will only depend on you and your financial abilities. However, the more you put in this account, the better. According to financial advisors, those who still struggle with debt should aim to have at least $1,000 in their emergency fund. Others claim that you should have at least 3 to 6 months of your living expenses in your emergency fund. It mainly depends on your ability to save so much or not.

Try to figure out how much your household is comfortable with saving for this purpose. Saving something, no matter how little, is better than finding yourself without any money in emergency situations. For the beginning, set aside $5 or $10 for emergencies, weekly. If you’re comfortable with it, increase the amount periodically.

Prioritize expenses

All people have to prioritize their expense. Ideally, your spending habits should align with your values. Do you care more about buying a new kitchen appliance, or about your summer vacation? Pick between the two. Apply the same principle to all your expenses, and you will be more likely to save money, in the long run. Apparently, financially well-off people seem to value more experiences over physical things. You could try to implement the same strategy. Because new physical things appear frequently today, obsessing over them will only lead to higher expenses. Prioritizing experiences and things that bring happiness, in the long run, is more rewarding and less expensive.

These are the basic ideas and tips recommended for people who want to save some money but are not as experienced in the matter. Your money-saving journey can begin today. It’s never too late to pick up healthy money management habits. Go at your own pace and you will be more likely to succeed. Avoid letting external pressure guide your decisions and only make those moves you are comfortable with. Of course, the rest of your family should follow your lead. Saving money as a family is more effective but it can also be more difficult to manage.

As a parent, you must guide your children’s path to financial independence. Fortunately for you, there are available online tools that can help. Start knowing your teen’s financial personality through the Financial Identity Quiz. It is a research-based tool for teens and young adults aged 16 to 24.

After determining your child’s designated identity, you must discuss its advantages and disadvantages. Give some scenarios to help them decide better.

IDENTITY 1: THE PATHFINDER

As the name suggests, Pathfinders are committed to explore their own financial paths. This does nor mean that they do not need your guidance! From time to time, you must encourage thoughtful discussions about their financial goals. Where are they headed?

To give a distinct financial path, you must challenge your child to look for a positive financial model. It can be a professor, a blogger, an author, and so on. Discuss the steps taken by your child’s financial model. How does he or she plan to achieve the same path? Start by applying similar money principles as your financial model.

IDENTITY 2: THE NOMAD

Some people know their direct paths to success and others are still exploring. Not all those who wonder are lost, but the Nomad needs a little structure in his or her financial life. Help shape your child’s financial habits by finding an ideal financial path together.

Ask your child to do his or her research on a regular basis. You can train this by giving scenarios. For instance, ask what he will do if he showed up to an event without enough cash. Will he panic when faced with late fees via a credit card billing statement? Will he ask for your help when he missed a deadline for a school activity? Also, where will he buy gas when all the petrol stations are closed? These experiences can turn to teachable moments about financial obligations.

IDENTITY 3: TENDERFOOT

You may know a friend or two who has a Tenderfoot approach to money. A Tenderfoot has the most to learn when it comes to making financial decisions. You see, this type is so careful and conservative. This can be a good thing! However, being too careful can make you miss out on other opportunities. You need to take necessary and responsible risks along the way!

Help your children make their own financial decisions by asking what they will do when they are living on their own. Will they have a roommate or live with each other? What if they had an unforeseen medical bill or job loss? How will they raise enough money to survive? Discuss what they will do when help from a parent or a guardian is hard to reach. They have to take risks on their own.

IDENTITY 4: TROOPER

Last but not the least is the personality that echoes you the most – the Trooper. It is flattering to have your child follow in your footsteps. However, you also want to guide your beloved to make his or her own mark. What would be right for you might not be right for your child. Help your child to take ownership in money matters through discussions.

Image Credits:pixabay.com

Ask your child about the last time when he or she acted independently. How did it turn out? What was the problem and solution? How did he or she felt after taking the bold action alone? Then, make your child write down a list of personal priorities that he or she would accomplish alone. These priorities will be best accompanied by research. Help your child know which decision is the best one.

The Open Electricity Market (OEM) has allowed households to switch from SP Group to other retailers to trim their electricity bills. While this has been a fantastic ride so far, it would be even better if households can make the switch with certainty on the following:

Knowing the unit rate to be paid across the entire duration of the contract

Enjoying the highest saving rate across the type of plans available

With so many fixed rate plans being offered in the market, consumers actually need to look no further than Senoko Energy LifePower24 Fixed Rate Plan to get the most bang for their buck. It offers one of the highest cost savings for a fixed price 24-month contract.

Senoko Energy LifePower24 Fixed Rate Plan

Senoko Energy LifePower24 Fixed Rate Plan is a 24-month fixed price contract where consumers pay only 17.78₵/kWh (price includes GST) instead of SP Group’s current regulated tariff of 24.39₵/kWh. This extremely low unit price is fixed for the entire duration of the contract. Furthermore, additional savings are thrown in as well:

$60 bill rebate;

Up to $50 one-time cash rebate for recurring payments made at Senoko Energy’s partner banks;

Up to 5% monthly bill rebate for recurring payments made with OCBC, Standard Chartered or UOB. Find out more about their bank partners here.

With such a low unit rate fixed across the duration of the entire contract, coupled with the excellent freebies thrown in, this makes Senoko Energy LifePower24 Fixed Rate Plan one of the lowest cost 24 months fixed rate plan in the market.

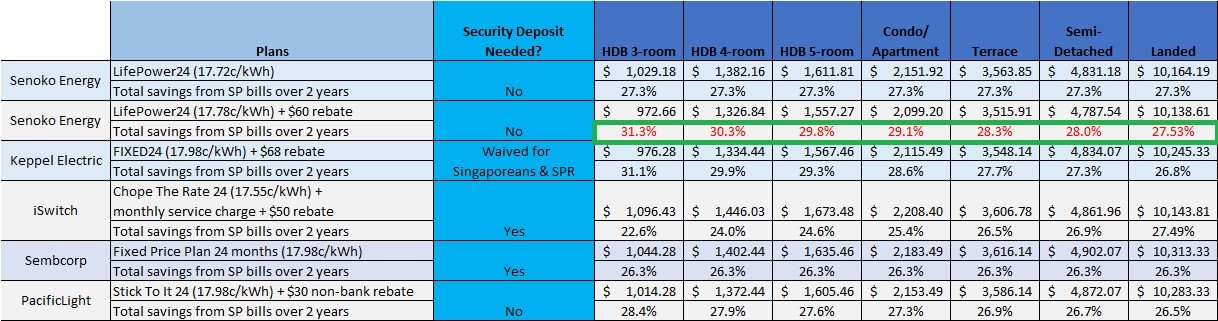

Highest savings amongst OEM Retailers for HDB 3/4/5 rooms, Condos and Landed properties

To illustrate why Senoko Energy LifePower24 Fixed Rate Plan is the lowest in town, let’s make a comparison across OEM retailers offering 24-month fixed rate plans based on SP’s average household electrical consumption.

Click on image to enlarge

Rates above are accurate as of 22nd May 2019.

Comparison are based on 24-month fixed rate plans with bill rebates factored, applied on national consumption patterns by dwelling types. Bank rebates are not yet included.

As seen in the above table, a comparable household staying in a 4-room HDB will enjoy 30.3% savings in electrical bills by switching from SP Group to Senoko Energy LifePower24 Fixed Rate Plan. The most important conclusion is that whether you are staying in a HDB 3-room or a condo apartment or even a landed house, Senoko Energy LifePower24 offers the highest savings rate amongst the OEM retailers compared. More importantly, Senoko Energy does not collect a security deposit when you make the switch.

Sign Up Now for up to $110 Bill Rebate

To milk the most out of this opportunity, consumers should quickly sign up for this limited-time promotion to enjoy up to $110 rebate. Hurry to lock in both the unit rate of your electricity bill and the greatest possible costs savings available in the market. Give your household the peace of mind and sign up with Senoko Energy LifePower24 Fixed Rate Plan now!

Legal Disclaimer: It is still important to exercise due diligence when choosing your retailer, so be sure to read the fact sheets and fine print.

Every business needs an effective marketing strategy to meet sales objectives. As we are progressing tremendously into the technological world, it is imperative that businesses leverage the digital realm to speak to their target markets in more effective ways. Here are three useful digital marketing tips you should consider as part of your overall sales strategy.

Build an SEO-friendly website

Having an online presence is the basic necessity to thrive in the digital world. With 4.92 million internet users in Singapore at a penetration rate of 84%*, tapping on this medium to market your business is essential. You can first start off with a fully-optimised website that is search engine friendly. While Search Engine Optimisation (SEO) is crucial for search engines to rank your website on the first page, you must also know how to target your audience online using SEO.

Keywords

Before beginning any SEO optimisation strategy, you must know what keywords or phrases you want to rank on search engines. These words or phrases are what your potential customers will key into the search box when they are looking for a product or service that you also offer. There are many ways you can do keyword research. For instance, you can find out what generic words or phrases best describes your brand and also look up those used by your competitors to see where you are lacking in. There are several powerful keyword planning tools you can find online to perform this step.

Do note the type of customers you want to attract. If you are looking to drive sales to your e-commerce site such as Shopify, your potential customers are more likely searching for a product or service with a buying intent and thus, your keywords and phrases should be more product and service-focused. Those seeking information often use different short and long-tail keywords that are topical. While the former appears to be a more direct way to drive sales, the latter is also an important digital marketing strategy to tap on as it can persuade potential customers to visit your website to learn more about your brand before making a conversion.

On-page SEO

Once you have decided on your keywords and phrases, it is time to work on your on-page SEO. These include updating your metadata by giving descriptive page titles and unique meta descriptions for each web page. Your URLs must also be easy to read, and your site must be accompanied by a clean web structure that is easy to navigate.

Images play a big role in search engine optimisation too. You can boost image SEO by updating your alt texts, image descriptions and titles with relevant keywords that relate to the nature of the image, the text it is accompanied by and the webpage it is displayed on.

Content

One other crucial element of on-page SEO that is significant in digital marketing includes optimising your website content that can drive sales. While it is necessary to include keywords in your optimised content, you must remember that your content is not only meant to convert prospects but also serves as a resource for others to share. This means that you can reach new audiences that will increase your website traffic and thus increase the chance for you to convert a lead to a customer. There are different types of content you can include – blogs, videos, guest posts, product reviews and guides, among others.

Establish a powerful social media presence

Once you have a well-optimised website, you can now take advantage of social media to further enhance your online presence and be a level higher in your digital marketing sales strategy. There are 4.6 million active social media users in Singapore, with 4.2 million accessing the application via their mobile phones. Apart from creating paid advertisements on these platforms, you can create engaging organic content that your customers want to read, and drive engagement through likes, comments and shares. This allows you to generate positive brand mentions when your followers consistently interact with your brand in ways that meet your objectives. It is also an excellent opportunity to incorporate weblinks into posts and encourage your followers to click on them to reach your site.

All in all, boosting your products and services on social media not only helps to increase traffic to your website (that could potentially lead to conversions), but it also helps to build a base of loyal brand followers who are willing to share your content and thus increase your audience reach.

More prospects, more opportunities for a conversion!

Attractive Google My Business Profile

If you are running a business with a single store or several franchises across the country, setting up your Google My Business (GMB) profile will be incredibly helpful. An important SEO ranking signal, GMB allows you to manage your presence on Google Maps where you can provide all relevant details of your business such as the address, opening hours, telephone number and email, reviews as well as a link back to your website. Moreover, you can also give prospective customers an idea of what your business looks like by incorporating a 360 virtual tour. This allows them to have fun while interacting with your content and be prompted to find out more about your business by navigating to your website through your GMB profile. This drives organic visitors to your site who have the potential to generate conversions.

There is never a direct way to drive sales when it comes to digital marketing. Often, customers may not be as receptive to promotional content and thus it is useful to find other meaningful ways to engage them before they are more confident to make the purchase.