Let me start by saying that you must not spend more than what you can afford. Remember that credit is a loan, which is meant to be repaid. It is your responsibility to stay on top of your debts and to keep your commitment with the lenders. Maintain your control by avoiding the credit limit of your cards.

DO CHECK YOUR CREDIT HISTORY

Reality check! Credit cards with premier rewards and terms fall down to candidates with the best credit. This is why it is important to see your financial circumstance in the eyes of an issuer. Consider getting a credit report, before availing a credit card. Keep your eyes peeled to some errors!

Image Credits: pixabay.com

DO NOT PICK AN UNSPECIFIC CARD

Much like a box of chocolates, credit cards exist to embody different functions. Some are used for travel miles and others are used for shopping rebates. You must figure out which credit card suits you best! Compare credit card options from different issuers, before making a grand decision.

DO KEEP UP WITH YOUR STATEMENTS

To reap the benefits of your credit cards, you must fully pay for your statement each month. Not paying the full amount entails acquiring interest. The interest that you will be paying for will just cancel out any benefits that you are meant to receive. Moreover, paying off your statement each months ensures that you stay out of debt too.

DO NOT GIVE YOUR CREDIT CARD INFORMATION AWAY

As much as you trust a partner or a friend, you must not give your credit card information to someone else. It may entice this person to use it against the law. Say that you lent your credit card to a co-worker. While some cashiers do not check NRIC these days, you will never know when someone will ask for it. You would not want to be entangled with a “fraudulent” scene.

Image Credits: pixabay.com

DO MEMORIZE THE ISSUER’S HOTLINE

A credit card offers an additional layer of protection than a debit card. Debit cards only offer the pin numbers as protection. You see, credit card companies often have a department that follows up on reports of fraudulent charges. Things will be taken cared of, if you quickly report a stolen credit card. Thus, you must know the no-cost hotline of your credit card issuer.

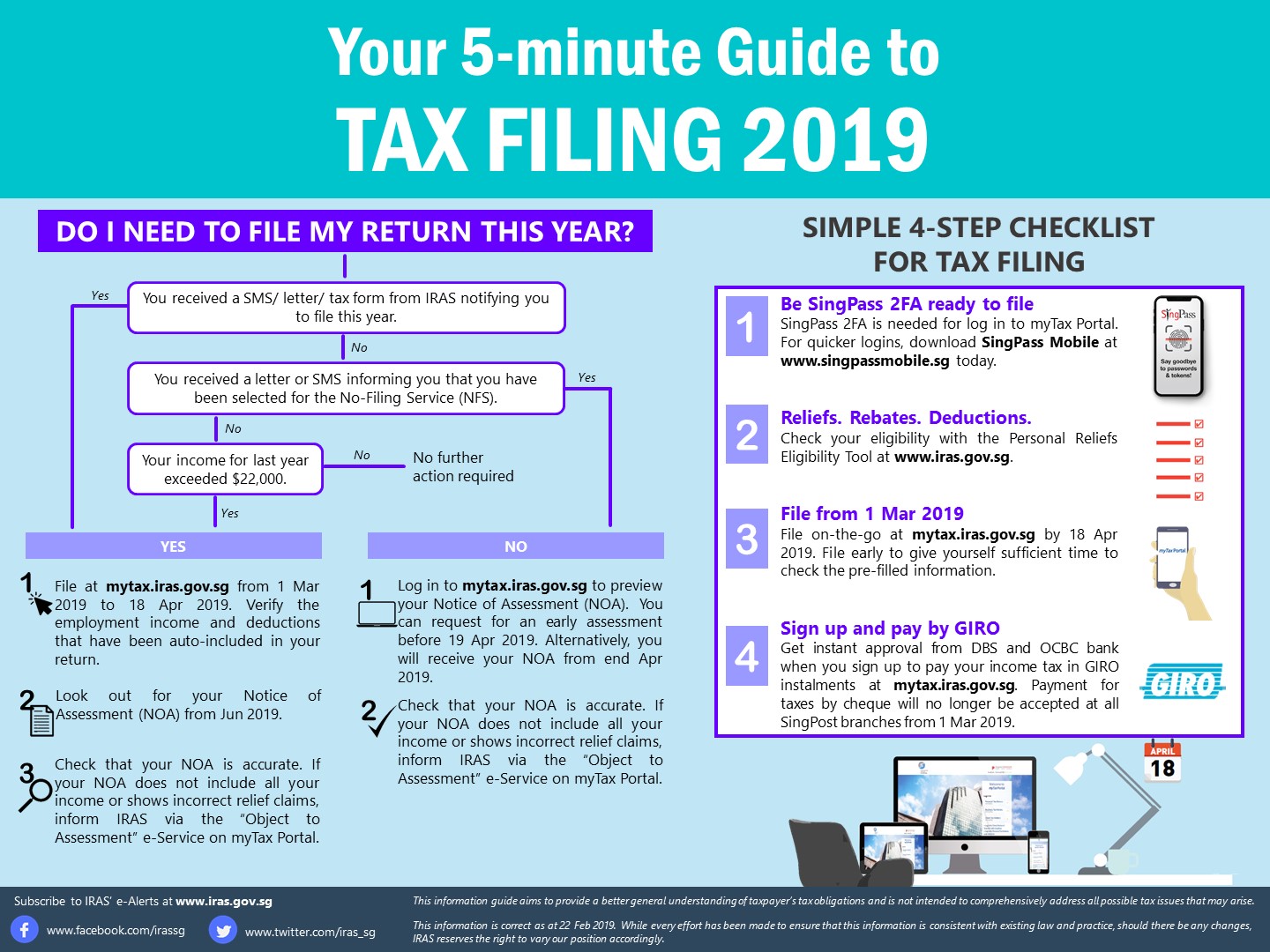

Lower your tax bill by maximising the tax reliefs available to you, and pick up some tax filing tips for a smooth tax season.

Tax season 2019 has begun, and like most Singaporeans, you may once again be required to file your taxes this year. From filing your taxes to utilising the tax reliefs at hand, here’s a quick way to a breezy tax season.

5 minutes: Find out if you are required to file your taxes this year

To file your taxes or preview your Notice of Assessment, log in to https://mytax.iras.gov.sg using your SingPass.

10 minutes: Edit your tax return and claim the tax reliefs available to you

Your income information may have already been pre-filled in your tax return if your employer is under the Auto-Inclusion Scheme. This means that your employer submits your income information to IRAS on behalf of you. However, if you received additional income in 2018 or spot an error in your tax return, hit ’Yes, I need to edit my Tax Form’ to ensure that these are reflected in your return.

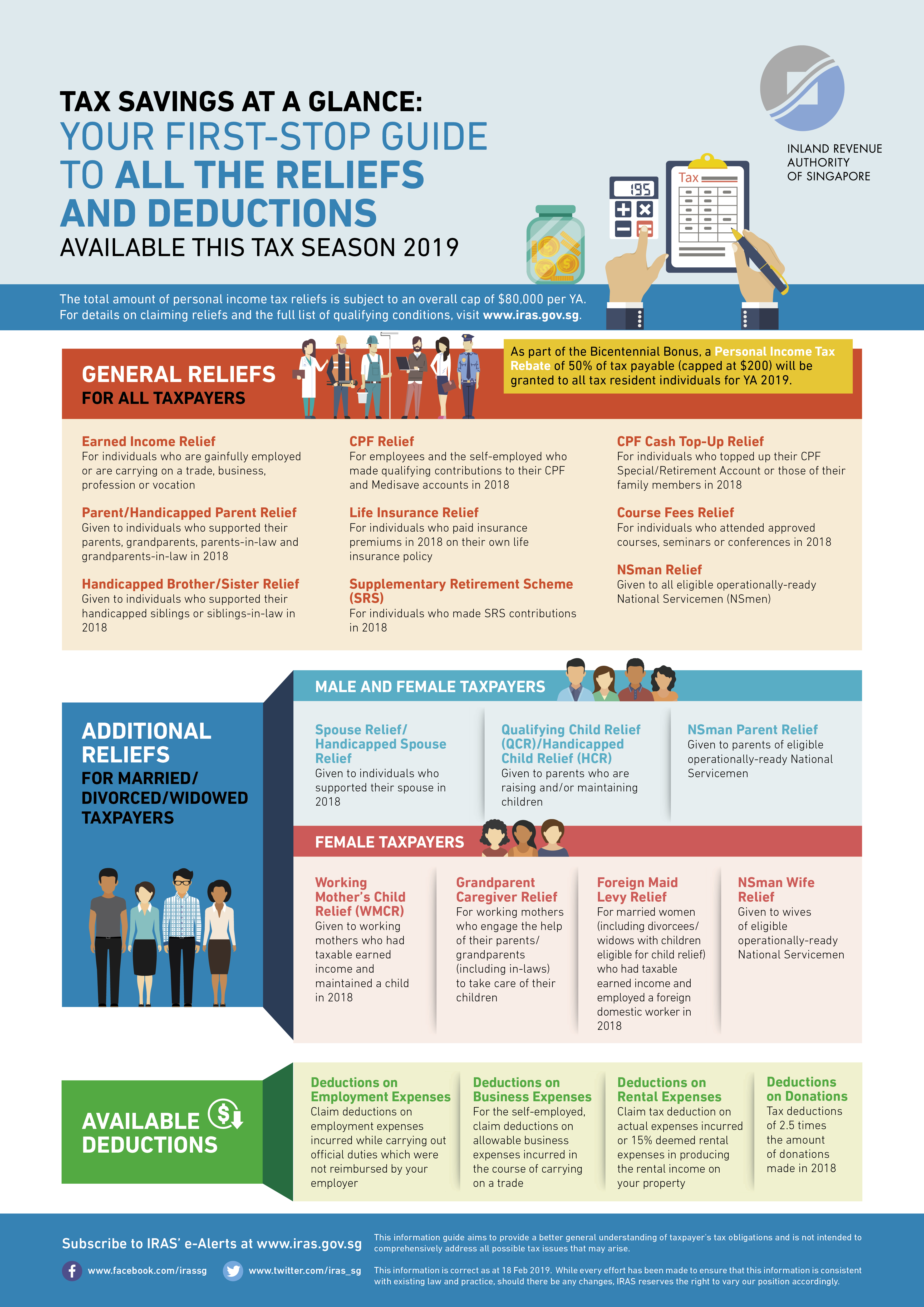

Tax reliefs and deductions are targeted at certain groups of people to encourage social and economic objectives, such as filial piety and the advancement of skills. If you are eligible for any of the tax reliefs below, be sure to make your claims for them in your tax return for a lower tax bill!

When you’re ready, hit Submit before logging out. An acknowledgment message will be displayed upon successful submission of your tax return. Your tax bill will be sent to you between end Apr and Sep 2019. In the meantime, sign up for GIRO if you have yet to for a hassle-free tax payment experience.

Remember, file your taxes at myTax Portal by 18 Apr 2019 to avoid the last-minute rush and late filing penalties.

Aside from its undeniable cleanliness and thriving economy, foreign investors see Singapore as a country with an attractive corporate and personal tax rates. The Singapore taxing system is widely known for its tax relief measures, absence of capital gains tax, one-tier tax system, and extensive double tax treaties. What keeps this system going?

To answer that question, we must dive in to different types of taxes.

INDIVIDUAL INCOME TAX

As the name suggests, the individual income tax is imposed on a person following his or her total income. The extent to which a person pays for depends on one’s status in Singapore. At the time of assessment, the government may consider you as a taxpaying resident or a taxpaying non-resident. For residents, the tax rates begin at 0% and are capped at 22% (above S$320,000). For non-residents, the flat rate is 15% to 22%.

CORPORATE TAX

The corporate tax is imposed on a company following its profit or net income. Net income refers to the difference between the total expenses, receipts, and additional reductions in the book value of an asset. You have to understand that a company will only be taxed if the income is generated from Singapore or generated from overseas and received in Singapore.

What’s more? The corporate tax operates on a one-tier system and caps at 17%. By keeping corporate tax rates competitive, the country continues to attract a significant share of foreign investment.

PROPERTY TAX

It comes as no surprise that all property owners in Singapore are subject to Property Tax. It is imposed on property owners based on the expected rental values of their properties. It is levied on the unmovable properties such as buildings and lands. It is pretty much clear cut from here.

GOODS AND SERVICE TAX

Last but not the least is the type of task that we tackle on a daily basis – the Goods and Service Tax (GST). It is an indirect tax levied on the price of goods and services in the country.

GST was introduced in 1994 at a rate of 3%. Years have passed and the rate has been steady at 7%. Imported goods sold in Singapore follow the same GST rate too!

Image Credits: pixabay.com

Use these information to enrich your savvy consumer skills! ?

Whether you are doing business online or you have a physical store, payment security is a must for you. Credit card payment is one of the popular ways for customers to pay for the goods or services that they are availing.

It is essential to your business to make sure that the credit card payment you are taking is free of fraud. Consumers who are victims of fraud purchases can file chargebacks through their credit card companies, leaving you on the losing end, especially if you have already shipped the goods.

On the other hand, you have to secure your payment system as well, so the cardholder’s information will not fall on the hands of cyber thieves.

Here are some credit card safety tips for you to minimize business’ losses:

1. Verify the issuing card company

If you are taking payments over the phone and you are unsure of the issuing card company, try a BIN lookup. Just enter the first 6-8 digits of the card number, and it will tell you the issuing card company.

Knowing the issuing card company will help you if there is a need for you to report a suspected fraud. Do not even think twice in calling the issuing bank. Fraudulent transactions will do you no good. It may look like money, but it will be reversed anyway.

2. Take advantage of an Address Verification System (AVS)

Credit card companies and issuing banks cooperate with merchants to check whether the submitted billing address by the customer matches with the address on their end. Major card companies such as Visa, MasterCard, American Express and Discover Card support AVS.

If you are using a payment processor, talk to them on how to integrate and implement AVS on your payment processing.

Briefly, though, this is how AVS works:

When you make the AV request, the first 4 to 5 digits on the street address and the zip code will be checked against the address on file at the bank. For instance: 1238 Main Street, Main USA 98763. What will be checked are “1238” and “98763.”

There will be six return codes for the check namely: full match, partial match address, partial match zip code, no match, international, and unavailable. You will receive one of these codes.

A full match is ideal as it comes with less risk. If the shipping address matches with the address on file at their issuing bank, then it is harder for the customer to dispute the transaction.

Maintain a secure network

Invest in high-grade encryption especially that you are processing payments. In doing this, you are not only protecting your business but also your customers’ information.

Apart from encryption, there are other ways to secure your network:

Install anti-malware software especially those that can run in the background.

Update your tools regularly so weak spots will be fixed.

Utilize layered security measures like using strong passwords and two-factor authentication.

Always be watchful of the different fraudulent schemes of these con artists.

Be PCI Security Compliant

The Payment Card Industry has set some guidelines on how to secure cardholders’ information. You can read the details of these guidelines on the PCI Security Standard Council’s website.

Take some time to read the guidelines so you can implement the security measures recommended. These measures suggested will keep the acceptance and transmission of cardholders’ information safe. Being compliant to these is one of the best ways to combat credit card fraud.

5. Be critical of customers’ purchasing behavior

As it is essential to secure your payment system technically, it is equally important for you to be vigilant on customers’ behavior.

These are few things to be watchful of on your customers:

Multiple items in an order especially if it doesn’t make sense.

Multiple orders on the same day.

Orders coming from countries you unusually get orders from.

Big items such as tv’s or laptops.

You can require additional identity verification for unusual purchases. Customers will appreciate your effort as you explain to them the purpose of what you’re doing. After all, it is for their own safety, too.

Maintaining the safety of credit card payments and making sure that you are taking payments from the legitimate cardholders will not only ensure that your business is profit-wise, it will also safeguard your reputation.

As an entrepreneur, you cannot afford to lose some profit to con artists and tarnish the reputation you are working hard to build. Carefully examine your current payment system and make the necessary changes if needed.

Hard assets, such as art, antiques & collectibles, as a form of investment alternative?

Well, perhaps these could be the following reasons.

Assets of such, often retain their value as inflation rises, and they can also provide balance to other asset classes that suffer more from rising costs.

Collectibles include everything from high-priced antiques, gems, works of art and many others.

1) What makes collectibles valuable?

Some collectibles are valuable because they are creations born of talent, skill and workmanship.

For instance, Chinese Porcelains. Each item is inherently unique, and its value may be specific to that individual item. These types of collectibles tend to hold their value over time, generally keeping pace with inflation. Many also have the potential to appreciate in value. The value of these types of collectibles depends on many factors as well. The age of the item, rarity, craftmanship and its current popularity among collectors may all be factors in determining its value.

2) Why invest in Antiques & Collectibles?

Some but not all, increases in value, though they tend to appreciate slowly over a number of years. Another attributing factor, “The new high will always be higher”, which is why we oftenly see these items setting new records high with auction houses around the world. Collectibles, however, can act as a hedge against inflation too. This is why many investors are sometimes tempted to add them to their portfolios.

3) Upsides

As an investment, There are a number of unique upsides which you cannot replicate with anything else.

Tangible assets:

Collectibles are not influenced by inflation or interest rate headwinds.

Low-correlation to the stock market:

Collectible markets rarely move in tandem with the economy.

Growing rarity:

It is all about supply and demand.

And over time, A good piece of work, become scarce when that particular item is no longer trading in an open market.

Personal control:

You hold on to the assets; you don’t have to worry about anything like an investment bank run, or being scrutinized into a virtual world with no physical ability to control and manage. And If you’re one lucky collector with ability to capitalize on arbitrage situations, you’re against all odds.