It is highly likely that infections of Zika virus will continue to elevate in Asia, according to the recent statement given by the reputable World Health Organization. This statement encourages heightened awareness as 70 countries were already affected. Zika virus has been endemic in Thailand, Malaysia, and Singapore. In our country alone, there have been over 400 reported cases this year.

For those of you who are not familiar with this illness, let me enlighten you! The first case of the Zika virus was reported in the 50s. It is transmitted by the Aedes mosquito (much like dengue). What is unique about it is that only 1 in 5 infections are symptomatic. That is alright because Zika is generally mild and self-limiting. However, it is dangerous for pregnant women due to the congenital Zika syndrome. Rare cases showed that some individuals developed serious neurological complications. This can potentially harm an unborn child. Unfortunately, there are no vaccines or anti-viral drugs to treat this illness.

Due to this alarming outbreak, many Singaporeans were quick to purchase protective measures such as mosquito repellents and insecticides. Further protection led for some people to pursue insurance policies. To their favor, more and more insurance companies are now offering extensions for Zika virus. These extensions are under personal accident or travel policies.

Among the five insurance companies that offer Zika coverage, NTUC Income came first. NTUC Income’s Personal Accident Assurance policy included Zika virus in the optional infectious disease coverage back in April. Ms. Annie Chua, the VP for personal lines at NTUC Income, once said: “This could be extended to other products with infectious disease cover.”

Great Eastern allows its previous and new Personal Accident policyholders to claim up to S$300 for medical expenses and S$30,000 in the event of death due to the virus. A pregnant woman who has been diagnosed with the illness is entitled to twice the amount of medical reimbursement. Furthermore, Great Eastern will pay a total of S$3,000 if the baby is born with an abnormally small head or with a Zika-related microcephaly.

Other insurance companies that provide Zika coverage are Prudential Singapore, Sompo Insurance Singapore, and AIA Singapore.

Mosquitos that cause Zika and dengue breed around homes in small amounts of clean water. This is why it is important to dispose waste in flower pots, discarded tyres, and other vessels that may accumulate water. Watch this short video to learn more about the efficient preventive measures:

Singapore’s public and private hospitals offer some of the world’s most exceptional healthcare services. The only drawback is the rising healthcare costs of about 8-9% each year. Other countries are embracing this upward trend due to the global inflation.

The question now is: “How will you save for future healthcare costs?”

CREATE A SEPARATE SAVINGS ACCOUNT

If you have a trusted financial advisor in your network, discuss about the feasibility of opening a separate savings account for your healthcare costs. You may choose to categorize this under your emergency fund for fuss-free budgeting. Otherwise, you will have to adjust your budget to accomplish this.

EVALUATE YOUR OPTIONS

Whether we are purchasing a plane ticket or a small furniture, we are constantly on the hunt for the good deals. However, we can easily spend thousands of dollars on medical costs without comparing the hospital prices. Avoid sinking in a pile of debt by not jumping into the first offer.

For instance, you have a substantial amount of time to evaluate your options for an elective surgery. Maximize your time by shopping around.

Image Credits: pixabay.com

PREVENTION IS BETTER THAN CURE

A surefire way to manage overwhelming healthcare expenses is to prevent them from happening. Your road to wellness starts today! Make healthier choices by eliminating your unhealthy vices including your indulgence on junk food. Afterwards, commit to eating a balanced diet and to cultivating an active lifestyle.

COMPARE THE INSURANCE POLICIES

Get the best health insurance that your money can afford! Frame your current situation and compare the insurance coverages that will suit your medical needs. For instance, some insurance policies cover long-term care. This only make sense if you plan to retain the policy throughout your retirement years.

Perform a quick cost-benefit analysis by check it out Singapore’s first health insurance comparison website: gobear.com.sg. It provides basic information such as the premium amount per month as well as the maximum payout per year.

FAMILIARIZE YOURSELF ABOUT MEDISHIELD LIFE

Central Provident Fund administers a health insurance plan called MediShield Life. It aids in paying out huge hospital bills and certain outpatient treatments such as dialysis and chemotherapy. MediShield Life’s coverage is ideally for Class B2/C wards at public hospitals.

You may choose to stay in a Class A ward or a private hospital, but the payout will only make up a small proportion of your bill. You will have to fork out cash or pay from your Medisave.

No one is entirely certain about what the future holds. Preparing now can help you manage the financial pain of later years!

Some Singaporeans have gone off the idea of travel insurance. While it used to be considered an absolute necessity, more travellers now think of it as an unnecessary waste of S$50 to S$100.

This is particularly true of those who go on short trips, to whom travel insurance becomes a significant expense. But are they doing the right thing?

Why No Travel Insurance?

The most common reasons are:

They have personal accident insurance

They feel the claims process is unrealistic and restrictive

The seek cost-efficiency

They are already covered by credit card

They are covered under their employer’s insurance

They Have Personal Accident Insurance

For some travellers, their main concern is their healthcare related. They do not want to face medical expenses if they suffer from a fall, get hit by a car, etc.

They are less concerned about the other things that travel insurance covers. These are things like lost jewellery (they may not be carrying anything valuable), flight delays (not an issue if they have airline memberships that already compensate them), or tour agency issues (they may not be on a package tour).

For those travelling to countries where they have friends or family, some of the emergency assistance from travel insurance may be irrelevant. For example, if you are travelling to stay with your uncle in Canada for a few days, it may not be a big deal if your luggage is diverted for a day or two. The inconvenience may not be worth a S$100 insurance policy.

(It might be a different story if you are travelling alone, and know nobody where you’re going).

These travellers typically add personal accident coverage to their existing insurance policies, in the form of a rider. This can give them comprehensive protection wherever they are, for a fairly low cost (e.g. under S$30 a month).

If they are going skiing, for example, they may be happy to rely on their personal accident coverage, without adding travel insurance.

They Don’t Want to Go Through the Claims Process

Some seasoned travellers are intimately aware of travel insurance terms, and are dissatisfied with them.

For example, many policies do not allow you to make claims for lost jewellery. For lost cash, the maximum claimable amount might be too small to be relevant (e.g. The maximum claimable amount is S$250 regardless of how much you lose, and then insurance policy alone is already over S$100).

There are often tight limits on maximum claim amounts, on a per item basis. Even if the policy insures you for you to S$1 million, for example, the maximum claimable amount on your broken iPad may only be S$500.

Some travellers also feel the claims process is unrealistic, or too convoluted. For example, you may be required to present original receipts if you want to make a claim for your broken laptop.

With regard to trip cancellations, some policies only pay out only under specific conditions. For example, a policy may not pay out if the cause of the cancelled trip is the Singapore haze or a strike (the trip may only be insured against poor weather).

As such, a subset of travellers believe travel insurance has too many restrictions to be useful. If you want to join their ranks though, you will have to be sure that you make up for lack of travel insurance with the right safety precautions, and the right personal insurance policies.

They Seek Cost-Efficiency

As a rule of thumb, it is not cost-effective to insure expenses you can pay out of pocket.

For example, it would not make sense to pay premiums to insure your socks, or to insure cheap canned food in your kitchen pantry – the odds of losing them are so low, and the cost of replacement so cheap, that the premiums would just be a waste of money.

The same theory can be expanded to things like second-hand laptops, cheap watches, old clothes in your bag, etc. Some travellers would feel no significant pain from losing these items, and prefer to have more cash on hand for shopping or better accommodations. Should they lose the items, they have more than sufficient money to replace them immediately.

(Note: if your worry is losing your luggage and having no clothes, toiletries, etc., you should note that most airlines provide supplies or funds for passengers whose luggage they lose).

Their Credit Card Offers Free Travel Insurance

Many air miles credit cards, such as the Citi PremierMiles Visa Card, come with complimentary travel insurance if you charge your travel tickets to it. The Citi PremierMiles Visa Card covers up to S$1,000,000 in case of death or permanent disablement from accident in a common carrier, up to S$40,000 for medical expenses during a trip, and travel inconvenience.

If you are satisfied with these, there’s no need to buy more travel insurance.

They are Covered by Their Employer’s Insurance

Many people overlook this, so make sure you don’t.

If you are flying abroad for business, check with Human Resources on whether you are covered under your employer’s insurance. If there already is one, you do not need to buy your own.

Some companies have generous corporate insurance plans, that will cover you even if you are not on official business. If so, all you need to do is familiarise yourself with the terms (and get private only if you are unsatisfied).

Insurance is a safeguard against unfortunate and unforeseen events. It is a strategic way to manage various risks. Insurance companies offer individuals or policyholders protection from potential losses in exchange of payments called premiums.

To manage your policy letters better, insurance companies offered their own apps. It sounds like a great idea for people who possess a couple of policies from different insurance companies. However, it is quite a chore for people who hold several policy documents. That is when PolicyPal comes in.

Ms. Valenzia Yap is the brainchild behind PolicyPal. About two years ago, Valenzia’s mother was diagnosed with a serious illness. Her mother was diagnosed with one of the most notorious illnesses across the globe – CANCER. The unfortunate turn of events did not stop there. She was surprisingly rejected by the insurance company because of several lapses that they were not aware of.

The inconvenience that she went through while sorting out her mother’s policy letters gave her an idea to digitize the collation of the insurance policies and other documents. So, Valenzia collaborated with two programmers named Rick Wong and Jun Wei Ng to create the PolicyPal. Necessity was truly the mother of invention this time around.

ITS CURRENT SITUATION

This impressive app received over a thousand of users since its launch. Majority of these users are either on their late 20s or early 30s. Interestingly, their policies range from 1 to 12. These information simply shows how a significant number of Singaporeans are conscious about their health and safety choices.

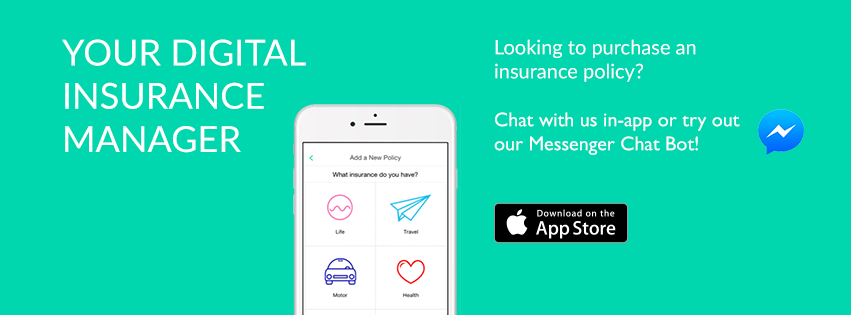

THE EASY PROCESS

In simpler terms, PolicyPal follows these steps:

1. Capture an image of your policy’s first page.

2. Taking a snap of the second page is only necessary if you have riders.

3. Wait for the app to process your data. It will analyze the policy number, premiums, coverage, and expiration dates.

4. View your premiums and coverage in a graphical overview or a comprehensive chart.

5. Request for a review.

6. Get a free portfolio review to understand your coverage its gaps.

7. Purchase from the available policies if necessary.

Image Credits: facebook.com/hipolicypal

Eager to get your very own PolicyPal app, visit policypal.co to download it for FREE!

MORE FINTECH APPS

There are other incredible financial technology startups that originated from the Lion City aside from PolicyPal. These startups came up with smartphone apps that make financial services more efficient, convenient, and prompt. They challenge the traditional businesses that are less reliant on the potency of software.

Do yourself a favor and know more about the Call Levels (i.e., providing live updates for traders and investors), the TradeHero (i.e., gamifies trading), and the Dragon Wealth app (i.e., one-stop shop for financial advisors)!

When you hear the term “Critical Illness Insurance”, what comes to your mind?

If you are envisioning a coverage which offers a payout when the policyholder is diagnosed with a critical illness (e.g., stroke or cancer) then, you are correct!

Critical Illness Insurance or Dread Disease Policy is a lump sum payout given in the event that the policyholder is diagnosed with one of the specific illnesses covered by the policy. It can either be sold as a stand-alone policy or a part of a main policy in life insurance or investment insurance. The guidelines and definitions of the 37 critical illnesses are predetermined by the Life Insurance Association of Singapore. This definitions are fixed across the board.

Unlike other forms of health insurance, the benefits of Critical Illness Insurance is paid out in lump sum so that the person can use it not only for medical expenses but also for other living expenses that can result from the ongoing treatment.

COMMON FEATURES

Here are some of the usual features of the Critical Illness Insurance:

1. Its premium is adjusted based on the policyholder’s age-band.

2. The policyholder is allowed to claim no more than one of the critical illnesses listed.

3. There are no restrictions on the utilization of the benefit payment.

4. The critical illness rider will be terminated once you give up the basic policy.

5. A type of health insurance (with a critical illness rider) has an expiration once the policyholder reaches a maximum age.

6. To reduce the risk of moral hazard, there is a limit on the total amount that you can purchase.

7. Upon purchasing the Critical Illness Insurance, there is a waiting period before you can make a claim.

POSSIBLE ISSUES

Given the fixed definitions of the critical illnesses as well as the common features of the Critical Illness Insurance, there are several issues that can possibly happen in different situations. For starters, the benefits can only be paid if the disease EXACTLY meets the standard definition stated by the policy.

For example: Coma is defined as…

“A coma that persists for at least 96 hours. This diagnosis must be supported by evidence of all of the following:

• No response to external stimuli for at least 96 hours; • Life support measures are necessary to sustain life; and • Brain damage resulting in permanent neurological deficit which must be assessed at least 30 days after the onset of the coma.

Coma resulting directly from alcohol or drug abuse is excluded.”

In reference to the definition above, say your beloved spouse had been in a state of coma for the past 48 hours due to substance abuse and you cannot do anything about it because he is not qualified to claim the insurance payout. It will be difficult for you to fork some money at a relatively short notice.

Another issue that can happen is when two or more diseases transpire (co-morbid diseases) and you can only claim for one of it.

Image Credits: pixabay.com

Furthermore, claiming of the benefits usually has a waiting period. If a critical illness is carried out during the waiting period then, you cannot be paid for its benefits.