For frequent jetsetters, nothing feels more indulgent than stepping away from the crowded terminal and into the calm of an airport lounge. More than a waiting area, it is a sanctuary where you can settle into a plush seat, sip a complimentary drink, enjoy a hot meal, and even catch up on work without the usual airport frenzy.

This experience is no longer reserved for business class tickets or elite frequent flyers. With the right credit card, you can unlock a global network of lounges that quietly elevate your travel routine.

Image Credits: unsplash.com

At the top of the scale sits the American Express Platinum Card, often regarded as the gold standard for those who value both breadth and luxury. Cardholders earn 0.69 miles per S$1.60 spent locally and enjoy unlimited worldwide lounge access. The exclusivity comes at a steep cost with an annual fee of S$1,744, but for those who fly often, the comfort and convenience often outweigh the price.

For travelers seeking balance between cost and perks, the Citi PremierMiles Card has long been a crowd favorite. It offers 1.2 miles per local dollar and 2.2 miles per overseas dollar, along with two complimentary Priority Pass lounge visits per year at more than 1,300 airports. The annual fee of S$196.20 makes it a practical choice for those who may not travel every month but still want comfort when they do.

The DBS Altitude Visa Signature Card delivers strong value, especially for those who maximize overseas spending. Cardholders earn 1.3 miles per local dollar and up to five miles per overseas dollar, paired with two complimentary Priority Pass lounge visits each year. With an annual fee of S$196.20, it is a solid option for travelers who want their everyday spending to translate into meaningful travel rewards.

At the entry level, the Standard Chartered Journey Credit Card with an annual fee paying version extends a taste of premium travel. It earns 1.2 miles per local dollar and two miles per overseas dollar, plus two Priority Pass lounge visits annually. The annual fee of S$196.20 makes it an approachable choice for younger professionals or occasional travelers who want to enjoy the benefits of lounge access without overcommitting.

Image Credits: unsplash.com

In the end, the value of free lounge access depends on how often you fly and how much you prize comfort before takeoff. For some, unlimited entry is worth every dollar of the fee. For others, a couple of complimentary visits each year provide the right balance. What is clear is that modern credit cards are reshaping the way we travel, making airport lounges less of an exclusive privilege and more of a practical perk.

Singaporean households are taking on more debt than before, yet the broader financial landscape tells a reassuring story. Household balance sheet numbers from the recent Singapore Department of Statistics (SingStat) release showed that liabilities grew for the sixth consecutive quarter, rising 5.2% in the first quarter of 2025 compared with the same period a year ago and reaching $384.1 billion. This marks the sixth consecutive quarter of rising debt, driven mainly by increased borrowing for property purchases and other major expenses.

But don’t mistake rising debt for financial distress. For many Singaporeans, taking on long-term loans to finance big-ticket items such as homes is a sensible strategy, especially when balanced with careful cash management for everyday costs. In a city where the cost of living never sleeps, spreading payments over time helps families better manage their cash flow.

Image Credits: unsplash.com

Meanwhile, household financial assets have grown even faster, increasing by around 7.5% compared with a year ago to an estimated S$670.1 billion. This means that the liquid assets Singaporeans hold, including cash and bank deposits, comfortably cover their debts. With assets outpacing liabilities, overall household net worth remains healthy, climbing 8.1% in the first quarter compared to a year earlier, reaching $3.1 trillion. This marks a slight slowdown from the previous quarter’s 8.5% growth, but the momentum is unmistakable.

Image Credits: unsplash.com

Experts point out that housing loans continue to dominate household debt portfolios. Mortgage loans now represent more than 70% of total liabilities. Yet, resilient property values have provided a sturdy cushion, shielding households from overexposure and bolstering their net worth.

In essence, borrowing when paired with strong asset growth and responsible repayment can be a sign of financial strength rather than vulnerability.

I’ve been on the lookout for a credit card with the best rewards and after some research, I stumbled on this combo:

UOB Lady’s Credit Card x UOB Lady’s Savings Account

I’m excited to make the most out of my savings and spending, knowing that signing up for both can earn me up to an impressive 25X UNI$ per S$5 spent, equivalent to 10 miles per S$1!

How It Works for Me:

UOB Lady’s Credit Card: I earn 10X UNI$ per S$5 spent on up to two of my preferred rewards category(ies). That’s 4 miles for every S$1 I spend.

UOB Lady’s Savings Account: I boost my rewards with up to an additional 15X UNI$ per S$5 spent on my preferred rewards category(ies), adding up to 6 more miles per S$1.

Plus, there’s no lock-in period, giving me the flexibility to choose and change my preferred rewards category(ies) every quarter.

And the best part? There’s no minimum spend required, allowing me to earn rewards on my terms!

Painting the Picture:

I have plans to maintain a S$50,000 Monthly Average Balance (MAB) in my UOB Lady’s Savings Account and spend S$800 each month on my preferred rewards category(ies) with my UOB Lady’s Credit Card.

For me, a monthly S$800 spend is easily attainable since I spend the bulk on the Beauty & Wellness and Dining categories.

Here’s the rough breakdown if you’re interested:

Gym membership ($100)

Beauty/cosmetic buys ($100)

Personal grooming such as hairdressing, facial treatment/hair removal, nails/lash/eyebrows, etc. ($300)

Dining at my favourite restaurant and ordering food via foodpanda ($300)

This means in just one month, I could rack up 3,200 UNI$.

Keeping this up for 12 months means I could gather a whopping 38,400 UNI$ in a year!

Redeeming My Rewards:

I can convert these UNI$ into 76,800 KrisFlyer miles (1 UNI$ = 2 miles).

With that, I could snag my round-trip business class ticket to Hong Kong* within a year! It would be my first-ever business class experience.

But if I decide not to spend all my UNI$ on flying, I have plenty of other options too.

I can redeem my UNI$ for rewards from a variety of dining, shopping, and travel merchants on UOB Rewards+.

In essence, whether I’m aiming for luxury travel or indulging in simple everyday perks, the benefits add up quickly!

*Based on Singapore Airline’s Saver Awards Chart as of October 2023, excluding taxes, charges, and fees.

Maximizing Your Rewards:

You can choose and change your preferred rewards category(ies) every quarter. These include:

Dining

Travel

Fashion

Beauty & Wellness

Family

Transport

Entertainment

This flexibility means you can adapt as your spending habits and priorities shift.

Switch to whatever categories you deem fit quarterly to maximize your UNI$ and get the best rewards for your spending and savings!

For example, during the year-end holiday season, I can switch my rewards category to Travel. This allows me to book air tickets and easily hit the S$800 spending target in a single transaction!

By consistently managing my spending, I can easily accumulate a significant amount of UNI$ annually. During travel months, I can reach the monthly spending target even faster by booking air tickets and covering other travel expenses.

If you have more savings to park aside and can maintain at least a S$100,000 MAB, you can earn an additional 15X Lady’s Savings Bonus UNI$ on your preferred rewards category(ies).

So, it’s smart to consolidate your purchases with the Lady’s Credit Card to maximize your Lady’s Savings Bonus UNI$.

Curious About Your Rewards?

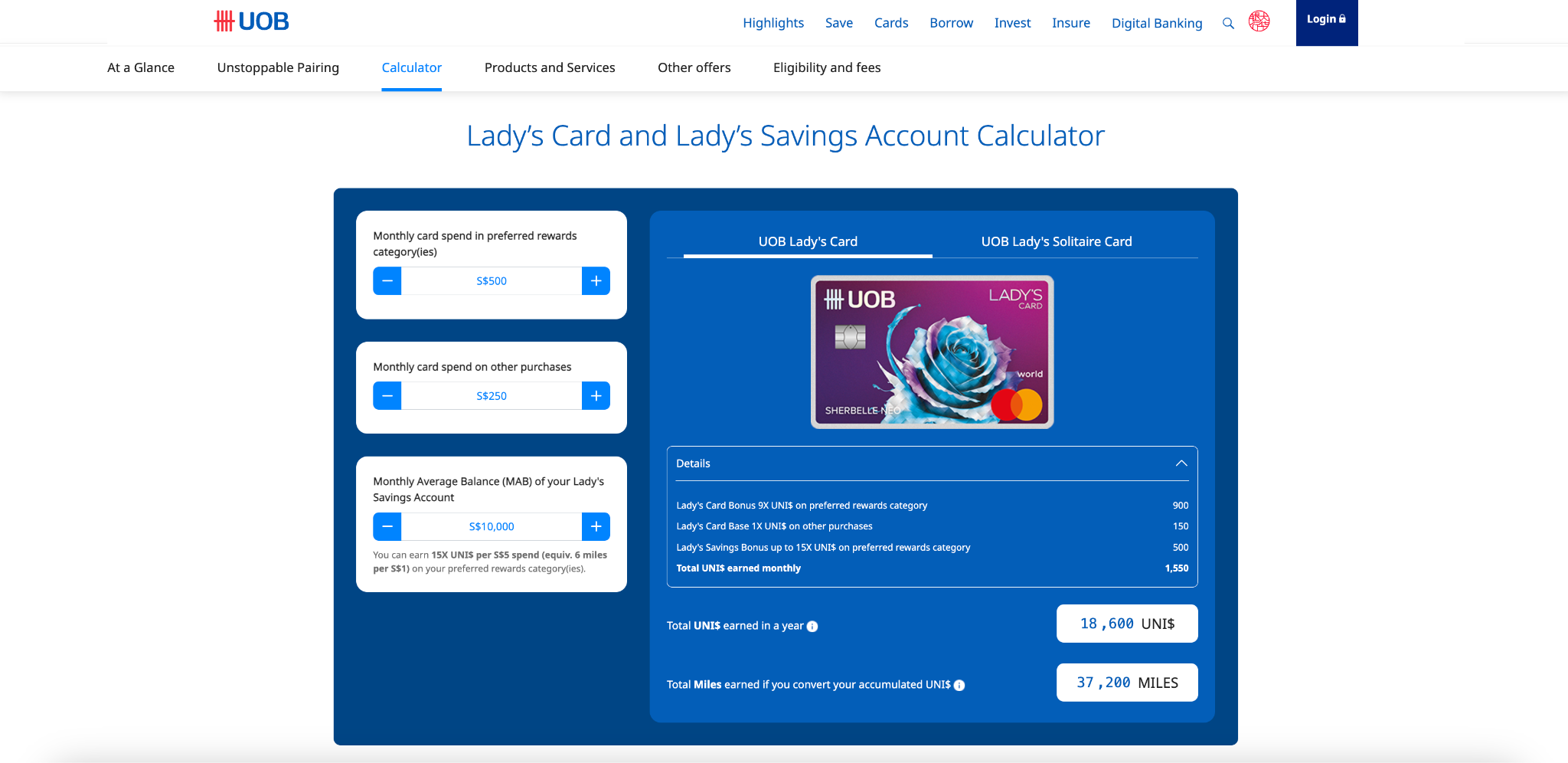

Wondering how many UNI$ and miles YOU can rack up based on YOUR spending and savings?

Simply click this link to UOB’s official website and click on ‘Calculator’ to access the ‘Lady’s Card and Lady’s Savings Account Calculator’ to enter your details and see your potential rewards in a flash!

Just like this:

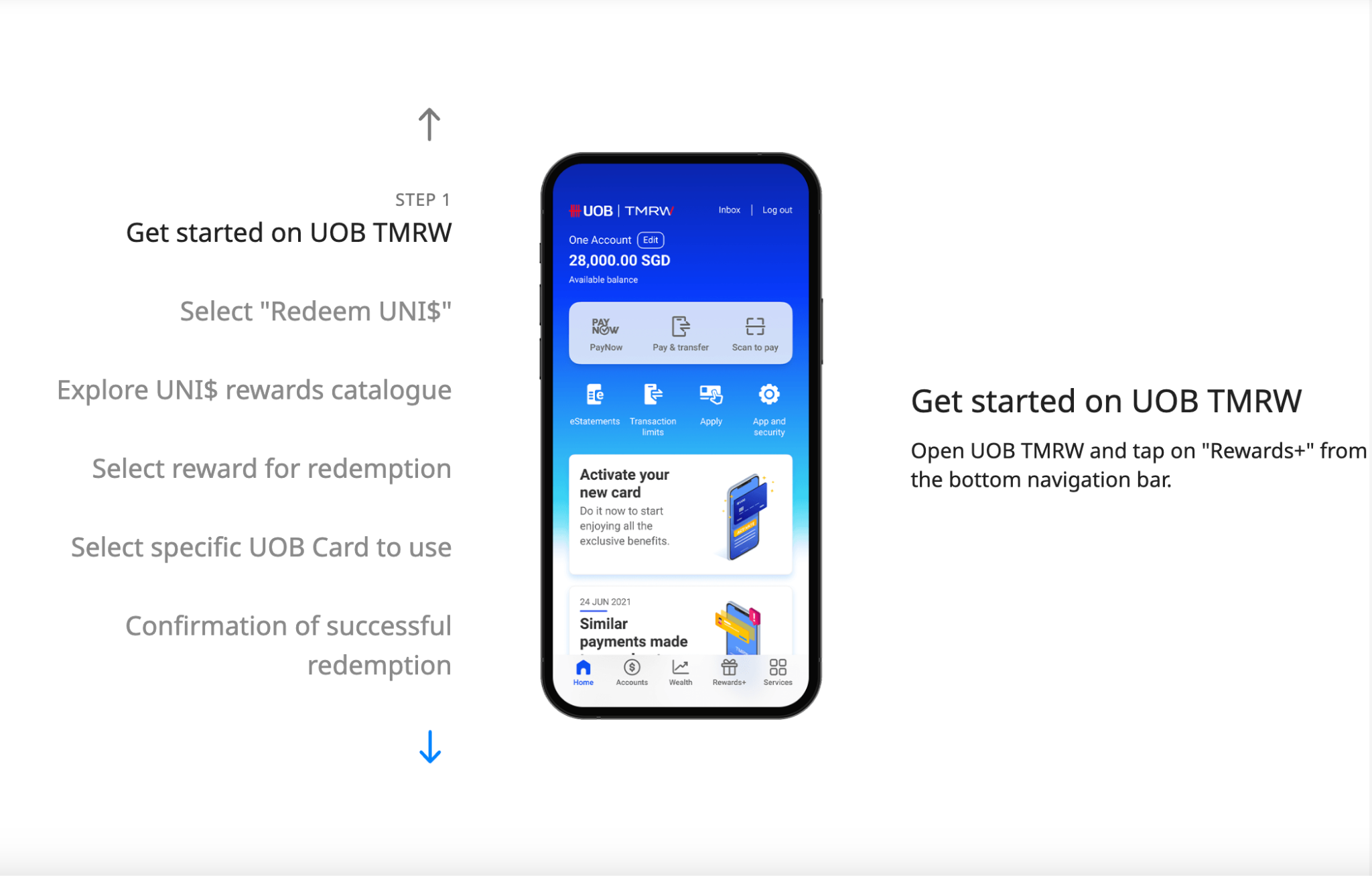

Subsequently, as a card member, you can easily view, track and redeem your UNI$ rewards all on the UOB TMRW app.

0% LuxePay Interest-Free Payment Plan over 6 or 12 months on your luxury purchase (shoes or bags)

Exclusive Birthday Treats during your birthday month

e-Commerce Protection for your online purchases

Complimentary Travel Insurance covering up to 100,000 USD

Receive a S$250 Sephora Gift Card when you spend a min. of S$6,000 on your UOB Lady’s Credit Card. Limited to the first 280 eligible cardmembers.

For the UOB Lady’s Savings Account:

Receive a Bespoke Puffy Bag with Rose Leather Charm worth S$98 by reBynd, an eco-conscious brand by Bynd Artisan, when you apply for the account online and deposits S$5,000 new funds into the account. Limited to the first 150 customers in each calendar month from 8 March to 30 April 2025 only.

That’s not all. UOB is also rewarding ALL customers who hold both the UOB Lady’s Credit Card and UOB Lady’s Savings Account as of 30 Apr 2025 with a lucky draw chance to win an Éclat KNOT Alone® Double Pave Bangle worth S$520 or Gentle Monster sunglasses worth S$490.

T&Cs apply, of course. Insured up to S$100k by SDIC.

So stop waiting and join me right away by signing up now here.

Discover how to use loans strategically for personal and business growth. Learn about payday loans, SME loans, and financial planning tips for a secure future.

While this may sound ordinary, loans for managing money can be more than a safety net. They can be stepping stones toward big dreams. Whether you’re looking to expand your small business, cover emergency expenses, or invest in yourself, using loans strategically can make all the difference.

Here’s a practical guide that will help you navigate financial planning with loans without getting overwhelmed.

Why Loans Are More Than Just Borrowing

Loans are mostly misconceived as a last resort for people in financial turmoil. But the fact? Loans are a powerful financial tool whenever used wisely.

Think of them as your partners in your financial journey. They are there to help you seize opportunities, solve problems, and pave the way for growth. The key lies in knowing how and when to make use of it.

1. Borrow to Invest in Yourself

Sometimes, the best investment you can make is in yourself. Be it funding a professional course, earning a certification, or pursuing a degree, using loans for education or development of skills will yield benefits over a long period of time. This kind of investment not only increases your earning potential but also makes you more competitive on the job market.

Payday loans can be a godsend to bridge quick funding to cover immediate-term expenses in pursuit of your goals.

2. Loans for Business Expansion

For most small and medium-sized businesses, it is access to capital that makes the difference in scaling up, not just staying operational. A loan for an SME can give your enterprise that boost it needs when creating new talent, making investments in new equipment, or embarking on launching a new product.

It is, therefore, more convenient for you to get your funds through a number of options specifically tailor-made in Singapore for owners of businesses.

Interested in SME loans? Take a look at Capitall to see how they can help you expand your enterprise.

3. Manage Short-Term Needs with Payday Loans

Life has a way of throwing those unexpected expenses into our laps. Be it an unplanned medical bill, urgent repairs in the house, or a travel need cropping up all of a sudden, payday loans can bring quick respite.

These loans are meant for short-term financial gaps; hence, they have shorter approval and repayment periods. Just be sure to borrow only what you can comfortably repay.

4. Consolidate Debt for Better Financial Health

Overwhelmed with a lot of loans or debts? A debt consolidation loan is one that helps you put all of them together into a single, supermanageable payment. This makes budgeting easier and can even lower your overall interest rate to save money in the long run. Consolidating debt is smart when anyone has to juggle high-interest debts.

5. Establish a Good Credit History

One of the best ways to build a strong credit history is by taking loans and repaying them in time. A good credit score opens doors to larger loans with better interest rates in the future. Start small with manageable loans, repay consistently, and watch your financial reputation soar.

6. Plan Big Life Events Without Stress

Great moments in your life, such as marriage, buying a home, or starting a family, usually bear big price tags. Couples handling family-related financial planning may also benefit from a Family Law AI Platform to better manage legal documents and associated costs. In addition, loans can also make such events more manageable, as the cost is divided into smaller portions over a great deal of time. Just be sure to budget well and borrow only what you’re comfortable repaying.

7. Emergency Preparedness

Nobody likes to contemplate emergencies, but one should be prepared for them. Loans act like a financial cushion during contingencies, whether it is a medical emergency or a case of sudden loss of a job. Knowing you have access to quick funding provides peace of mind during challenging times.

8. Understand the Terms of the Loan

Be certain, before signing on the dotted line, that you understand every single condition of your loan. In particular, look for:

Interest Rates: Fixed rates come with fixed, predictable payments, while variable rates can fluctuate.

Repayment Tenure: The shorter the tenure, the bigger the EMI but the lesser the overall cost.

Hidden Fees: Check for any mention of processing fees, late payment fines, or even prepayment penalties.

Take time to understand the details of what is being discussed in order to avoid surprises in the future.

9. Choose the Right Loan for Your Needs

Not all loans are created equal. Here are a few popular options:

Payday Loans: These loans are ideal for urgent short-term expenses.

Personal Loans: Great for major life events or debt consolidation.

Sites such as OMY Singapore allow you to compare loans and choose the one that fits your needs.

10. Know When to Seek Help

If you are confused about taking which loan and how much, never feel shy to go for advice. Financial experts will explain your options for you and plan your financing. Similarly, being a businessman, consulting with a financial expert can keep you correctly utilizing loans for your benefit.

Successfully Managing Loans: Tips

Taking a loan is only half the journey. The other half is taken care of when you see to it that you run it responsibly. Here come some tips:

Create a Repayment Plan: Budget your monthly income to include your loan payments.

Avoid Overborrowing: Only borrow what is truly needed.

Set Reminders: Set up an automatic deduction or calendar reminder so you will never have to worry about missing a due date.

Communicate with lenders: If you’re having trouble making payments, reach out to your lender and talk about options for restructuring or deferring.

Loans as Tools, Not Loads

The golden rule is quite simple: loans are to work for you, not against you. They’re tools to help you get to where you need to go, instead of anchors holding you down from an economic perspective.

Prepare a plan in place for how the funds are going to be utilized effectively, loans can unlock possibilities one never thought available to him or her.

Think Long-Term

While loans can solve immediate problems, they’re also an opportunity to think long-term: scale your business, build your dream home, or set yourself up for a secure financial future. The right loan can help you get there faster.

Conclusion

Loans, if correctly leveraged, can be your best allies in your journey in finance. From payday loans, for emergency needs, to SME loans for a company’s expansion, knowing how to choose and manage a loan is what makes a person financially fit.

Access to exploring choices gets easy with platforms such as OMY Singapore. The bottom line should, therefore, be to borrow thoughtfully, plan profoundly, and use loans on what you want to turn to in the future. Use proper monetary strategies to realize your objectives without compromising your financial strengths to a great extent.

Browsed any online store recently? You’ve probably encountered the enticing “Buy Now, Pay Later” (BNPL) option. With the promise of splitting payments over weeks or months without interest or hefty fees, it seems like a dream come true. For many, it has been. Yet, as it becomes a tool for essentials like groceries, it’s worth pausing to consider: is BNPL as great as it seems?

#1: BUYER’S REMORSE HITS TOO LATE

Remember the days of saving for that dream pair of sneaks, making payments, and only taking them home after they were fully yours? BNPL flips this script. You get your purchase instantly, and with the click of a button, you’re locked into a commitment before common sense kicks in.

If regret creeps in later, BNPL doesn’t care. Essentially, you’ve handed over control of your wallet.

#2: RISKY CONNECTION TO YOUR CARDS

BNPL payments are often tied directly to your debit or credit card. Miss a payment due to insufficient funds? Expect a late fee. Fail to pay off your credit card balance on time? That BNPL purchase suddenly carries a hefty interest charge. What starts as a seemingly free loan could snowball into a mess of late fees and mounting credit card debt.

#3: IMPULSE SPENDING MADE EASY

Saving up for a purchase gives you time to evaluate if it’s truly necessary. BNPL removes that waiting period, nudging you to click buy without hesitation. So, if you’re going to use BNPL, be intentional. A new wardrobe for a job might be justifiable. A shopping spree because it’s interest-free? Not so much.

Image Credits: unsplash.com

#4: HAVING A MINDSET OF “ZERO” INTEREST

While many BNPL services advertise zero-interest payments, not all plans are created equal. Larger purchases, like appliances or electronics, may come with longer terms and interest. Sometimes, the interest rates are even higher than what your credit card might charge.

The trouble? It’s all too easy to click “BNPL” without fully reading the terms. Once the purchase is processed, undoing it can be a challenge.

#5: TRAPPED BY HIDDEN PSYCHOLOGY TRICKS

One of BNPL’s sneakiest pitfalls is how it breaks down costs. A purchase of S$80 might feel like a mere S$20 every fortnight. While this makes items feel more affordable, it also detaches you from the full cost. Couple this with a lack of financial education and relentless advertising, and many see BNPL as a way to manage money. The result? Early reliance on debt and a lifetime habit of paying things off in chunks rather than saving.

Image Credits: unsplash.com

IN A NUTSHELL

Don’t buy it if you cannot afford it. If you’re tempted, ask yourself: Do I truly need this? Can I pay for it outright?

Financial freedom isn’t about splitting payments or juggling debts. It’s about saving and spending within your means. BNPL may be a tool, but it’s not a safety net. In the end, whatever you’re buying will feel far better when they’re truly yours.