For most Singaporean families, buying a condominium is the single largest financial commitment they will make. Getting the structure right — CPF usage, loan quantum, cash reserves, and TDSR positioning — matters enormously before you commit to a unit.

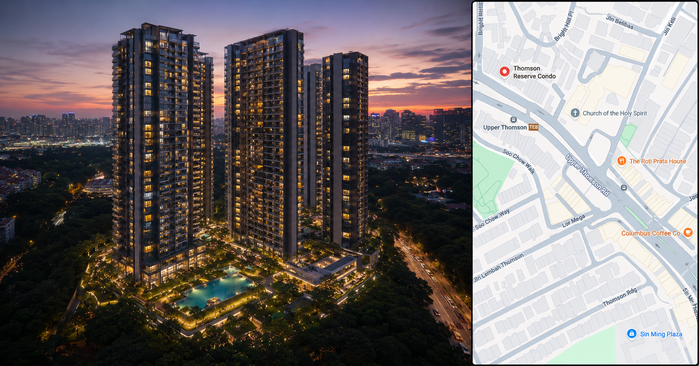

This guide breaks down the real numbers for the most anticipated new launch condo at Upper Thomson — Thomson Reserve at Bright Hill Drive in District 20 — so you can assess whether it fits your financial profile before the showflat opens.

What Does Thomson Reserve Actually Cost?

Official pricing has not been released as of mid-2026, with the showflat preview targeted for later this year. Based on the land acquisition cost of S$1,178 psf per plot ratio and current D20 market benchmarks, analyst estimates place launch pricing in the mid-$2,300s to $2,700 psf range.

In practical quantum terms:

- 1-Bedroom (484 sqft): From approximately $1.19M

- 2-Bedroom (~700 sqft): From approximately $1.55M

- 3-Bedroom (~1,000 sqft): From approximately $2.1M

- 4-Bedroom (~1,300 sqft): From approximately $2.8M

How Much Cash Do You Actually Need?

For a Singapore Citizen buying their first private property with a bank loan, the Loan-to-Value (LTV) limit is 75%. For a $2.1M 3-bedroom unit, the maximum bank loan is $1.575M and the remaining 25% ($525,000) must come from CPF OA funds and/or cash.

Of the 25% downpayment, at least 5% must be in cash (the option fee on booking). The remaining 20% can be CPF OA and cash combined. Assuming $150,000 in CPF OA savings, the minimum cash outlay on a $2.1M unit is approximately $270,000 in cash — before legal fees and BSD.

Buyer’s Stamp Duty: The Often Underestimated Cost

BSD is tiered and frequently underestimated. On a $2.1M purchase:

- First $180,000 at 1% = $1,800

- Next $180,000 at 2% = $3,600

- Next $640,000 at 3% = $19,200

- Remaining $1.1M at 4% = $44,000

Total BSD: approximately $68,600. This must be paid in cash or CPF OA and is separate from your downpayment.

The TDSR Calculation: Know Your Ceiling

Singapore’s Total Debt Servicing Ratio (TDSR) caps monthly debt repayments at 55% of gross monthly income. At a 3.2% stress-test rate over 25 years, a $1.575M loan generates monthly repayments of approximately $7,600. To qualify comfortably, you would need a minimum gross monthly income of approximately $13,800 with no other outstanding debt.

HDB Upgrader Considerations

HDB flat owners can own one HDB flat and one private property simultaneously — but must sell the HDB flat within 6 months of receiving keys to the new condo (after TOP). With Thomson Reserve’s expected TOP in the 2028–2029 range, upgraders have approximately 2–3 years to plan the transition while continuing to service their HDB loan at favourable rates during construction.

Is the Timing Right?

The Upper Thomson corridor has seen consistent PSF growth of 6–10% annually since 2020, supported by the completion of the TEL and increasing demand from families seeking top primary school catchment. Thomson Reserve is the first mega development in this enclave in over a decade — a structural undersupply condition that supports long-term pricing.