There are many benefits to having and using a credit card. From enjoying cashback and discounts to chalking up air miles for your next holiday, the credit savvy are charging everything to their credit card.

When used wisely, it could actually help you save money while letting you enjoy the perks exclusive to the cardholders.

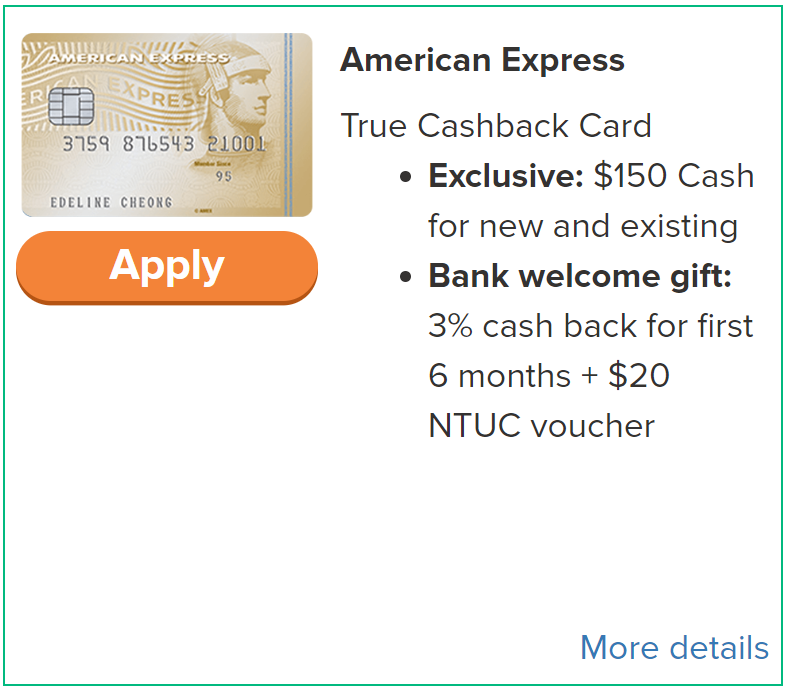

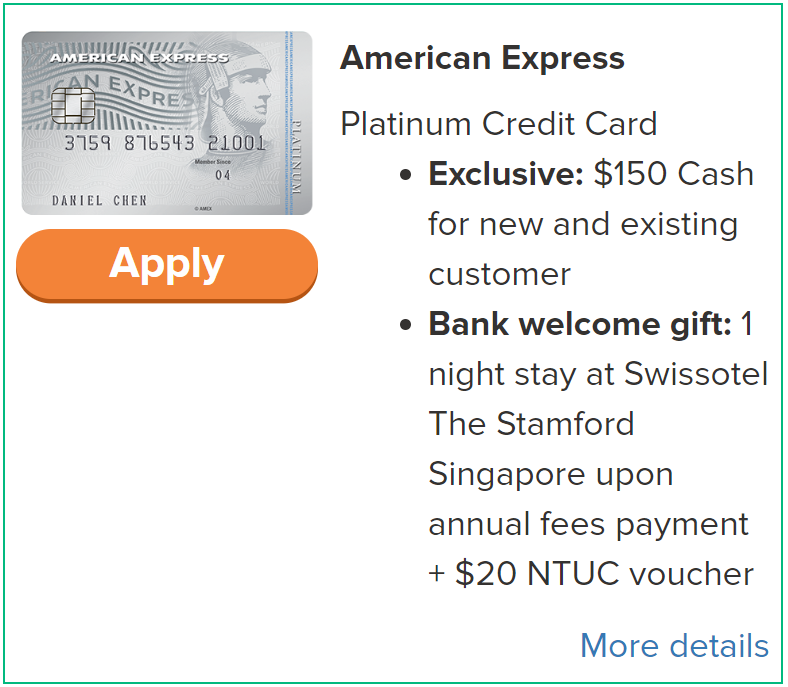

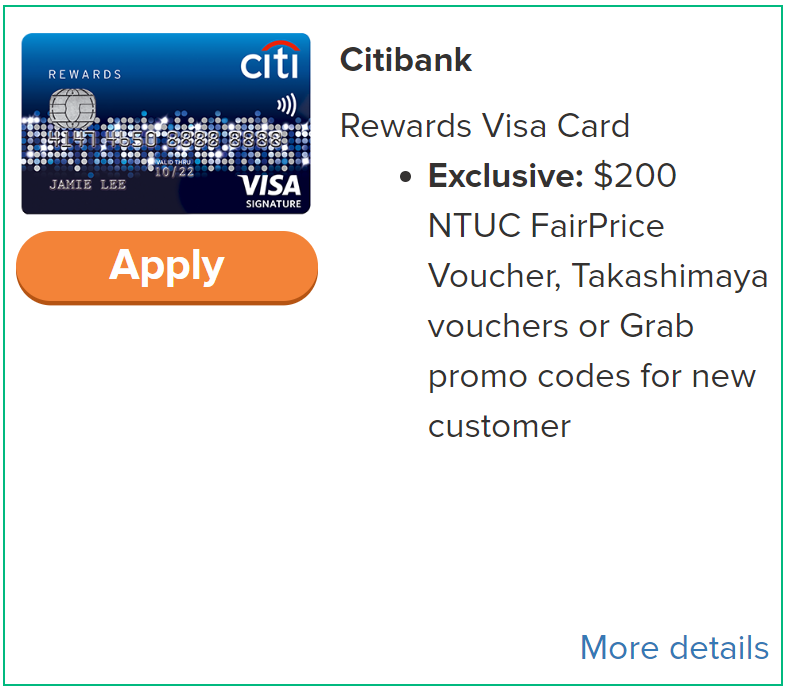

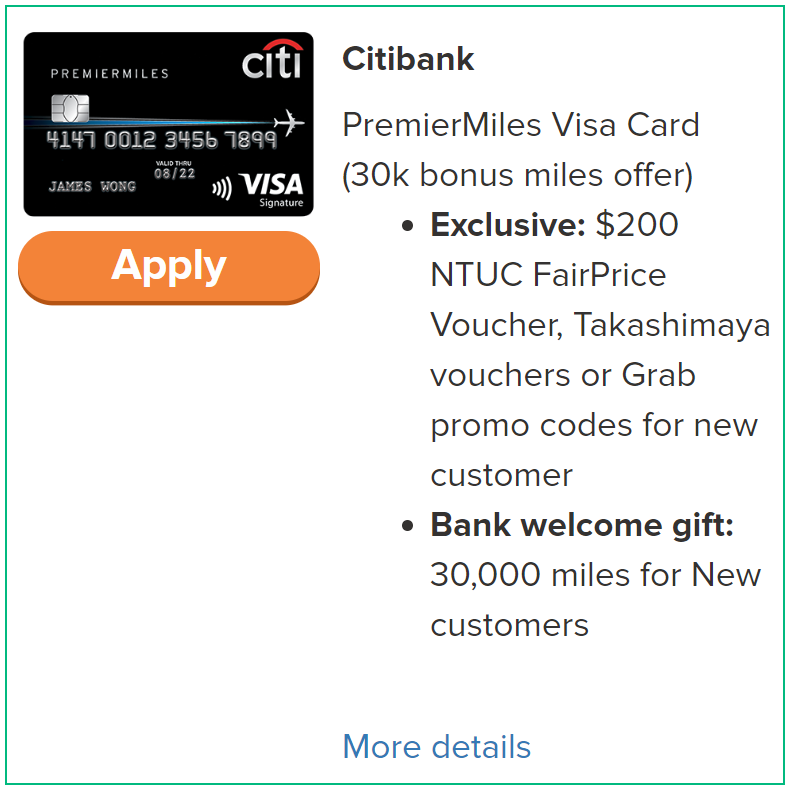

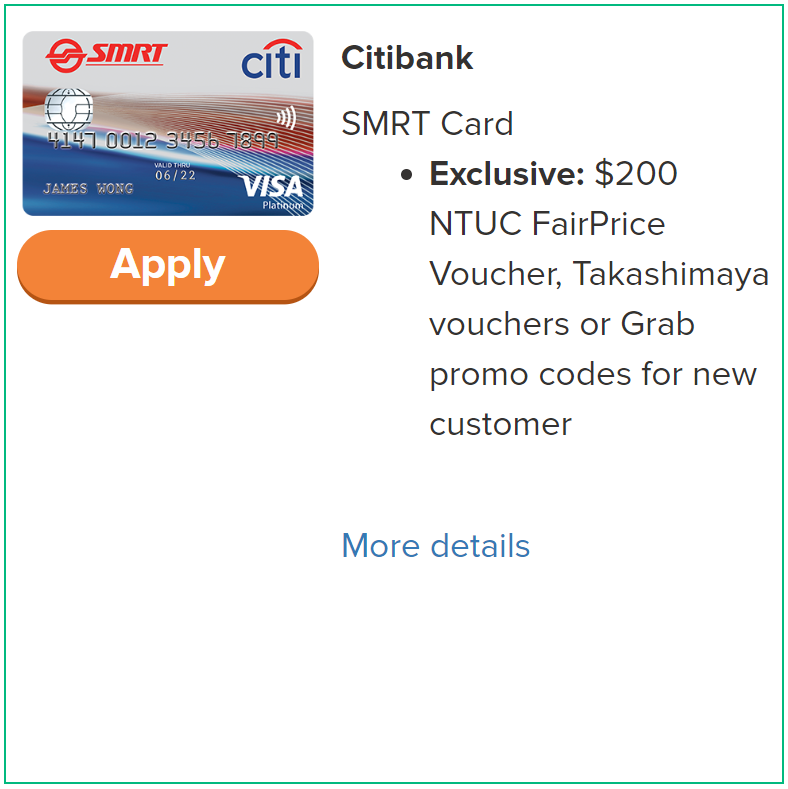

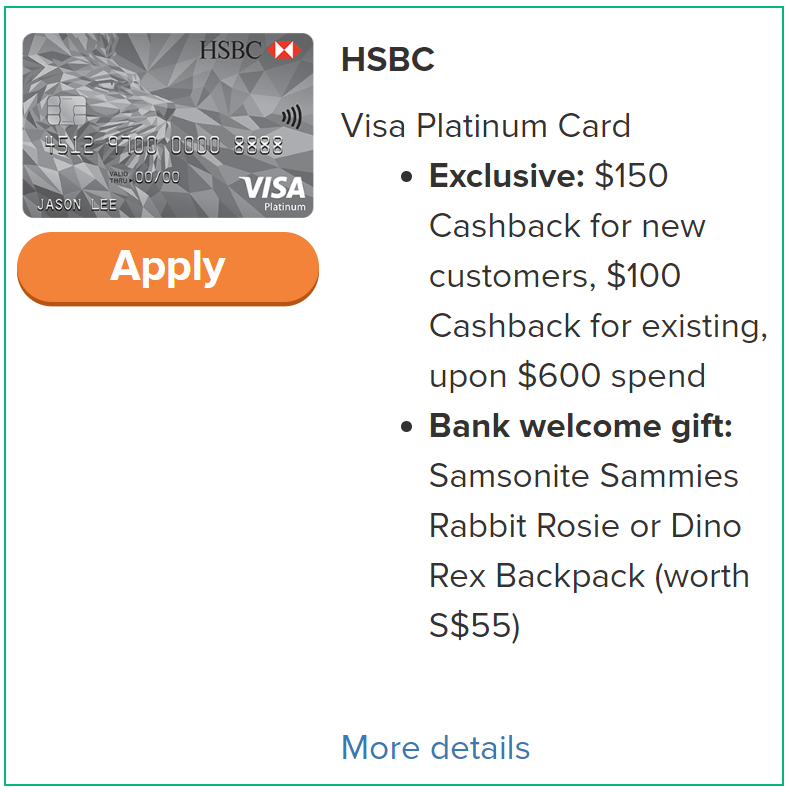

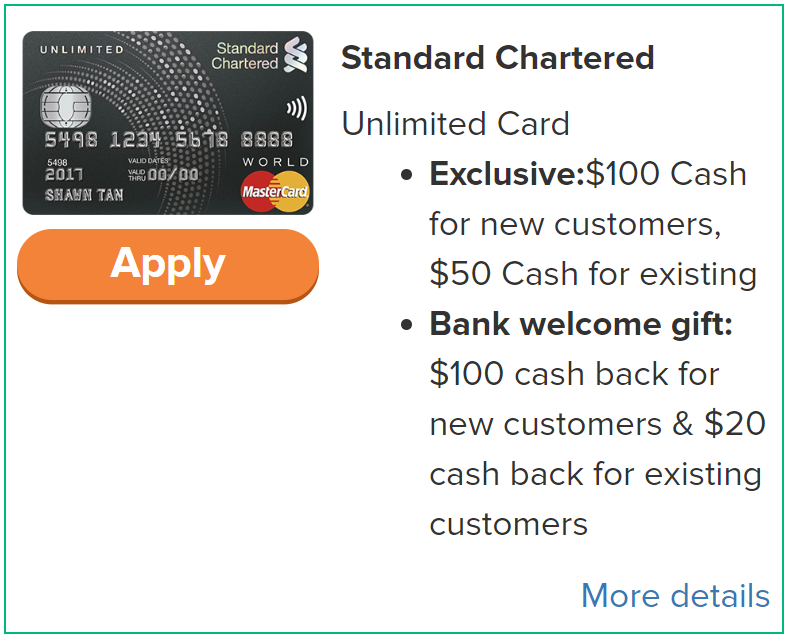

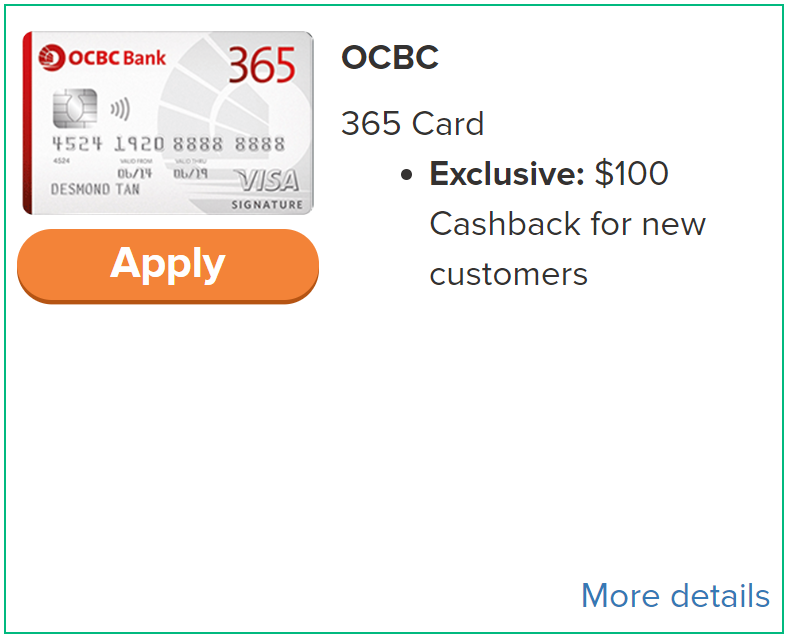

And for a limited time only, receive up to $500 cash, vouchers, cash backs and more when you apply for any of the selected credit cards before 30 November 2018.

What’s better than a Great Singapore Sale? The 11.11 crazy Singles’ Day sales.

If you’re an avid fan of online shopping, you wouldn’t have been spared from the numerous “virtual” billboard signs plastered on your favourite e-commerce shopping platforms, screaming descriptions claiming to offer the biggest and largest deals of the year.

Even if you’re not, you’re not spared either. Virtually every social media platform would have had advertisers interrupt your viewing pleasure with attention-seeking colours to tempt you to shop, shop, shop.

I hate to admit it, but even I have fallen prey to such sales tactics.

Have you accumulated too much credit card charges during the 11.11 sale? Here’s how you can make yourself feel better – choose to repay your credit card outstanding amount with a credit card balance transfer card that has a short-term loan tenure at 0% interest with $0 processing fees.

What is a balance transfer?

Simple logic – the lower the interest rate, the less you have to repay your credit card charges. Balance transfers involve a transfer of funds from a high-interest credit card to a lower-interest card.

This is where the Standard Chartered Credit Card Funds Transfer card comes in.

Exclusive 0.9% processing fee, which can be offset by $220 cash back, for new Standard Chartered cardmembers

Flexible repayment amounts

Comes together with a Standard Chartered Unlimited card

Instead of having to suffer from high interest charges for loan amounts that can be fully repaid in a short period, i.e. 6-12 months, you can now pay them off without these incurring these interest fees and putting an even greater dent on your shopping expenses.

Find out more about the Standard Chartered Credit Card Funds Transfer card on the SingSaver website.

Though created differently, all credit cards have a limit. The credit limit dictates the maximum amount an issuer allows a borrower to spend on a single card. Ideally, your balance should fall below the limit. You see, maximizing your credit card can hinder you from making additional charges.

Employ these tips to ensure that you spend less than your credit card limit.

#1: TRACK YOUR SPENDING

It goes without saying that awareness of your spending habits will help you control your credit card usage. Monitor your billing statements by checking your balance in the bank’s online app or website. Staying on top of your spending will help you foresee any event leading up to going beyond your limit. Thus, you must adjust your expenses accordingly.

#2: CHECK YOUR BALANCE REGULARLY

Before making a purchase, check your available credit balance using your bank’s mobile app. If your credit card issuer does not have an online app, call the bank instead. You can find the contact details at the back of your plastic card.

Image Credits: pixabay.com

Doing so lets you determine whether you should postpone your purchase or to pursue the checkout counter on the spot.

#3: DO NOT INCREASE YOUR LIMIT RIGHT AWAY

Say that you have been constantly spending beyond your credit card limit. You may think that the logical step to take is to ask for a limit raise. However, asking for a limit raise within six months of receiving it can indicate that you are having financial difficulties. Issuers may be less willing to trust you with more credit.

Waiting for bank to automatically increase your credit limit is the best option. This way, you will be able to employ strategies dedicated to spending within your means.

#4: STICK TO THE THIRTY PERCENT

The easiest way to stay within your credit card limit is to provide a cushion. Keeping a cushion of about 30% of your actual credit card limit helps you avoid going overboard. For instance, Mary has a credit card limit of S$5,000. She must not swipe her card after hitting the S$3,500 mark.

Image Credits: pixabay.com

This threshold must apply to all of your credit cards and not just the banks you owe huge money too.

An option used in a hurry might just jeopardize you. You must think down the line twice before applying for your next or first loan. You may just finally end up paying more for this home loan than your original mortgage loan. Therefore, compare and contrast the different interest rates offered by the lending company, look up the advantages and disadvantages and then make your final decision.

The Variable Rate Loan Vs. A Fixed Rate Loan

Are you stuck with a variable rate mortgage and your interest rate is going up day-by-day? Well, home loan refinancing can help you switch over to a fixed interest rate.

A variable loan rate can help you select protective attributes such as lower cap premiums, and cash out from your home collateral.

The Rate Fees and Annual Percentage

This is actually the precondition factor of any kind of home loan plan. Before signing up for any remortgage plan, be very positive about your total forecasted cost savings. In essence, the particular cost of capital the new home loan, in totality, should be less than the financial savings you have as a result of interest rate.

It is possible to reduce your mortgage refinance costs – iSelect by asking for no upfront and at the same time going for lower rates of interest.

The Actual “Safe Margin”

The actual “Safe Margin’ means that you can make your mind up whether you should go for the remortgage option or not. If the particular comparison of the balancing valuation on financial savings against loan refinancing is more than a couple of percentage points slightly higher than the current market rate, then you can certainly go for refinancing mortgage.

At the same time, you have to be able to live in your house for enough period of time and harbor no plan of leaving. Usually, your financial savings will be figured out within 3-7 years, determined by the actual costs at the time you choose to sign up for your home remortgage.

Mortgage Comparison

Comparing your original mortgage and new financial loan needs to be carried out, trying to keep the future in your mind. You need a reasonable thought regarding how long you would like to keep your new mortgage. All things considered, mortgage refinance is a great option on condition that the all-inclusive costs of the current home loan are a bit more than the total cost charged as a result of the new home loan. Which means, your new home loan will allow you to cut costs.

Be Skeptical About Your Pre-Payment Fees and Penalties

You might like to pay the balance of your original home loan early but be familiar with the pre-payment fees and penalties involved in this process. Loan companies are prone to charge penalty costs if you’re thinking about paying off your very first mortgage loan earlier than the specified time period. This takes care of the interest charges, which would have been due in case the mortgage payment had been made through its life.

Admit it! Financial conversations can be awkward, but your relatives can save you in the future. Support them and your relationships with the help of these tips:

PROVIDING A LOAN

One of the most controversial yet clear-cut way to help a family member in need is by providing a loan. The loan is ideally short and straightforward. One must write the terms and conditions that both parties will sign into. This will help ensure a binding financial agreement. Other details that you should clarify include:

a. the total amount of the loan,

b. the installment conditions (e.g., monthly basis),

c. the interest rate calculation,

d. the payment deadlines, and

e. the legal action necessary to cease the payment.

CHIPPING IN AS A GROUP

Tackling a dilemma as a group will maximize your efforts and resources. Say your parents are asking you for an allowance. If your siblings are in a capable position to contribute their funds then, you must ask them. However, you must access whether they have a good relationship with your parents too.

Please involve your partners in the discussions as you do not want to create resentment between siblings and their spouses. If they cannot afford to loan money, they may suggest other ways to help (e.g., accompanying your parents during weekend errands).

EXTENDING AN OFFER

Providing a short-term loan can only last for a specific period of time. On the other hand, offering a means of living can go a long way! Consider hiring or recommending your relative to assist your company’s needs. The job can help him or her to earn money for paying bills or debts.

Image Credits: pixabay.com

Treat your relative like any other employee. Layout the job description as well as the task deadlines. Ensure that you will be able to deal with incomplete or poor quality of work.

GIVING NON-MONETARY ASSISTANCE

Some people may not be comfortable with the act of loaning money without the guarantee of getting payment. If you are unwilling to give cash to a family member, opt for giving non-monetary assistance such as gift certificates or gift cards. This way, you will have more control over what your money will be used for.