Before anything else, we must define two terms: debt and credit. Debt is the amount borrowed by one party (e.g., corporations or individuals) from another (e.g., banks). While Credit is the lawful agreement in which a borrower receives something of value today and agrees to repay later on in the future, usually with interest. Simply, when you use your credit card, you create debt. Debt here is the result from your ability to borrow – from your credit.

Now that you know the definitions and the differences between these two terms, you must discover the pros and cons of using credit as well as the 3 C’s of worthiness. All these are according to the Credit Bureau Singapore. Credit Bureau Singapore was set up in lined with the Monetary Authority of Singapore’s vision to enhance the public’s risk management abilities.

Image Credits: pixabay.com (License: CC0 Public Domain)

PROS AND CONS OF USING CREDIT

The pros and cons of using credit or credit card are plain and straightforward.

Pros

Being able to buy what you need right away

Not having to carry cash

Automatic record of purchases

More convenient than cheques

Cons

Interest especially for items of higher cost

Have additional fees

Financial difficulties may arise

Elevation in impulse purchases may occur

Image Credits: pixabay.com (License: CC0 Public Domain)

3 C’S OF WORTHINESS

Before swimming in a pile of credit, know if you are worthy to take the plunge by asking yourself a set of questions.

1. Character (Are you the type of person who will repay his or her debt?)

Does your credit history show that you are honest and reliable in paying debts?

Do you pay bills on time? Do you have a good credit score/report?

Can you provide a couple of character references?

How long have you been at your present occupation?

How long have you lived at your present home?

2. Capacity (Are you able to repay the debt?)

Is your job income enough to support your credit usage?

Is your job stable and steady?

How much is your salary?

How many loan payments do you have in total?

What are your current debts?

How many people are dependent on you?

3. Capital (Do you have back-up if you cannot repay the debt?)

Do you have a savings account?

Do you have various investments to use as a collateral?

Can you enumerate the properties that you own to help secure loans?

What other valuable assets do you have that could be used to repay debts?

It is essential to know all these to assess whether you are truly fit to apply for a credit card or loan. Furthermore, you may use the information to guide you in your responsibilities as a borrower. 🙂

Many Singaporeans look to their CPF to provide for retirement. As the General Election draws close however, some critics have panned the retirement scheme, saying it no longer suffices. Have a look at some of the realities of the CPF, and decide for yourself:

What is the CPF?

The Central Provident Fund (CPF) is a mandatory savings scheme for Singaporeans. This fund is used to provide for a range of crucial financial needs, such as healthcare, retirement, and home ownership.

Your CPF is automatically deducted from your wages, and your employer is also required to pay a portion into your CPF. Compulsory CPF contributions are as follows:

Age

Your contribution

Your employer’s contribution

Up to 50 years old

20% of monthly income

17% of monthly income

From 51 to 55 years old

19% of monthly income

16% of monthly income

From 56 to 60 years old

13% of monthly income

12% of monthly income

From 61 to 65 years old

7.5% of monthly income

8.5% of monthly income

Above 65

5% of monthly income

7.5% of monthly income

Your CPF is divided into an Ordinary Account (OA), a Special Account (SA), and your Medisave account. The interest rates for these accounts (as of 2015) are:

OA – 3.5% per annum

SA – 5% per annum

Medisave – 5% per annum

You do have the option to invest your CPF money in other schemes, based on an approved list. However, the returns are not guaranteed, and the government will not replace any losses you incur. You can see further details on allowable investments here.

Once you reach the age of 55, you will be able to withdraw all the money except for a required Minimum Sum. The Minimum Sum is placed in a Retirement Account (RA). From the age of 65, savings in your RA are disbursed to you in monthly payouts, which should ideally last till you are 90.

The Minimum Sum (as of 2015) is S$155,000. From the age of 65, this should provide monthly payouts of around S$1,200.

Is the CPF Alone Enough to Retire On?

The answer for most Singaporeans is “yes, but…” Here are some of the factors you need to consider:

Your CPF depletes very quickly when used to pay for your flat

The CPF rate barely keeps pace with inflation

A lot depends on how comfortable you want your retirement to be

1. Your CPF Depletes Very Quickly When Used to Pay for Your Home

Buying a home is one of the ways Singaporeans use their CPF. When you take out a HDB concessionary loan, the entirety of the down payment can come from your CPF*.

(*This does not apply to private bank loans, in which only 15% of the down payment can be made with CPF.)

CPF can also be used to pay for certain fees, such as the legal paperwork for the purchase. Mortgage repayments can be taken from your CPF rather than your bank account.

But this means that, if you use too much of your CPF money purchasing a house, there is a real possibility of it running out.

If you use HDB loans, the interest rate is 0.1% above the prevailing CPF rate (3.6% at present). If you use a private bank loan, the rate fluctuates according to an index, such as SIBOR or SOR. Both options can wipe out your CPF, and leave too little even for the Minimum Sum.

So if you want CPF to provide for your retirement, never overreach and buy a property beyond your means. If you buy the biggest house you can possibly qualify for, be aware that you could be forced to sell it to fund your retirement.

2. The CPF Barely Keeps Pace with Inflation

Singapore’s core inflation hovers at around 3%, which is on par with most developed countries. This means that the general cost of living goes up by 3% with each passing year, and your wealth is being depleted if it can’t grow as fast.

Given the CPF’s return of 3.5% and 5% (for OA and SA respectively), your real returns are only around 0.5% for OA and 2% for SA. This means that relying on CPF alone will provide for a very modest retirement.

Should you have plans after you stop working (e.g. travel the world, look after your grandchildren financially), it may not be a good idea to rely solely on CPF. You should speak to a financial advisor or a wealth manager about different investment products, which can complement your CPF.

3. A Lot Depends on How Comfortable You Want Your Retirement to Be

A pay out of S$1,200 a month is comfortable for some people, but painful for others. We are all used to different standards of living. If you enjoy a high income of S$15,000 a month, for example, switching to S$1,200 a month will be extremely painful.

As such, it is important to work out your desired Income Replacement Rate (IRR). This can be done with holistic financial planning, which also takes into account the amount you will need at retirement, and how long you have to get there (your investment horizon).

Do not believe any arbitrary “rules”, such as sayings that you must have a million dollars to retire in Singapore, or that S$500,000 is enough to quit your job. Such figures are not grounded in your specific needs. Speak to a qualified wealth manager or financial advisor to identify the sum you need.

A Note on Debt

Personal loans range from 6 – 8% per annum, and credit card loans reach around 24%. Your CPF interest rates (or the rates of even the most phenomenal financial products on the market) will never “outgrow” your debt. It is almost impossible.

If you want to retire well, you must pay down your debts early. Be an extreme miser with loans. Make comparisons every time you need money from the bank. You can find the best loans on SingSaver.com.sg.

In Summary:

The CPF is enough to provide the bare basics, when it comes to retirement. However, your retirement will not be lavish if you rely on CPF alone, especially if you are used to a more expensive lifestyle.

Whether you like it or not, along with your marital vows comes the union of your finances. Your partner’s financial habits can either boost or ruin your financial future especially if he or she has a pile of debt. One’s credit history can affect several facets of your life such as loan eligibility, loan rates, and job applications. This is why it is important to openly discuss about your credit history and to plan your future finances together.

Here are some steps you may take…

1. HAVE A TRANSPARENT DISCUSSION

To prevent unforeseen monetary issues, understand each other’s view by explicitly discussing your differences on financial issues. For example, if your partner is a saver then, he or she may view money as an important currency that shall not be wasted.

Then, for honesty’s sake, show a copy of each other’s credit report. Know what your debt and income are actually worth so that you can realistically plan on how to pay for the remaining debt. Your partner’s lack of credit history will reflect on your credit score if you combine accounts.

2. PRACTICE THE ART OF MINDFULNESS

Gone are the days when Mindfulness is practiced solely for meditation. You heard that right! Actively paying attention to the present situation can affect your finances. As you are aware of what is happening in the present, you can make better decisions about money no matter how important it is. For instance, you will keep your credit score healthy because you are aware of the billing schedules. Also, having a present mind will allow you to be vigilant in checking whether the statement breakdown (e.g., phone bill’s data usage) is accurate.

3. LIMIT THE USE OF CREDIT CARD/S

It takes no genius to conclude that overusing your credit card will jumpstart your credit. So, if you cannot say farewell to the plastic card, you might as well limit your usage. As much as possible, keep your usage to a minimum, 25% below your credit limit is a good start. Then, pay off the balance monthly. Examine your progress together as you end the month.

According to the High Court, an individual becomes bankrupt if he or she owes at least S$10,000 and has no means to pay it.

Filing for bankruptcy can be done by the creditor or the debtor. A deposit of S$1,600 to the Official Assignee (OA) is required. The OA is the authority that is responsible for selling as many of your assets as possible to repay your creditors. Credit bureaus will display your bankruptcy date for five years after the date of discharge.

Aside from this, it is essential to note that there are assets that are protected by the creditors such as furniture, HDB flats, compensation awarded for legal actions, and life insurance policies.

The effect of bankruptcy does not only take a toll on your finances but also on other aspects of your life. For instance, there will be restrictions in travelling overseas and in looking for a job especially as a director of a company. Truly, it drastically affects your lifestyle, your career, and your relationships.

This is why it is important to avoid falling to this “black hole” by being financially knowledgable. To put it in perspective, here are 4 Ways To Prevent Bankruptcy…

MANAGE YOUR DEBTS

First, be aware of how much your debts and assets total to. Include every billing statement, every document, loans, and mortgages you may have. Take immediate action when you notice that it is getting hard to pay for your debts.

CUT DOWN YOUR EXPENSES

After seeing the bigger picture, it is time to cut down your expenses. Reduce the unnecessary expenses first such as designer bags or costly coffee beans. Then, add the minimum payments of your debts and the cost of your necessities to your monthly budget.

SELL YOUR STUFF

To aid your budget, you must sell your unnecessary items among others. Selling whatever you can spare can help pay off your multiplying debts.

SEEK HELP

Calculate the money that you need to prevent bankruptcy. Examine how much money you are able to get. Then, consider seeking help from your family and friends to make up for the difference. Yes! Asking your friends and family for money maybe a shady area but this situation is an exception.

If you still find it uncomfortable to seek their help then, consider hiring a professional (e.g., credit counseling agency or debt management firm) to help you reduce your interest rates and penalties at friendly time frame.

Living barely within your income is not a laughing matter. When you are living paycheck to paycheck, you live a life of constant stress, worry, and dread that you might be stuck in an unfortunate debt. It is a struggle to gain control of your money and your commitments. So, here are 3 Simple Tips To Stop Living From Paycheck to Paycheck…

1. CREATE A SYSTEMATIC FINANCIAL OPERATING SYSTEM

In order to cease your worries, a huge turnover can be money flow management. You must give conscious effort to know about where your money flows in and out. Once you have control over your money flow. Then, you will be able to create a systematic financial operating system that consists of: money flow management and budgeting.

Money flow management is accomplished by using a ledger or an app. There are a couple of efficient yet free apps that can help such as: EXPENSIFY, EXPENSE MANAGER, MONEYWISE, POCKET EXPENSE PERSONAL FINANCE, and MINT.

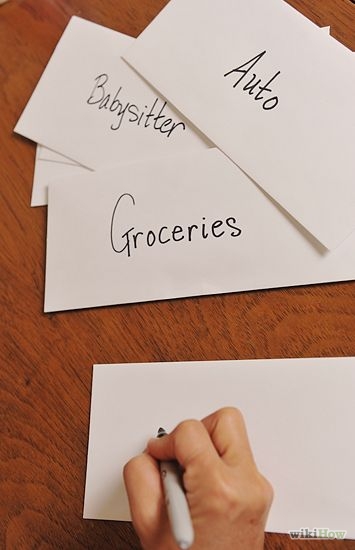

Image Credits: wikihow.com/Do-Envelope-Budgeting

Likewise there are a couple of budgeting such as STATIC or FLEXIBLE budgeting. For personal finances, I highly recommend a simple technique called ENVELOPE budgeting. It starts by storing the cash into separate categories of household expenses that are allocated in separate envelopes.

Budgeting will surely help you gain clarity and control. Start by writing down your monthly income, followed by your monthly expenses, and then subtract the two. Plan and search for a suited technique.

2. PREPARE MONEY FOR YOUR BILLS ACCORDINGLY

Some bills are due frequently while some are semi-annually. Prepare money for your bills accordingly by noting them down. If you have a monthly bill, you may try a trick called half payments. For half payments, you prepare the payment for the bill by subtracting half of the bill’s amount to your bank account per two weeks (bi-weekly).

3. BOOST YOUR EMERGENCY FUND

Prepare for the unforeseen events and financial failures by saving at least 8% of your income per month. You shall call this category your “emergency fund”. It is better to save a certain amount of money than to have nothing save at all.