Quite often the most important thing that you pursue in life is that sound financial situation that you’ve been dreaming for years. You can do so by pulling yourself off from the credit card debt burden. Pulling out of this financial burden isn’t that easy unless you keep following a disciplined and structured approach.

Check out some important steps that can actually help you out of debt:

Evaluate your financial standing

You must know your current financial standing before even attempting to lower your credit card debt. Several experts are of the same opinion when it comes to addressing the core issues pertaining to money management . Once you’re aware of where you’re standing, you’ll certainly be able to hit the target. In doing so, you’ll need to be absolutely honest to yourself. For every card that you possess, you must keep a note of your debt and the interest that you’re required to pay.

Pick a unique payoff strategy.

You may opt for a strategy that suits paying off your credit cards more effectively. You may consider paying off the card bearing the highest APR while meeting the minimum balance with your other cards. For this, you must draw a separate budget from that of your monthly budget. This is certainly a good way of lowering your debt. You’ll find more cash on hand after paying off your first card. Thereafter, you must consider the card with the next highest interest rate for paying off. Similarly, you have to choose cards and pay them off as you go lower down the order of their APR value. On the contrary, you may choose to go the other way round by picking the card with the lowest interest rate first and thus going up the order as you develop the snowball effect. However, you can’t resort to any of the quick cash loans while repaying your cards.

Keep a note of all costs.

Create a list of all of your unavoidable and regular expenses like that of the minimum payments on credit cards, car maintenance, phone bills, insurance policies, cable connection, mortgage besides tracking your expenses pertaining to family trips, entertainment, and dining out. You may develop your budget on this foundation. You may derive a true and fair view of your overall monthly expenses by checking out your bank statements and credit card statements.

Draw your budget.

You might need to cut down on some of your expenses. You’ll need to be realistic in your approach as you ought to bear with a few sacrifices. Cutting out is often not effective as that of cutting back. You may achieve a few big savings when you make a few amends in your domestic budget. However, you must remember that it’s often not easy to opt for an overhaul of your lifestyle. Your budget demands some breathing space so that you may cope with the unforeseen expenses more comfortably.

You may opt out of some services, which in turn helps you in cutting back much sooner than you expect. Segregate your monthly income for meeting a portion of your budget every week.

Monitor your progress.

You must keep a track of your spending just to check if the expenses are dropping or mounting beyond your reach. Keep checking your progress towards an improved financial situation after every alternate month. You can’t see yourself in stress for a much longer duration.

You must have been through a lot while trudging your way through debt. Now, it’s your time to hold on to your patience and work your way out of it. You may check out your financial progress by setting reminders on a sheet a paper. Comparing your progress turns easier as you get it updated with your initial balances.

All is fine and dandy when your life is nicely panned out for you, but as Singaporeans, we can never be too cautious. What if a once-in-a-lifetime opportunity knocks, and you suddenly require a larger-than-expected sum of money to seize this opportunity?

Opportunities can come in different forms in your various stages in life. There may be investment opportunities, a chance to go abroad on an exchange programme, or a chance to further develop your skill sets.

If you find yourself short on cash and need a sum of money to tide you over a short period of time, a personal loan can come in useful.

When we think about loans, most would frown upon it. We would assume that borrowers are incapable of managing their own finances, or that they are financially irresponsible. That is but a misconception, as personal loans are merely tools that can improve our lives if used in a responsible and wise manner.

As compared to home loans, car loans or educational loans which have specific purposes, personal loans are a more flexible type of loan which can be used for almost any purposes you wish. The most straightforward of which are personal instalment loans, where you borrow a lump sum of money from a bank. You can use the borrowed cash for any reason you like. Payment is in fixed monthly payments over a specified time period.

You never know when you might need a loan, but it’s always good to be aware that there is this option out there without breaking the bank. A loan can be useful in the following situations:

A buffer for depleting all your savings – taking a personal loan instead of using up your emergency savings in case of, well, emergencies, and you need the savings

Seizing opportunities with smaller cash outlays – taking a personal loan for immediate cash to enrol in a workshop or class to improve your skill sets and employability, which will result in an eventual higher return

Fulfilling aspirations – perhaps an exchange abroad, a hobby you’ve always wanted to master or even an important bucket list item

Repaying a high-interest loan first – taking a personal loan to pay off higher-interest loans, such as credit card bills

Not all banks and money lenders are created equal. Different financial institutions offer different incentives – some offer lower interest rates while others have lower minimum criteria.

Ultimately, it’s always good to compare loans before applying for one, so you end up with the best bang for your buck for your personal goals and budget – one that has the lowest interest rate, the lowest fees, meets your requirements and has the best welcome offers.

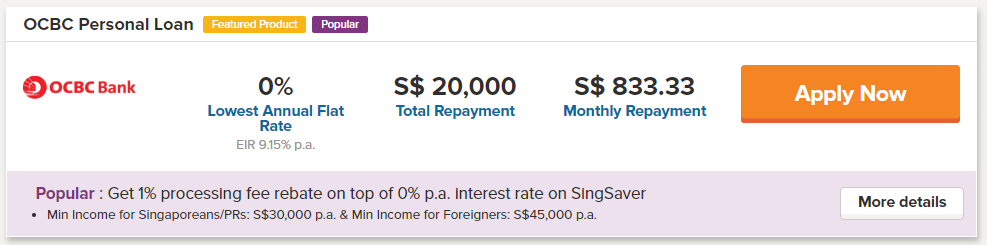

SingSaver offers a convenient platform for comparing between different financial institutions. For a limited time only, get the first 3 months of interest FREE when you apply from SingSaver’s website. That’s not all — SingSaver has also partnered OCBC to offer 0% interest free loan applicable for loan with 2 years tenure.

Not only does choosing the right loan mean meeting your goals earlier, it also means that you can pay off your loans faster.

So while you’re all up for borrowing, be aware of the higher interest rates accounts that you’re liable to paying, so that you clear off those loans first.

Before you purchase your HDB flat, you will be faced with the dilemma of deciding between a HDB loan or a bank mortgage loan. This article demonstrates why it may make sense to choose a bank mortgage loan.

HDB loan is pegged at 0.1% above the interest rate of CPF Ordinary Account. Therefore, the current interest rate on HDB loan is 2.6%. However, you might be able to save on your interest payment if you choose a bank mortgage loan instead. Based on a comparison result from SingSaver, the interest rate on current bank loans varies from 1.62% to 2.28%. Therefore, if you are looking to borrow a loan amount of $200,000, HSBC’s TDMR-Pegged Package is the cheapest at 1.65%. Using this as a comparison, a home owner would need to pay $907 per month by taking a HDB loan, as compared to $814 per month by taking the HSBC home loan ($200,000 mortgage, 25 year repayment at 2.6% versus 1.65%). Therefore, assuming interest rates for both packages stay constant, a home-owner who took up the HSBC TDMR-Pegged package would have saved approximately $28,000 over the loan tenure.

Banks also tend to reward loyal customers for doing more banking activities with them. By taking a bank mortgage loan, the homeowner will be able to earn higher interest rates on their savings deposited. Some common savings accounts are the DBS Multiplier, Standard Chartered Bonus Saver Account and the Maybank SaveUp Account. The additional interest rate given to your savings is on top of the savings that you may have already incurred as a result of paying lower interest expenses on your home loan.

If you are able to apply a savvy refinancing strategy, you will be able to gain some form of control over the interest rates that you pay on your bank mortgage loans. Some of the strategies include

Actively comparing home loans on comparison website such as SingSaver to get the best quote,

refinance only after lock-in periods are over to avoid paying any penalties,

negotiate with the banks for waivers on items such as legal fees etc.

Therefore, by applying a smart refinancing strategy, you can further maximize the savings on your bank mortgage loan.

Do note that a bank mortgage loan has some slight disadvantages as well. A higher downpayment (20% of purchase value) is required, of which at least 5% must be in the form of cash. Therefore, greater cash outlay will be required when choosing a bank mortgage loan over a HDB loan. However, if your budget meets this cash outflow, then this will not be an issue to you. For such group of prospective home-owners, it makes perfect sense for them to choose a bank mortgage loan.

Here’s an exclusive offer from SingSaver: Apply for a home loan and receive $200 cash upon approval. For more details, click here.

Many of us know the importance of personal financial planning, but do not know how or where to get started. Some of us are hesitant to approach a financial consultant for advice, in fear of being pressurized to commit to a financial product. Some of us may seek out advice or recommendations from our friends, family members, and colleagues, but the advice may not always be suited to our personal needs. Many of us are put off, or even intimidated, by hearing all the unfamiliar financial jargon.

These are just a few of the many difficulties that we encounter in personal financial planning. What if we could remove these challenges and get free, easy to understand, and personalised financial advisory at our fingertips?

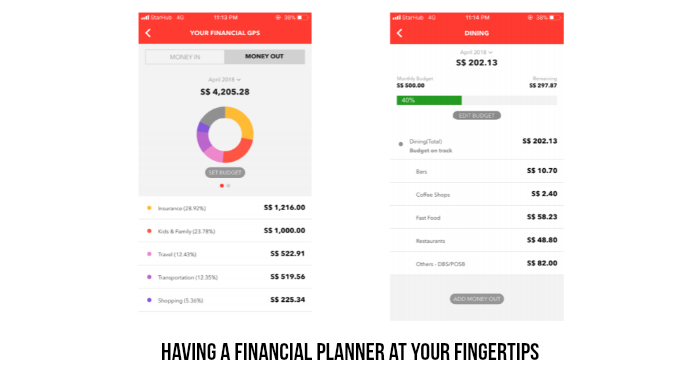

Introducing Your Financial GPS

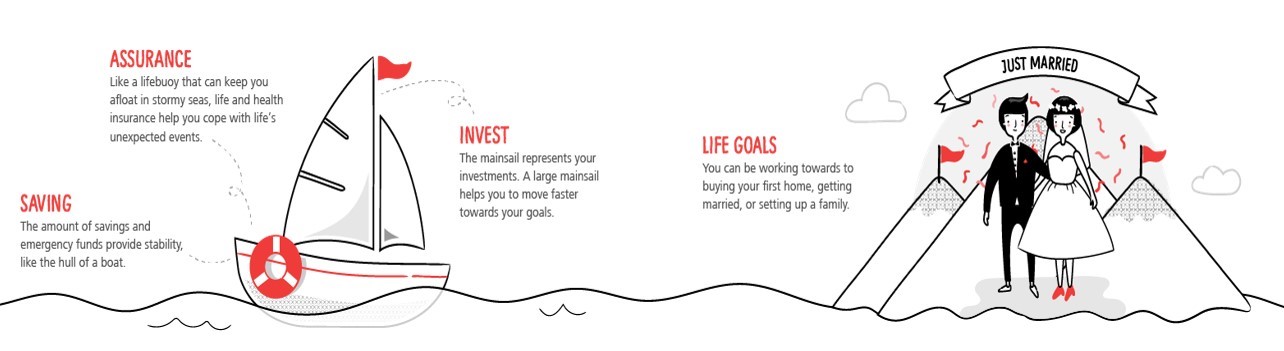

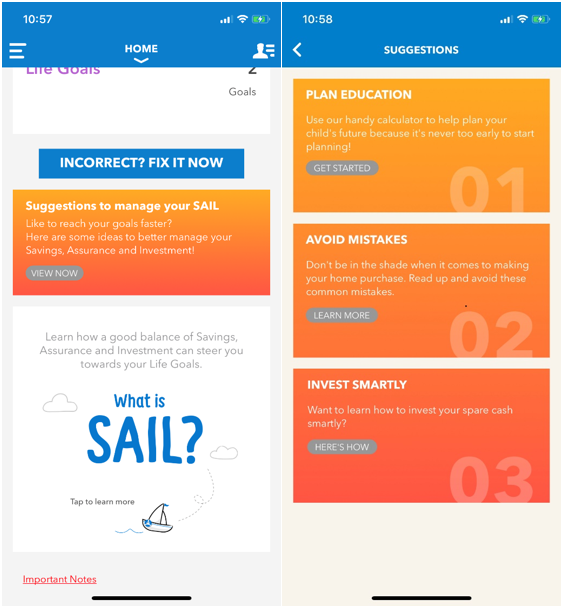

Here’s introducing NAV -Your Financial GPS, a digital financial advisor that helps people like you and me navigate through personal financial planning effortlessly. Your Financial GPS makes the principles of personal finance easy to understand using the acronym ‘SAIL’, which stands for Saving, Assurance, Invest and Life Goals. Starting with Life Goals as the destination for our journey, the other ‘SAIL’ components act as the mainsail, lifebuoy and hull of the boat to help us move towards our destination. For the boat to weather through storms and successfully reach its destination, all ‘SAIL’ components must be looked after, and well-balanced. Thus, this helps to simplify the process of financial planning for many.

Your Financial GPS At A Glance

Your Financial GPS is available to all DBS and POSB customers through the DBS/POSB iBanking and digibank app. When you log into your DBS/POSB iBanking or digibank app, you will see a tab for Financial GPS, which provides a personalized snapshot of your financial health. Your Financial GPS allows you to check your monthly spending across different categories, set budgets, and provides personalized insights based on your saving and spending information.

As a digital financial advisor, Your Financial GPS also provides a snapshot of your current SAIL status. It provides insights on the areas in which you can work on, and suggestions on how to work on these areas to achieve your life goals.

For me, personalizing Your Financial GPS for myself was a breeze. Most of my spending was linked to my DBS Live Fresh card, which was automatically categorized into different categories under spending. For spending that I have incurred using cash or on other banks’ credit cards, I could easily add in the amount as expenses so that Your Financial GPS has a comprehensive picture of my total finances.

I also set up my first Life Goal, which was to pay off my home down-payment of $300,000 by age 40. Your Financial GPS immediately calculated the amount of money which I would need to set aside monthly to achieve this goal. This helped me realise how unrealistic my goal was, which was similar to key insights of how many do not know how much they need for their goals. This was one of the insights that DBS had learnt from its intense and rigorous research to understand customers’ financial planning needs. Besides that, Your Financial GPS also came up with a list of suggestions tailored to my life goals, one of which was very relevant advice on how to avoid common mistakes as a first-time home buyer.

DBS NAV Hub: Free Personalized Financial Consultations

Want to do even more for your personal finance? Book an appointment with the dedicated NAV Crew at the DBS NAV Hub for a free personalized financial consultation. During the private one-on-one session, the crew will help you to assess your financial health and answer any money-related questions you might have. You will receive a free report on your financial health, with absolutely no product or sales pitches involved.

Ready to Sail?

Here are three ways how:

Your Financial GPS

DBS Nav Hub

DBS Nav Website

Available on DBS/POSB iBanking

and Digibank

Click to download the DBS Digibank SG app on iTunes

or on Google Play

Whatever your reason may be for buying yourself a car, you should take out car insurance immediately afterward. After all, you wouldn’t want to face legal repercussions for driving without any car insurance. But if it’s your first time to purchase car insurance, it’s easy to do it wrong, especially with so many insurance companies out there offering protection for both your car and your finances. To make taking out car insurance easier for you, here are some key tips to consider:

1. The state where you’re residing would require you to purchase third party cover as a bare minimum

There’s no telling at all when your car might accidentally hit a person or a piece of property no matter how defensive you are with your driving. The person your car hit might get injured or even die. The piece of property that your car had crashed into might become unusable or beyond repair.

Worse, the entire balance of your savings account might not be enough to cover the medical or funeral costs of the person that your car had hit. It might also not be enough to cover the repair or replacement costs of the property that your car has damaged. As a result, most states would require you to buy third party cover as part of the car insurance that you’ll be taking out from your chosen provider.

Unfortunately, third party cover won’t be able to shoulder any damages that your car had sustained as it only covers costs associated with a person or piece of property that your car had hit.

While not a state requirement, you might want to purchase comprehensive cover as well.

On the other hand, if you want any damages that your car had sustained shouldered by your chosen insurance provider, you should buy comprehensive cover instead. This will help with any repair costs associated with your damaged car.

Your car insurance’s comprehensive cover can also act as a third-party cover since the former allows for a wider coverage compared to the latter as evident in its name. The said type of cover can also shoulder you financially in case your car is consumed by fire, stolen, or hijacked.

You might want to include some extra features on top of the car insurance that you’re planning to take out.

Having a third party or comprehensive cover might not be enough once you take out car insurance as it might not sufficiently cover any highly specific damages that your car may sustain at any given time. Thus, you might want to have some extra car insurance features so that you can still get protected no matter what unfortunate situation might happen to your car. Some of those additional features that you can consider including in your car insurance are as follows:

Windscreen cover – useful for when your car’s windshield, side windows, or rear window gets broken or cracked, and you want to recover the cost of having any of them either repaired or fully replaced

Fire and theft cover – as the name implies, useful in case your car either gets burnt to a crisp by fire, stolen by burglars, or hijacked and you haven’t taken out comprehensive cover as part of your car insurance policy

Zero depreciation cover – aims to add value to your car insurance’s comprehensive cover by excluding costs associated with your car’s depreciation in value due to age, wear and tear, etc.

You might want to consider looking into other types of car insurance coverage as well.

As both third party and comprehensive cover of your car insurance might not be enough to help you financially, you might want to consider including the following additional types of car insurance coverage in your car insurance:

Collision coverage – covers repair costs associated with your car after you’ve gotten involved in an accident with another driver regardless if the said incident was your fault or theirs, though you’ll want to add this one only if you’ve bought your car new and not used

Uninsured and underinsured motorist protection – useful if an uninsured or underinsured driver had hit your car since they’re unable to pay any repair costs associated with it but you wouldn’t want to pay those costs out of your pocket at the same time

Personal injury protection – Pays for all medical expenses and lost wages that you or any passengers that you’ve brought along with you in your car would incur after you’ve gotten involved in an accident

The amount of your car insurance premiums depends on the amount of risk that you’re posing to your chosen insurance provider.

Your car insurance premium is the amount of money that you’ll have to pay for the car insurance that you’ll be taking out from your chosen provider. How much your car insurance premium will amount to is proportional to the degree of risk that you’re carrying with you as a driver.

Your chosen car insurance provider would gather information about you including but not limited to your age, criminal record, and residence’s location to determine the degree of risk that you’re posing to them. The higher the risk that you’re posing to your chosen provider, the more expensive your car insurance premium would get.

Thus, if you want to pay an affordable car insurance premium amount, you’ll have to lessen your degree of risk.

Ask your chosen provider if the car insurance would cover you in certain situations other than driving your car or not.

There might be some situations where your car had gotten involved in an accident, but you weren’t the one behind the wheel at the time when the incident had occurred. Or you might have been driving somebody else’s car or a rental vehicle when you’ve gotten involved in an accident.

In cases such as this make sure the provider covers this prior to taking out the insurance to make sure you’re fully covered.

Pay your car insurance premium either as a lump sum or in installments depending on how much money you’re willing to give to your chosen provider.

As already mentioned earlier, the money that you’ll pay is known as a premium. You can pay your car insurance premium in one go covering an entire year and even get a discount from your chosen provider while at it. But if that’s too heavy of a financial burden to you, you can pay your car insurance premium in two, four, or 12 installments instead. However, you should take note that the higher the number of installments, the higher the additional fees that you’ll have to pay as well aside from your car insurance premium amount.

When the policy period expires, they’ll automatically renew it unless it isn’t eligible for renewal anymore.

Right now, there’s no such thing as multi-year car insurance. In fact, the longest car insurance policy period is only a year followed by six months and one month. However, car insurance with a policy period of only one month is usually reserved by providers only for those drivers that they’ve assessed as high-risk. Thus, the car insurance that you’ll be taking out from your chosen provider may have a policy period of either six months or one year.

Once your car insurance’s policy period comes to an end, your provider would automatically renew it, especially as your car insurance is most likely to have an auto-renewal clause included in it. But if your provider didn’t automatically renew your car insurance’s policy period either because you’ve become a high-risk driver or you’ve moved to a different state, you’ll have to take out car insurance from another provider instead.

Conclusion

All 50 states in the U.S. require every car driver passing by the nation’s roads to carry car insurance. Thus, unless you want to break federal and state laws, you should look into car insurance after successfully purchasing a car. However, as you may be clueless about buying car insurance, the above-listed key tips to consider should make taking one out an effortless process for you. After all, better safe than sorry.