With an abundance of low-cost investment brokerages and a wide range of investment products, we believe that anyone can get started on investing. Unless your ambition is to become a day trader, you do not need to master technical analysis or complex charting techniques.

Simply carve out your path by following these steps.

#1: OPEN AN INVESTMENT BROKERAGE ACCOUNT

Unlike your comfort food, stocks cannot be bought at a store and taken home in a paper bag. You need to go through an account with an investment brokerage. A brokerage is a company or firm that acts as the middleman to connect you to the stock exchange.

Brokerage companies usually receive compensation by means of commissions or fees that are charged once the transaction has been completed. Brokerage accounts charge through minimum fees (i.e., to pay on each trade) or trading fees (i.e., percentage of each trade). These fees will affect your profits, so ensure that you do your research.

#2: FUND YOUR ACCOUNT

It is necessary to transfer money to your account to begin trading. Take note of the brokerage company’s requirements such as the minimum fee.

These companies generally accept multiple funding methods such as PayNow transfer, FAST transfer via online banking, or overseas remittance. Use a method that suits you best.

#3: DETERMINE WHICH STOCKS TO INVEST IN

Do your research, ask financial questions, and compare the facts to determine which stocks to invest in. There are different types of investment products such as Blue chip stocks and Real Estate Investment Trusts (REITs).

Blue chip stocks are the stocks of well-known, high-quality companies that are leaders in their industries. Investors usually hang on to these stocks for long periods and collect its dividends. Local “blue chips” include Singtel, DBS, and ComfortDelGro. Many Singaporean investors prefer to invest in blue chip stocks because of its perceived certainty and stability. Local blue chips are deemed to be less risky and are often common household names that most Singaporean investors can relate to.

Real Estate Investment Trusts (REITs) allow you to buy shares in a variety of properties. For instance, CapitaLand and Ascendas gives you access to purchase shares in commercial properties such as shopping malls and office buildings. It is one of the most popular options for investors seeking regular income.

#4: ACQUIRE YOUR FIRST SHARES/STOCKS

Once your funds have been sorted out, you can buy your first shares/stocks using your brokerage’s online platform. As a beginner, you may make investing a regular habit by spending a fixed amount every month on generic Exchange Trade Fund. The Exchange Trade Funds (ETFs) are similar to mutual funds in many ways. Although, ETFs are bought and sold throughout the day on stock exchanges.

Image Credits: unsplash.com

The idea is that over the long term, the ETFs will rise. By buying a fixed sum every month, you will be able to spread out your risk through ups and downs. Consistently funding your account is key.

Peer-to-Peer or more commonly known as P2P lending started in the US and UK in 2005, and has since taken the world by storm. Back home in Singapore, P2P lending contributed to approximately USD 207 million in financing offered to businesses here in 2020. Investors on P2P lending platforms can participate in these financing and earn returns in the form of interests.

Take for example Funding Societies, a popular P2P investment platform amongst Singaporean investors. It is currently licensed in Singapore and has operations in 3 other SEA countries. Backed by Sequoia India, Softbank Ventures Asia, SGInnovate amongst many others, the platform has grown at a rapid pace since launching in Singapore 6 years ago. Here are some things to note when investing with Funding Societies:

Low barrier to entry: Investors can invest as low as $20 per loan

Short tenor: Investment tenors are quite short ranging from 1 to 12 months

Returns on Investment for each Product Type: Interest rates usually range between

3% – 5% per annum for a Guaranteed Investment product;

6% – 8% per annum for a Property-backed investment product;

8% – 18% per annum for Invoice financing and Working capital related investments products

Risks and Returns of P2P lending in Singapore

Investors are able to invest by crowdfunding the business financing available on the platforms and potentially earn returns in the form of interests typically ranging in the mid to high single digits. The investment amount starts as low as $20 at Funding Societies, which investors can leverage on for their portfolio diversification. Depending on the loan product, payouts can be done monthly so investors get their investments and returns in a shorter time frame. Compounding returns, as well as a rather short learning curve, are also attractive incentives as well.

That said, repayments can be delayed or go completely unpaid. This is why it is imperative for the P2P lending platform to first do a preliminary round of due diligence and present the facts comprehensively to investors, before allowing investors to decide whether or not to proceed. There is also a risk of the P2P lending platform shutting down if it is not financially stable on its own. To mitigate this risk, P2P platforms regulated by MAS can engage an independent escrow agent to handle all investor funds separate from its business account, such that the escrow agent will hold the funds even if the platform goes under. Funding Societies does just that to provide peace of mind to investors. As such, there is a need to do your due diligence and ensure such investments match your risk appetite.

How can Diversification help to minimise risks in P2P lending?

One of the largest risks in investing in a P2P lending platform like Funding Societies is the risk of a SME defaulting. Portfolio diversification by means of investing into a good mix of notes and industries on the platform is one way to mitigate concentration and default risks and optimize your portfolio returns in the long run.

Taking the above scenario as an example, we see that Andy invested S$800 into a single deal and this single investment makes up 50% of his overall portfolio. Whereas in the other scenario, Emma invested S$50 uniformly across 100 deals, making a single investment just 1% of her overall portfolio. In the event that Deal A defaults, Emma’s potential loss will only be 1% of her overall portfolio whereas Andy might face a potential loss of half of his overall portfolio.

Conclusion

Although P2P lending is still a fairly young industry within Singapore, the demand is ever increasing. Given that 99% of businesses in Singapore are SMEsand that the returns on investments typically range in the mid to high single digits interest rate per annum, P2P lending in Singapore serves both the needs of SMEs and investors. With all that said, it is important for investors to do their own due diligence and measure the risks involved against their own risk appetite.

Investors must sign up with the aforementioned promo code and make a total investment of at least S$200 by 30th Apr 2021 to be eligible for the $20 cashback. Cashback will be credited into the eligible investors’ accounts by the end of May 2021. Funding Societies’ investor T&Cs apply.

Funding Societies is the largest SME digital financing platform in Southeast Asia. It is available in Singapore, Indonesia, Malaysia and Thailand, and backed by Sequoia India, Softbank Ventures Asia Corp and SGInnovate amongst many others. It provides business financing to small and medium-sized enterprises (SMEs), which is crowdfunded by individual and institutional investors. Investors can invest from as low as S$20 with a tenor of no more than 12 months.

Disclaimers:

This article is contributed by Funding Societies.

It should not be construed that Moneydigest is endorsing this article or any of the products and services provided by Funding Societies.

The content and materials made available are for informational purposes only and should not be relied on without obtaining the necessary independent financial or other advice in connection therewith before making an investment or other decision as may be appropriate.

Actual returns may be lower than the expected rates of return, and historical rates of returns may not reflect future returns. The Product type interest rates indicated in the article are derived from historical rates of returns and are exclusive of service fees.

All information in this article is accurate as of 29th March 2021

One of the questions we get more often is how to choose a broker. There are many and all offer different services and publicize diverse features. How do you make sure you’re choosing the right one for you?

There are certain steps that we can walk you through to choose a forex broker that suits your trading style and your general level of expertise.

First of all, traders, mostly beginners but also experts, must think about their goals in the currency exchange market, as well as their needs in terms of strategies, currency pairs, and spreads.

Then, traders can start matching forex brokers to their standards and narrowing down the search by establishing clear priorities. As a trader, do you care more about low spreads and cheap deals? Or do you prefer to have quality customer service? Or maybe do you need a list of PayPal forex brokers?

Your needs and interests

Being clear about your priorities is a must for anyone trying to figure out what broker is best for you.

You can start by thinking of what’s your style of trading. Some traders are more interested in short-term investments and maybe day trading is a better option for them. Others prefer a longer investment and may have less time to spend in the market every day.

When it comes to forex, there are different trading strategies. Apart from day trading, there is also trend trading, price action trading, swing trading, and many more. Which one suits you better?

Another aspect to consider is your level of expertise. While forex trading is easy and accessible, traders need to be familiar with spreads, pip, and market trends. How much experience you have in forex trading will also determine what broker is best for you.

What to keep in mind when choosing a Forex broker?

There is a wide variety of aspects that may be a priority for some traders, but some should be considered by all. Especially when talking about security and regulatory bodies. Other aspects are spreads and speed of execution, initial deposits, customer service, and a general feeling of the brokers’ online platform.

Security and regulatory compliance

Any search for a new broker should start here.

Making sure the forex broker you are considering is registered with the regulatory bodies in place in your country of residence is a must. This will guarantee your safety as an investor and the security of your money.

Forex trading is strongly regulated in most countries and there is a good reason for that. Wherever there is a chance to make money, there are also scammers and fraudulent operations in place. The best way to avoid them is to simply disregard any brokers with shady regulatory registrations.

Spreads and commissions

Some brokers have a good reputation for offering lower spreads and this means lower commissions and higher chances to make a profit.

While this alone should not be the only thing to consider, it’s undeniable that it plays a big part in many investors’ considerations when choosing a broker.

Trading platform

Making sure you are familiar with the platform your broker offers, and you can use it to its maximum potential, is very important. It guarantees you are investing in the right way and taking advantage of all the features they offer, which ultimately, help you increase your income.

Most brokers today offer a demo account which is not only a good way to start learning about the forex market and experimenting with different strategies but also a good way to see if you like the platform and suits your trading needs.

Ever since Bitcoin came around, the debate between the digital asset and gold has been ongoing, trying to determine which is the better store of value. Proponents of each asset have numerous reasons why they believe one is better than the other. The interesting thing is that both share some traits like scarcity, which has led to Bitcoin being referred to as digital gold.

In terms of price, Bitcoin seems to have the upper hand over gold, with its value ten times more than that of its physical counterpart. The digital asset currently trades above $18,000 after gaining 18% over the past week, while gold prices sit at around $1,800. Bitcoin is on pace to beat it’s all-time high of $20,000 attained towards the end of 2017, and the latest bull run seems to have spiked the number of Google searches on how to trade Bitcoin. Unlike conventional cryptocurrency exchanges, PrimeXBT allows users to trade CFDs for BTC and profit from any positive or negative price changes. CFD products allow one to speculate on financial markets like crypto without having to own the underlying asset.

Billionaire Investor Who Loves Bitcoin

Recently Stanley Druckenmiller, a former hedge fund manager and billionaire investor revealed he owned a portion of his investment portfolio in BTC before explaining why it could be a better investment than gold.

Druckenmiller founded Duquesne Capital back in 1981 and ran it for almost three decades before shutting it down in August 2010. Within the period, he managed money for prominent individuals like George Soros, and together they made massive profits betting against the British pound in 1992.

Speaking to CNBC last week, the investor worth $4.4 billion, according to Forbes, said that even though he was “a bit of a dinosaur,” he had opened up to the idea that BTC could be a better asset class than gold with lots of attraction as a store of value.

He added that since it was created around 12 years ago, Bitcoin has picked up more stabilization with each passing day. Interestingly, other than BTC, Druckenmiller claims to have a lot of gold in his portfolio, more than BTC.

JPMorgan Believe Bitcoin Will Thrive

In a note to investors recently, JPMorgan claimed Bitcoin competes better than gold as an alternative currency. BTC is up 157% since the beginning of the year, with its latest rally fueled by the PayPal announcement. The company will allow its users to buy, sell, and hold the digital asset in their accounts in a few weeks. PayPal noted that more than 26 million merchants using the platform would have the ability to accept crypto as a funding source.

JPMorgan believes BTC can compete against gold because of its attractiveness to millennials, who are set to become a more important participant in the market over the coming decades. Therefore, their preference for BTC over gold should set up the cryptocurrency for success. Still, BTC has a long way to go if it’s to match the gold market, which is valued at around $9 trillion.

Currently, the Bitcoin market cap is around $330 billion. And if it’s to gain tractions as an alternative currency to gold, JPMorgan sees its price doubling or even tripling in the near future, making the current price of $18,000 modest.

Besides being a store of value, crypto drives its value for its utility as a means of payment. According to JPMorgan, the “more economic agents accept cryptocurrencies as a means of payment in the future, the higher their utility and value.”

BTC Is Better On Some Measures

Bitcoin is a clear winner compared to gold when it comes to portability. It’s a digital asset that exists on computers as code; therefore can be quickly sent and received to any corner of the world as long as there is an internet connection. Banks do not control it, so it’s easy and fast to send and receive payments in the asset across borders.

On the other hand, if you don’t hold the gold yourself accessing it is a problem, and even if you have it, moving it around can be inconvenient. Additionally, there have been cases where the government has tried to ban privately owning gold like it was the case in the US for 41 years. Such censorship can be inconveniencing and isn’t possible with an asset like Bitcoin that isn’t controlled by anyone in particular.

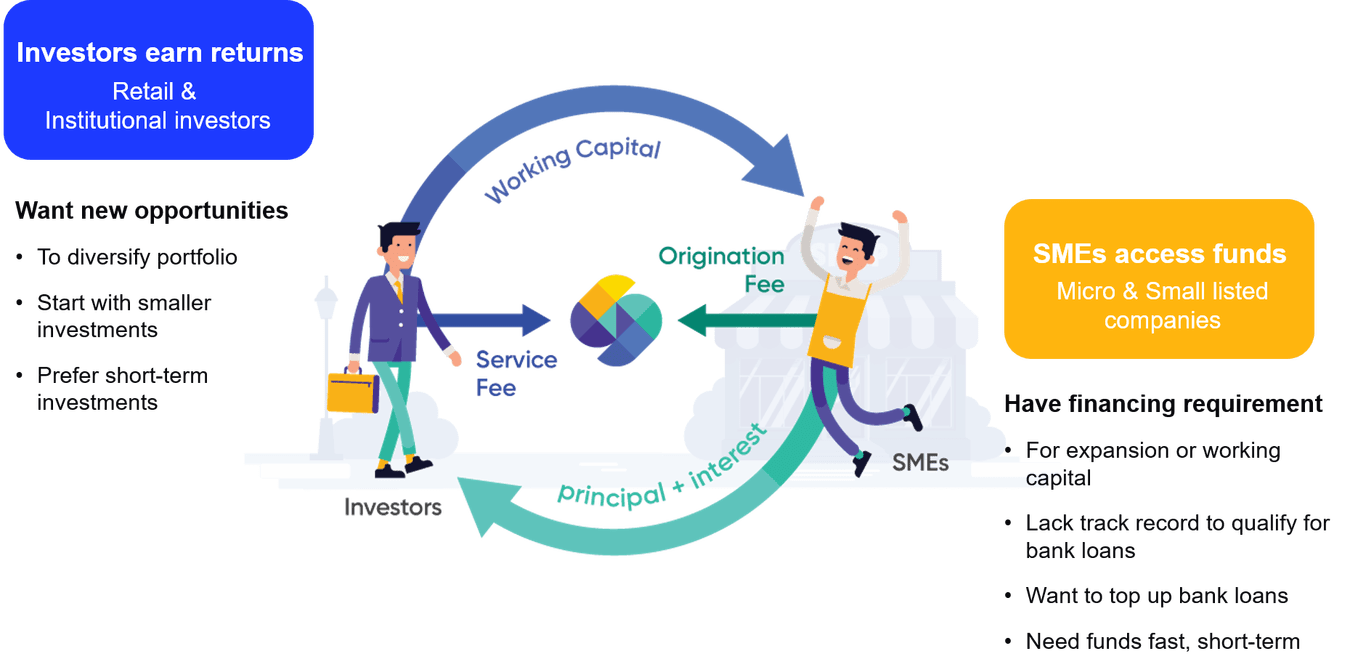

P2P investments or more commonly known as Peer-to-Peer (P2P) lending is a type of debt-based crowdfunding enabled by digital platforms that connect borrowers with investors without going through a traditional financial intermediary such as a bank. This concept will see investors lending to borrowers (i.e. SMEs) via the platform as a form of investment, and the interest earned from it will be their returns. Despite being a relatively new concept in Singapore, it has grown significantly over the years and has shown no signs of slowing down.

How does P2P investment work for investors?

For investors, it is a means for diversification into another asset class. As most P2P investments offer a frequent repayment schedule (monthly or within 90-120 days period), it can be considered a great supplement to more traditional long term asset classes like stocks or bonds. With interest rates on saving accounts heading south, investors can look for alternative ways to earn interest on their cash.

How much can investors earn?

Be it an individual or institutional investor, the reward on their investment will come in the form of the interest payments serviced by the borrower. At Funding Societies, investors can choose to participate across 6 different investment products with interest rates ranging from 3% – 18% per annum.

Risks and returns go hand-in-hand and the difference in interest rates range is tied to the risk associated with the product. For example, a guaranteed returns investment will yield an interest of between 3% – 5% p.a. while an unsecured business term investment can fetch between 8% – 18% p.a..

How much to invest in P2P investment?

There are no hard and fast rules on how much of one’s portfolio should be allocated to any particular investment assets, and this is the same for P2P investing. What is important is that investors should always consider diversifying across many notes and avoid concentration risk to create a healthy well balanced portfolio.

At Funding Societies, investments start from S$20 onwards and most products provide a periodic repayment of principal and interest. Jointly, it is a great recipe for investors to diversify and reinvest their investments.

P2P investment with Funding Societies

Funding Societies is Southeast Asia’s largest P2P lending platform with over S$1.7b in SME financing funded. In Singapore, the platform holds a Capital Markets Services (CMS) Licence and is regulated by the local authorities. Over the years, they have been able to raise several rounds of equity funding led by investors such as Sequoia India, Softbank Ventures Asia and SGInnovate to name a few. A few things to note when investing with Funding Societies:

Interest returns are exempted from tax: For interests earned in year 2020 onwards

Low barrier to entry: Investments start from $20 per note

Short tenor: Investment tenors ranges from 1 to 12 months

Returns on Investment: Interest rates usually range between 3% to 5% per annum for a Guaranteed Investment product, 6% to 8% per annum for a Property-backed investment and 8% to 18% per annum for Invoice financing and unsecured business term investments

Default Rate: The Singapore platform default rate is 1.89%

P2P investment products

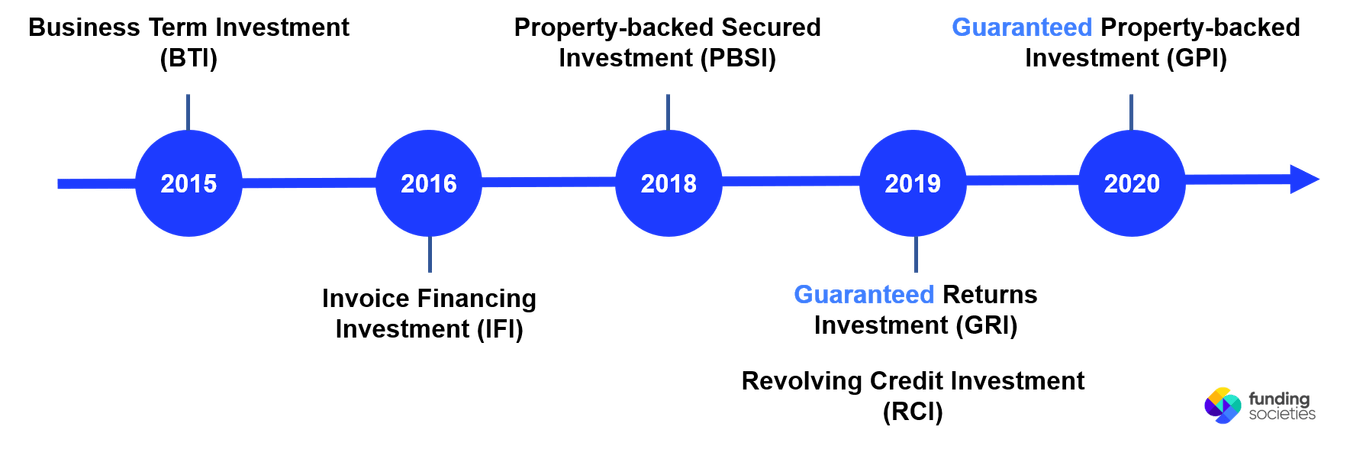

As the investor base grew overtime, they needed to continuously innovate new products to meet the needs of a wider range of investor profiles. Having launched the first product back in 2015, Funding Societies has now grown to offer 6 different investment products with varying levels of risk-return profiles.

TL;DR: P2P Investment Products Overview

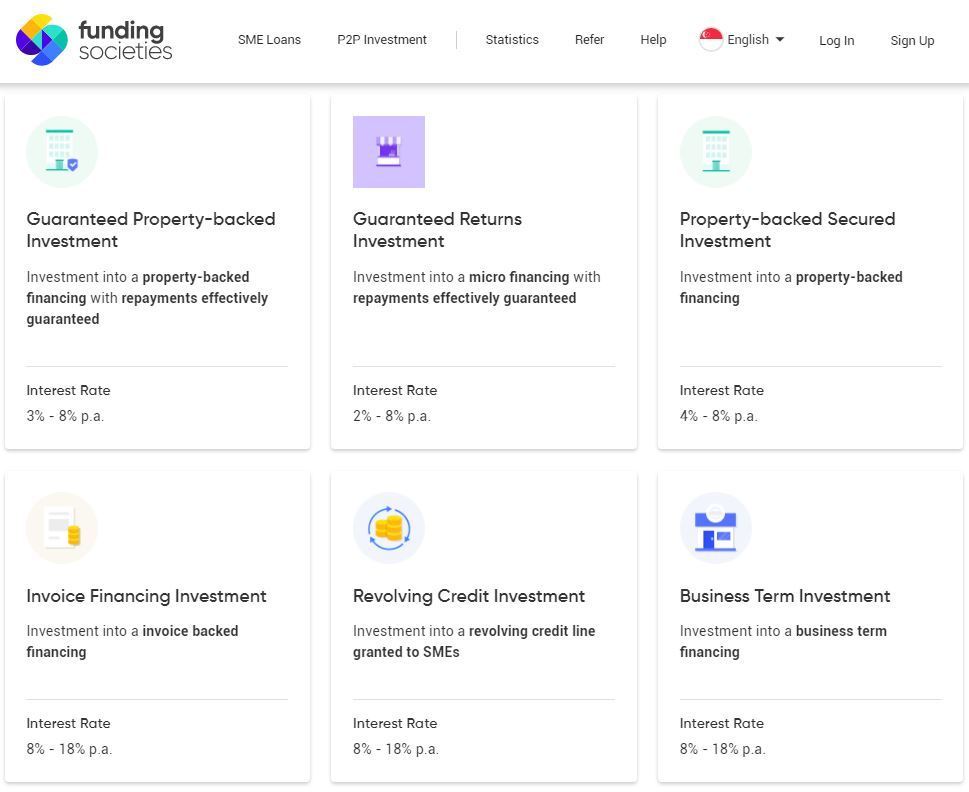

1. Property-backed Secured Investment

The Property-backed Secured Investment (PBSI) is a rather unique collateral-backed investment product launched to provide investors with an additional security in the form of a local Singapore property to back the investment. The property is pledged by the SME undertaking the financing.

Funding Societies holds first charge on the property on behalf of investors and it can be auctioned off to recover funds should the SME defaults.

To alleviate concerns on property value fluctuations, the percentage of financing amount varies as per the property types (residential/commercial/industrial) and in most cases is only up to 70% of the property value. The forced value of the property is also considered while arriving at the financing quantum. By doing so, Funding Societies maintains a buffer for fluctuation in property prices as well as for distress sale situations. The interest rate for this investment product is typically between 4% – 8% per annum.

2. Guaranteed Property-backed Investment

Launched in July 2020, Guaranteed Property-backed Investment (GPI) is an investment into a Property-backed Secured Investment with an additional effective guarantee of repayments to investors. Likewise to Property-backed Secured Investment, Funding Societies has the right to liquidate the property to recover the funds should the SME fail to fulfil their obligations.

Falling under the Guaranteed line of products means that both the principal & interest repayments are effectively guaranteed to the investor regardless of the SME’s status. The interest rate for this investment product is typically between 3% – 8% per annum.

3. Guaranteed Returns Investment

Guaranteed Returns Investment (GRI) is another investment product under the Guaranteed line of products. This product was first launched in August 2019 as a means to offer more investment opportunities to investors.

GRI is an investment into a micro financing with repayments effectively guaranteed. Similar to GPI, investors are effectively guaranteed to receive both the principal & interest repayments when they participate in this investment product. The interest rate for this investment product is typically between 3% – 5% per annum.

Please invest with the knowledge that while returns are effectively guaranteed by FS Capital Pte. Ltd., there may be a chance where we might not be able to fulfil the obligations under this arrangement. To mitigate this risk, a cash reserve buffer to allow for repayments to be made on time is maintained.

4. Invoice Financing Investment

The Invoice Financing Investment (IFI) product allows investors to invest into an invoice backed financing offered to SMEs. SMEs take this financing by pledging against the receivables of an invoice. By doing so, it helps to bridge the cash flow gap between actual sales and receipt of payments.

Due to the nature of the financing, investors in this product usually enjoy a relatively short tenor of 30 – 120 days. The short tenor enables investors to receive and reinvest their money relatively quickly. The interest rate for this investment product is typically between 8% – 18% per annum.

5. Revolving Credit Investment

If you own a credit card, you will probably be aware of how revolving credit or more commonly known as a line of credit works. Based on one’s credit standing, they will be issued a credit limit to draw down from over time. Likewise in the case of Revolving Credit Investment (RCI), it is an investment into a revolving credit line granted to SMEs. The SME can repay anytime within the approved tenor and draw down again so long as the amount outstanding is within the limit.

As an investor, you can participate in a single or multiple drawdowns, each with a tenor typically between 1 to 12 months with a chance of early partial or full repayments. The interest rate for this investment product is typically between 8% – 18% per annum.

6. Business Term Investment

Business Term Investment (BTI) was the first product offered alongside the launch of the Funding Societies platform back in 2015. It is an unsecured financing undertaken by SMEs as a means for working capital, expansion or bridging needs. The interest rate for this investment product is typically between 8% – 18% per annum.

Be it a way to diversify your investment portfolio or to beat the falling savings account interest rates, investors can consider to embark on their P2P investment journey with a platform like Funding Societies. If you have done your own due diligence and decided to invest with Funding Societies, they currently have a promotion for new investors. Sign up with promo code MDXMAS20 and make a total investment of S$200 by 31st Jan 2021 to get a S$20 cashback.

Terms and Conditions apply

Investors must sign up with the aforementioned promo code and make a total investment of at least S$200 by 31st Jan 2021 to be eligible for the $20 cashback. Cashback will be credited into the eligible investors’ accounts by the end of February 2021. Funding Societies’ investor T&Cs apply.

Funding Societies is the largest SME digital financing platform in Southeast Asia. It is licensed in Singapore, Indonesia and Malaysia, and backed by Sequoia India, Softbank Ventures Asia Corp and SGInnovate amongst many others. It provides business financing to small and medium-sized enterprises (SMEs), which is crowdfunded by individual and institutional investors. Investors can invest from as low as S$20 with a tenor of no more than 12 months. Depending on the investment product, interest rates can range between 2% to 18% per annum.