Singapore’s growth will be dampened by external factors in 2015, says the Ministry of Trade and Industry (MTI) on Tuesday.

While we cheered about our Q3 GDP of 2.8%, which beats the forecast of 2.4-2.5% growth, external factors around the world is likely to slow growth in 2015.

Economic recovery will be mixed across different regions with economy in Malaysia and Indonesia expecting to stay resilient, thanks to healthy investment growth.

Growth in both Asian powerhouses China and Japan is likely to be sluggish due to correction in the real estate market in the former and fiscal consolidation to reduce public debt in the latter.

For China, it’s extreme fast growth has caused a bubble in the real estate market and prices has since fell for consecutive months. It’s property market accounts for 15% of GDP and the threat of it bursting may cause the downfall of China’s economy which has spillover effect other sectors such as banking and construction.

The cost of servicing Japan’s public debt is likely to eat up half of its tax revenue despite raising its consumption tax from 5-8% in 2014 and up to 10% in October 2015.

Whereas in the Eurozone, the Ukraine-Russia crisis will likely affects offshore investments due to lower business and consumer sentiments.

In the US, there are uncertainties on when the Fed will raise a hike in interest rate as they aimed to strike a balance between the dyanamics of the labour market, inflation and economic growth.

Otherwise, Singapore growth is expected to be between 2-4% in 2015, says MTI.

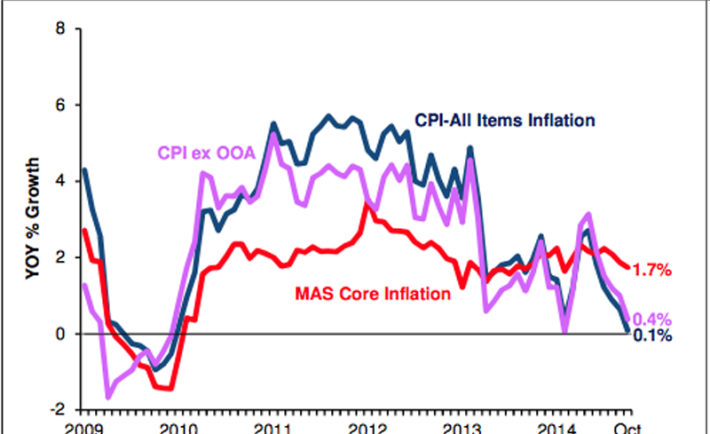

This was mainly due to the sharp decline to the cost of accommodation and oil-related items. Another reason is due to the fluctuation of the certificate of entitlement (COE) premiums.

Inflation is likely to remain low with higher supply of COE and housing units while the consumer price index of food, education and healthcare has been increasing.

Taking reference to Consumer Price Index, Oct 2014 published by the Department of Statistics, the increase in price of fruits and vegetables has contributed to the the overall increase in food price index.

Poor weather condition has attributed to the higher prices of food supply in the region.

For education, the consumer price index has increased by 3.2% as compared to last year and medical treatment has also went up by 2.8%.

Core inflation is expected to averaging between 2-3% in 2015.

To commemorate Singapore’s 50th birthday, or SG50, parents can look forward to the SG50 Baby Jubilee Gift for their newborn in 2015 unveiled by the National Population and Talent Division (NPTD) on Sunday (Nov 27). This is an initiative to achieve sustainable population.

Parents of their newborn can register for the gift at www.nptd.gov.sg/sg50baby and there are complimentary delivery or parents can self-collect them at birth registration counters of maternity hospital or the Immigration Checkpoint Authority (ICA).

There are eight items included in the Jubilee Gift Box:

1. Commorative Medallion

2. Scrapbook

3. Children’s Books

4. Diaper Bag

5. Baby Sling

6. Baby Clothes

7. Multi-functional Shawl

8. Family Photo Frame

The items and gift box are efforts of local designers such as Wang Shi Jia, founder of Ang Ku Kueh Girl and students of the LASSALE’s Design Communication students.

As reported on Telegraph, A Briton had won a £1M (S$2,031,767) lottery in Euromillions, akin to winning a S$2M Toto in Singapore. A dream that everyone wished for in their entire lifetime. Matt Myles is living the dream.

His plan?

He left his job and went on a bar hopping world tour to countries such as Indonesia and Thailand to Spain, Ibiza and America together with his brother and a few friends.

He splurged on booze and partying costing him up to £72,000, £45,000 on a Porsche and £9,000 on an Omega watch during a seven month stint. Add these up and multiply by 2 and you will get the total amount in Singapore Dollar equivalent – S$252,000 or a quarter of a million dollar spent, without taking into account of hotel and other expenses.

His plan of getting a few houses and earn passive income from rental by leveraging on mortgages came to a naught when mortgage lenders turn him away. Without a job with regular income coupled with poor credit rating amassed from his use of credit during his world tour, he is unable to get financing for his investment in properties.

Without financing options available, he ended up paying for a £150,000 house outright in full.

In Singapore, if you have that amount of credit without a regular income you don’t meet the 60% of Total Debt Servicing Ratio (TDSR) framework. That also mean that you can’t leverage on the low interest rate from your housing loan and end up paying in full, an opportunity cost that you could have generate better returns from other investments.

If you fall in the same category and is in the same boat as Matt’s, you should aim to repair your credit score by paying up your credit before reapplying again. Also consider talking to a mortgage specialist to see if there are other options for you.

And perhaps it’s time for you to get on the payroll?

In an article published by Singapore Business Review, it was found that almost half of the Singaporeans holding executive position struggle to make ends meet every month.

The statistic was first published on Jobstreet and it’s surprising to know that 44% of the Singaporean executive does not have excess saving after paying off their mortgage, car loan and credit card.

25% of them claimed that paying for insurance premium was their biggest monthly commitment.

That is a worrying trend for Singapore’s ageing population.

What this also means is that half of these executives will not be able invest or grow their savings to the effect of compounding interest. Without adequate savings to supplement their CPF payouts at their retirement age, this group of people at are the risk of outliving their retirement funds.

A study conducted by NUS draws the conclusion that the CPF is sufficient for the current group of young income earners of the 30th to 70th income percentile based on three important caveats: choice of HDB flats must be within their means, any CPF above the Minimum Sum they withdraw must be invested and they must continue to remain in the workforce for as long as possible.

The few key issues surface here are:

Carrying too much debts

For most of us, it’s impossible to live debt-free as we need to purchase our house and support our family. But before it gets out of hand, it is important to differentiate between good and bad debts.

Good debts are debts that create value to you and getting you what you need. Mortgage loan, for example, is a good debt to take on as it create value to you, considering the low interest rate. It can be bad if you leverage too much and cost you to be unable to afford the monthly mortgage payments.

Whereas, credit card and vehicle loan is a bad debt as the interest is exorbitant and the item you bought is of depreciating value – take car, for example.

Of course, it is not smart either to avoid debts at all cost if it means using up all your cash reserves for emergencies.

Not saving enough

As compared to our parents, the younger generation is simply not saving enough. For what Singapore has become today and being bred in a society where everything is provided for has denied them the opportunities to understand the importance of money.

We spend all that we earn, often lacking restraint in spending money.

As the saying goes:

A dollar saved is a dollar earned.

Save the extra dollar so that you can multiply them into many folds.

Making wrong financial decisions

Many young working adults are not savvy enough to manage their own finances. Taking on too much debts without knowing the long term effect, speculate in the stock market and dumping all their savings to purchase a car are some of the mistakes made by these group of people.

A quarter of these people spent too much on insurance. Insurance should be used as tool to hedge your risk of financial liabilities to you and your dependants – should untoward events happen to you. It should not be used as a tool to grow your money, as it is inefficient due to the high cost and fees charged. Being insured for around 10 years of your income using term insurance should be sufficient for most people and it will cost you only less than 5% of your income.