“My siblings are already fighting over my properties even though I’m still alive,” my uncle joked, acknowledging the numerous businesses and properties he owns. He stressed the importance of securing a competent lawyer to ensure his assets are distributed fairly.

You see, he plans to use his resources to establish a foundation dedicated to supporting vulnerable communities, particularly children who have been abandoned by their parents. This charitable endeavor holds a special place in his heart. He wants to ensure that his legacy will continue to help those in need even after he’s gone.

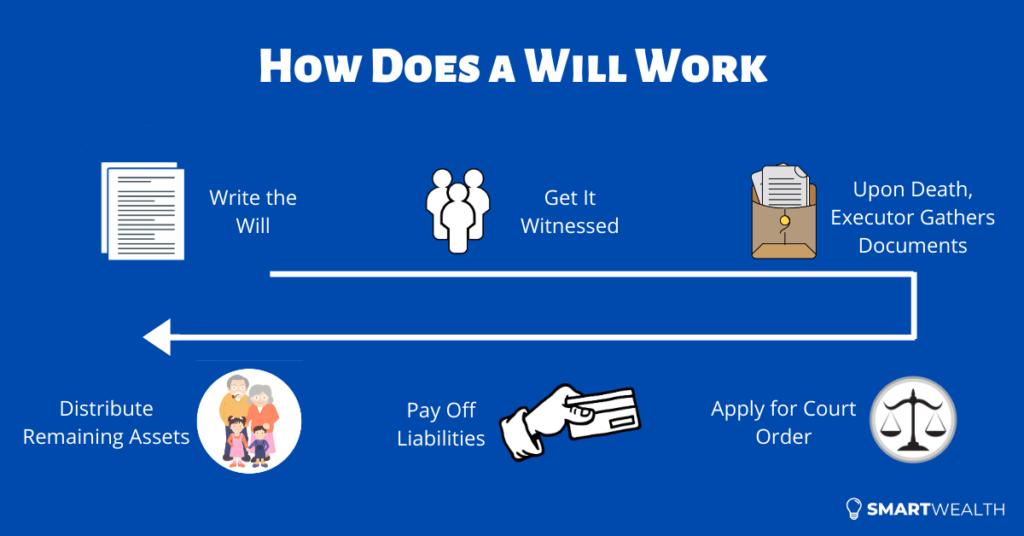

If he does not craft a Will in time, his estate will be divided according to Singapore’s intestacy laws. Having a Will will enable him to distribute his estate according to his wishes, after his death. It will allow him to give his money to the people he feels needs it most. Can you imagine how this vital document can change the lives of those around him?

Let us begin to understand what a Will is.

WHAT IS A WILL?

A Will is a legal declaration of how your assets will be distributed after your death. It prevents disagreements and provides clarity over your inheritance, which can be distributed to your loved ones or other charitable institutions after you pass away.

Apart from distribution of financial assets, a Will allows you to appoint your executors and your children’s guardians. You can approach a lawyer to help you draft a Will or use an online writing service. Feel free to change your Will anytime you see fit.

WHAT IS INSIDE A WILL?

Your Will should clearly state who is going to:

a. inherit your estate (i.e., include your beneficiary or beneficiaries),

b. take care of your children who are under 21,

c. carry out your wishes (i.e., your executor), and

d. dispose your assets if your beneficiaries pass away before you.

WHAT ARE THE BENEFITS OF ESTATE PLANNING?

1. As mentioned above, estate planning helps ensure that your assets are distributed according to your wishes after your death.

2. It specifies who will manage your affairs after you pass away to ensure that your matters are taken care of in a timely manner. Lasting Power of Attorney (LPA) allows someone to make decisions on your behalf in the event that you are unable to do so yourself.

3. It can help minimize taxes and legal fees.

4. Estate planning aids in ensuring that your business is smoothly transitioned to your heirs or successors.

CAN YOU PUT YOUR CPF IN THE WILL?

Central Provident Fund (CPF) savings are not covered under a Will and cannot be distributed via a Will.

You are strongly encouraged to make a CPF nomination so that your intended beneficiaries or charities can have quick access to the funds once unforeseen events happen. Moreover, completing your CPF nomination can help lessen administrative delays and avoid paying a fee to the Public Trustee’s Office for administering un-nominated CPF funds.

Not having a CPF nomination can result to your savings being distributed according to Singapore’s intestacy laws (or Islamic inheritance law).

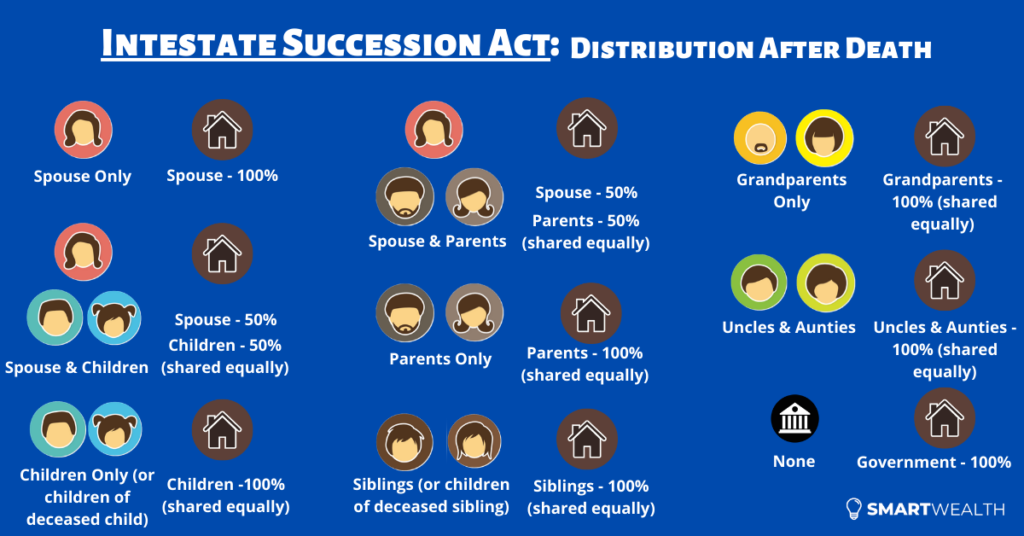

WHAT IF I HAVE NO WILL?

If you die without creating a Will in Singapore, your assets will be distributed according to Singapore’s intestacy laws or Islamic inheritance law. The Intestate Succession Act (ISA) will take effect. Distribution following the law may not be in accordance with your wishes or may not fit your family’s current financial situation.

Image Credits: unsplash.com

Having a Will enables you to distribute your assets on your own terms. Whether you want to provide for your elderly parents or your children, updating your estate plan regularly can ensure that it remains relevant and effective in light of changes in your personal circumstances and the law.

In Singapore, there’s always a constant strive to earn more money.

It’s perfectly understandable considering how high goods and services are priced, and how we want to provide a better future for our family.

Some of us take the next step by preserving our wealth and future income through the use of different types of insurance.

But only a few go even further to make it all fool-proof with estate planning.

What is estate planning all about? And what are some of the easy things we can do right now?

Let’s find out.

What Is Estate Planning?

When death happens, all your eligible assets (e.g properties, money in the bank account, investments, insurance) will form your estate which will be distributed according to prior instructions (if any).

The purpose of estate planning (which can only be done before death) is to decide how your estate is going to be distributed upon the inevitable.

This distribution is indicated with the use of several legal documents.

All these ensure that the wealth you’ve accumulated thus far will go to the intended beneficiaries (people/entities who’ll be receiving your assets), in a timely and efficient manner.

Why Should You Care?

We tend to focus on wealth accumulation (savings and investments) and wealth preservation (insurance).

But a lot less on wealth distribution (estate planning), which is equally important in the grand scheme of things.

Firstly, the process of unlocking assets will be more tedious and complex. This inevitably prolongs the time for beneficiaries to receive proceeds. If the family depends on timely money coming in, this issue will be more dire. Who’s going to provide them with liquidity to pay off current bills and expenses?

Secondly, also because of the complex and lengthy process, it’ll cost more.

And lastly, most of the proceeds will go according to the intestate succession act or the Muslim law.

Therefore, your assets may not go to the intended people. And even if they do, not in the correct allocation that you wish for.

For example, if your spouse, children and parents are still living, your assets will be distributed to your spouse and children only, and none goes to your parents (even if they raised you up since young).

And it could also go to the unintended people.

For example, if your spouse and children are still living, and you think that your spouse doesn’t deserve anything, distribution will still go to your spouse.

These will cause ugly disputes amongst family members because there’s no clear and distinct indication of WHO should receive WHAT.

Furthermore, when you’re not around anymore, there’s no one else to turn to except for any legal documents you leave behind.

But when you employ even the simplest of estate planning tools, you effectively eliminate all these potential problems.

What are some of them?

3 Core Estate Planning Tools in Singapore

When dealing with financial matters, there’s always some resistance in taking action.

For example, people always want to find out what’s the best investment before investing, which is perfectly fine. But a problem that comes out from that is that too much information paralyses them and nothing is done in the end.

It’s also the same with estate planning.

But I can assure you that setting up these 3 tools will have the most impact and take the least amount of effort.

1) CPF Nomination

If you’re a Singapore Citizen or a Permanent Resident, you will have CPF accounts – Ordinary, Special, MediSave, Retirement.

If you don’t make a CPF nomination, and death happens, distribution of CPF savings will take a longer time, higher costs and goes by the law.

So you’d always want to get it done. It’s free anyway.

But most see it as a hassle because it used to be done via hardcopy forms (with 2 witnesses) or by going to the CPF service centres.

However, back in 2020, CPF allowed the nomination to be done online, and this made the application easy and convenient. While you still need 2 witnesses, the entire process is done electronically. If you want a step-by-step guide, you can check out how to make a CPF nomination online.

Even if a nomination is made, you can easily change it in the future. It’s usually done by submitting a new one, and that will override the existing nomination.

2) Insurance Policy Nomination

If you’ve bought life insurance and think nothing else needs to be done, think again.

The second part is to make a nomination where you can specify who will receive the proceeds and in what percentage.

Nominations can be made on life insurance policies with a death benefit. Take note that nominations can only be done on private individual policies and not on company/group insurance – they’re not owned by you.

There are 2 types of nominations: revocable and irrevocable (trust). Most choose the former as the nomination can be changed easily in the future.

Although it isn’t compulsory, it’ll be useful.

This is because by nominating, the insurance company can pay out directly to the beneficiaries when there’s an eligible claim. This effectively bypasses the usual probate process, saving time and money.

But here’s a trick question: do you want to nominate all your insurance policies?

The answer: it depends.

If your proceeds are large and all your policies are nominated, it’ll mean that your beneficiaries will receive the proceeds all at once.

Will they be able to handle such amounts?

There are many cases where the beneficiaries mishandle monies, and in the end, it got them into further trouble.

So if your proceeds aren’t that much (which you should have it reviewed), then it wouldn’t matter all too much.

But if it amounts to a bigger sum, you can make nominations on a few policies just for liquidity purposes. The rest can still be specified in a Will to pay out on a staggered or monthly basis.

To make a nomination, you can download the relevant forms from the insurance company, fill it out properly and sign in the presence of 2 witnesses. Or you can approach your financial consultant to help you with it.

3) Writing a Will

Even when you’ve done the CPF and insurance policy nominations, some assets will still be left out.

Examples:

Money in the bank account

Investments over several platforms

Properties (depending on the ownership type)

etc

If you don’t make a Will, all these will still be distributed according to the intestate law or the Muslim law.

Other than the usual benefits of writing a Will, you can also use it to appoint a guardian to take care of young children and create a testamentary trust to stagger payouts.

Just know that getting a professional to write a Will only costs a few hundred dollars.

The obvious advantage is convenience but more importantly, the Will is drafted to be able to stand in court if challenged.

Other Points to Take Note Of

Apart from the 3 basic tools mentioned above, there are other aspects you should know also.

Firstly, setting up trusts can give you greater control.

Although the Will covers most needs, the trust will bring estate planning to the highest level.

These benefits include:

can be created when you’re living

provide for a special needs child

utmost confidentiality

delaying gifts to beneficiaries

etc

While higher net-worth individuals derive more value from it, there are affordable trusts out there that can suit the needs of the masses.

Secondly, a distant cousin to estate planning is advance care planning.

Have you thought of what happens when you’re neither “dead” nor “alive”? In other words, mentally incapacitated.

You can’t do anything about your finances. And estate planning doesn’t kick in.

That’s when advance care planning comes in. It also involves different tools such as the Lasting Power of Attorney and the Advance Medical Directive.

These are important because it will specify what happens next when certain situations come up.

For example, when an Advance Medical Directive is done up, you specify that you don’t wish to be on life support to artificially prolong your life.

And for the last point, you need to have wealth.

You see, if you don’t have any wealth (your liabilities are higher than assets), there’s nothing to distribute even if you’ve done estate planning properly. Even if you’re mentally incapacitated, there may not be money to even pay for your medical expenses.

That’s why, financial planning (wealth accumulation and insurance protection), estate planning and advance care planning, all have a part to play in the bigger picture.

If one is missing, your financial plan is not wearing its full suit of armour. And when a battle comes, damages will be done.

What’s Next?

Estate planning is often in the back seat.

But at times, you have to bring it to the forefront.

That means either to set up the tools or to review them.

So take small steps by looking at the 3 basic ones first – CPF Nomination, Insurance Policy Nomination, and Writing a Will.

And then explore other areas when you’re ready.

About the Author:

Abram Lim runs SmartWealth which covers topics on personal finance – insurance, savings, investments, retirement planning, etc. It strives to produce research-backed articles so that readers can make better financial decisions with objectivity.

The magical story of a young wizard named Harry Potter has captured the hearts of fans of all ages and with a good reason. In fact, I am wearing my Hufflepuff shirt while I am writing this.

Despite being in a fictional world, the Harry Potter characters’ financial problems cannot be solved with a wave of a wand. They also have to struggle with the challenges of saving, spending, and growing money throughout the series. Here are just some of the personal finance lessons that you can learn form the wizarding world of Harry Potter:

GET THE A DEPENDABLE AUTO-INSURANCE

In the “Harry Potter and the Chamber of Secrets” book, Ron and Harry crashed a car into a tree. It caused an irreparable damage to a car that they do not own. This scenario taught us the importance of having a car insurance.

In Singapore, it is mandatory to have your car insured. Examine your options and look for an auto-insurance that suits your needs and your budget. Some of the plans that you may consider are the FWD, Aviva, and NTUC Income auto-insurance plans. FWD has three auto-insurance plans from Classic to Prestige. Its annual premiums start from S$731.38. Aviva offers three auto-insurance plans too from Lite to Prestige. Its annual premiums start from S$883.12. Lastly, NTUC Income has Drivo Classic and Premium plans. Its annual premiums start from S$$970.35. Annual premiums are usually based on the driver’s profile and the car itself.

SORT OUT YOUR WILL

After living in an uncomfortable cupboard under the stairs for eleven years, the book’s main protagonist Harry Potter found out that he was a wizard and that his parents left him a considerable amount of money. His family’s wealth was beyond what he can imagine! Although his parents died at a very young age, when he was just a baby, it was clear that they a robust financial plan in place. They left all their wealth to Harry. This helped him secure his school supplies and daily needs throughout the years.

Unforeseen events can strike at any moment. It is important to save up for your retirement as soon as possible. Moreover, you must create a will that ensures the list of beneficiaries on all of your savings and investment accounts.

SEE THE POWER OF COMPOUND INTEREST

Harry not only benefits from his parents’ wealth, but also reap the rewards of compound interest. His money was untouched for eleven years. When he opened his vault for the first time at the Gringotts Wizarding Bank, he discovered the amount of gold and money that was in his vault. Despite having this wealth, he did not lead a lavish lifestyle.

Like Harry, you may benefit from compound interest by leaving your money untouched for years in a bank or by investing your money for the long haul.

APPRECIATE WHAT YOU HAVE

As I said above, he did not lead a lavish lifestyle. Harry was humble. In fact, he wore the same glasses for seven years. He appreciates what he has and exemplifies this trait the most in the first book. When Hagrid gifts him Hedwig the owl, he was amazed and accepted it wholeheartedly. He was also very grateful when he was gifted the Nimbus 2000 by Professor McGonagall.

In our world, it is easy to be caught by all the sale items and designer brands. However, you must remember to strike a balance between your needs and wants. Appreciate what you have and live within a realistic budget that you set.

SECURE YOUR MONEY IN A SAFE PLACE

Harry’s immense fortune was stored in the Gringotts Wizarding Bank, located in the heart of London. The bank is operated and guarded by goblins. These goblins serve as the gatekeepers to the underground vaults. It is often described as the safest place in the Wizarding World.

Image Credits: unsplash.com

While you cannot keep your wealth within the protection of magical spells and goblins, you can secure your money in other ways. Firstly, you may set up an auto-deposit scheme to send a portion of each paycheck to your savings account. Secondly, you may store your emergency fund in a place where you will not be tempted to spend it frivolously. For instance, you may set up a different account exclusively for that. Lastly, secure your online banking apps through Two-Factor Authentication.

Estate planning advice often focuses on the creation of legal documents such as wills and trusts. The choices you make about where your assets will go after you pass can affect people’s lives profoundly. This is why you must familiarize yourself about the basics of estate planning.

DEFINITION

In simpler terms, estate planning dictates how you would like to distribute your estate after your death. Your estate encompasses your properties, savings, and money. It makes sure that the people you love and the causes you care about are covered even after the inevitable event of death.

TRUSTS

As said above, estate planning primarily includes the creation of a will by appointing an executor. For individuals with higher net-worth, they may choose to create a trust in order to transfer their assets to pre-determined beneficiaries. Singapore is a prime financial hub for individuals with higher net-worth to set up their trusts. It is because the country is characterized by:

a business promoting environment,

a comprehensive legal system,

a globally competitive infrastructures,

a strategic geographic location, and

a robust set of regulations for the financial sector.

As trusts are used as a long-term tool, you must closely evaluate the pros and cons before setting one up. For instance, trusts are a viable option for vulnerable beneficiaries such as minors. However they can be costly and difficult to maintain.

TERMS

Here are the common estate planning terms that may boggle your mind at first:

Alternate Beneficiary is an individual or an organization named to receive the assets in the unlikely event that the primary beneficiaries die.

Co-Trustees are two or more people who had been named to coordinate in managing a trust’s assets.

Durable Power Of Attorney For Asset Management is a legal document that bestows a person full or limited legal authority to sign your name on your behalf in your absence. Its validity ends at death.

Gross Estate refers to the value of an estate before the debts are paid.

Will is a written document that includes the instructions for allocation of assets after one’s death.

Whether we like it or not, death is inescapable. This is why it is important to prepare a “Will”, especially if you are retiring soon. The essence of making a Will is not only to prepare for the event of death but also to make sure that others understand your parting wishes.

In Singapore, the surviving spouse is usually entitled to one half while the other half is divided among the children. But if there is no Will, there are higher chances that no one would be held responsible to sort out the estates or to take care of the orphaned children. Without a Will, your assets may be distributed to people whom you do not intend to give anything to. Certainly, it is simpler, more responsible, and more convenient to consider making your own Will.

Clueless about the entire process? Start here:

DEFINITION

An individual makes a legal declaration or a Will to provide the administration and distribution of what he or she owns among his or her beneficiaries at death. The person who made the will is called the “testator” while the people who will inherit the assets are called “beneficiaries”. The Wills Act governs all the Wills in Singapore.

A WILL’S FORMALITIES

1. The testator must be at least 21 years old.

2. The testator must sign the Will accordingly. If he or she is unable to do so, a trusted person may sign in his or her presence.

3. Two or more witnesses are required and they must sign the will too, in the presence of the testator.

4. The two witnesses cannot be beneficiaries of the will (e.g., spouse of the testator) but the third witness can be a beneficiary.

MAKING A WILL IN SINGAPORE

Interestingly, you do not need a lawyer to make a Will!

A 21-year-old individual of sound mind can make his or her own Will and change it any time in the course of one’s life. But if you have insufficient legal knowledge on the subject, your “homemade Will” may be at risk of being ineffective or invalid. So, it is still best to seek legal advice. After writing one, you must keep a copy in a secured place and let your family members know of its existence.

Image Credits: pixabay.com (License: CC0 Public Domain)

To ease the process, you must approach the Wills Registry to deposit the document’s information. Expect a fee for it.