“My siblings are already fighting over my properties even though I’m still alive,” my uncle joked, acknowledging the numerous businesses and properties he owns. He stressed the importance of securing a competent lawyer to ensure his assets are distributed fairly.

You see, he plans to use his resources to establish a foundation dedicated to supporting vulnerable communities, particularly children who have been abandoned by their parents. This charitable endeavor holds a special place in his heart. He wants to ensure that his legacy will continue to help those in need even after he’s gone.

If he does not craft a Will in time, his estate will be divided according to Singapore’s intestacy laws. Having a Will will enable him to distribute his estate according to his wishes, after his death. It will allow him to give his money to the people he feels needs it most. Can you imagine how this vital document can change the lives of those around him?

Let us begin to understand what a Will is.

WHAT IS A WILL?

A Will is a legal declaration of how your assets will be distributed after your death. It prevents disagreements and provides clarity over your inheritance, which can be distributed to your loved ones or other charitable institutions after you pass away.

Apart from distribution of financial assets, a Will allows you to appoint your executors and your children’s guardians. You can approach a lawyer to help you draft a Will or use an online writing service. Feel free to change your Will anytime you see fit.

WHAT IS INSIDE A WILL?

Your Will should clearly state who is going to:

a. inherit your estate (i.e., include your beneficiary or beneficiaries),

b. take care of your children who are under 21,

c. carry out your wishes (i.e., your executor), and

d. dispose your assets if your beneficiaries pass away before you.

WHAT ARE THE BENEFITS OF ESTATE PLANNING?

1. As mentioned above, estate planning helps ensure that your assets are distributed according to your wishes after your death.

2. It specifies who will manage your affairs after you pass away to ensure that your matters are taken care of in a timely manner. Lasting Power of Attorney (LPA) allows someone to make decisions on your behalf in the event that you are unable to do so yourself.

3. It can help minimize taxes and legal fees.

4. Estate planning aids in ensuring that your business is smoothly transitioned to your heirs or successors.

CAN YOU PUT YOUR CPF IN THE WILL?

Central Provident Fund (CPF) savings are not covered under a Will and cannot be distributed via a Will.

You are strongly encouraged to make a CPF nomination so that your intended beneficiaries or charities can have quick access to the funds once unforeseen events happen. Moreover, completing your CPF nomination can help lessen administrative delays and avoid paying a fee to the Public Trustee’s Office for administering un-nominated CPF funds.

Not having a CPF nomination can result to your savings being distributed according to Singapore’s intestacy laws (or Islamic inheritance law).

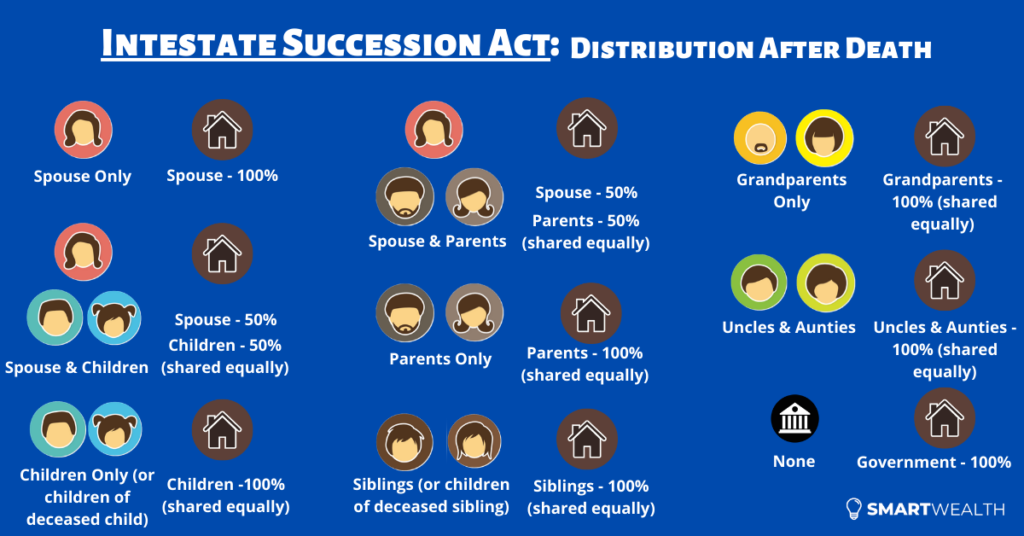

WHAT IF I HAVE NO WILL?

If you die without creating a Will in Singapore, your assets will be distributed according to Singapore’s intestacy laws or Islamic inheritance law. The Intestate Succession Act (ISA) will take effect. Distribution following the law may not be in accordance with your wishes or may not fit your family’s current financial situation.

Image Credits: unsplash.com

Having a Will enables you to distribute your assets on your own terms. Whether you want to provide for your elderly parents or your children, updating your estate plan regularly can ensure that it remains relevant and effective in light of changes in your personal circumstances and the law.

In Singapore, there’s always a constant strive to earn more money.

It’s perfectly understandable considering how high goods and services are priced, and how we want to provide a better future for our family.

Some of us take the next step by preserving our wealth and future income through the use of different types of insurance.

But only a few go even further to make it all fool-proof with estate planning.

What is estate planning all about? And what are some of the easy things we can do right now?

Let’s find out.

What Is Estate Planning?

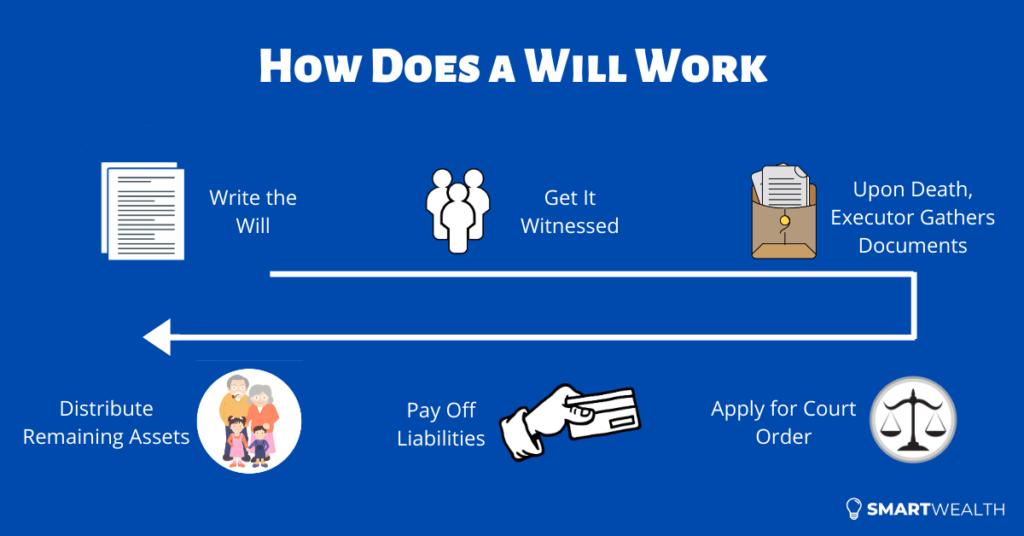

When death happens, all your eligible assets (e.g properties, money in the bank account, investments, insurance) will form your estate which will be distributed according to prior instructions (if any).

The purpose of estate planning (which can only be done before death) is to decide how your estate is going to be distributed upon the inevitable.

This distribution is indicated with the use of several legal documents.

All these ensure that the wealth you’ve accumulated thus far will go to the intended beneficiaries (people/entities who’ll be receiving your assets), in a timely and efficient manner.

Why Should You Care?

We tend to focus on wealth accumulation (savings and investments) and wealth preservation (insurance).

But a lot less on wealth distribution (estate planning), which is equally important in the grand scheme of things.

Firstly, the process of unlocking assets will be more tedious and complex. This inevitably prolongs the time for beneficiaries to receive proceeds. If the family depends on timely money coming in, this issue will be more dire. Who’s going to provide them with liquidity to pay off current bills and expenses?

Secondly, also because of the complex and lengthy process, it’ll cost more.

And lastly, most of the proceeds will go according to the intestate succession act or the Muslim law.

Therefore, your assets may not go to the intended people. And even if they do, not in the correct allocation that you wish for.

For example, if your spouse, children and parents are still living, your assets will be distributed to your spouse and children only, and none goes to your parents (even if they raised you up since young).

And it could also go to the unintended people.

For example, if your spouse and children are still living, and you think that your spouse doesn’t deserve anything, distribution will still go to your spouse.

These will cause ugly disputes amongst family members because there’s no clear and distinct indication of WHO should receive WHAT.

Furthermore, when you’re not around anymore, there’s no one else to turn to except for any legal documents you leave behind.

But when you employ even the simplest of estate planning tools, you effectively eliminate all these potential problems.

What are some of them?

3 Core Estate Planning Tools in Singapore

When dealing with financial matters, there’s always some resistance in taking action.

For example, people always want to find out what’s the best investment before investing, which is perfectly fine. But a problem that comes out from that is that too much information paralyses them and nothing is done in the end.

It’s also the same with estate planning.

But I can assure you that setting up these 3 tools will have the most impact and take the least amount of effort.

1) CPF Nomination

If you’re a Singapore Citizen or a Permanent Resident, you will have CPF accounts – Ordinary, Special, MediSave, Retirement.

If you don’t make a CPF nomination, and death happens, distribution of CPF savings will take a longer time, higher costs and goes by the law.

So you’d always want to get it done. It’s free anyway.

But most see it as a hassle because it used to be done via hardcopy forms (with 2 witnesses) or by going to the CPF service centres.

However, back in 2020, CPF allowed the nomination to be done online, and this made the application easy and convenient. While you still need 2 witnesses, the entire process is done electronically. If you want a step-by-step guide, you can check out how to make a CPF nomination online.

Even if a nomination is made, you can easily change it in the future. It’s usually done by submitting a new one, and that will override the existing nomination.

2) Insurance Policy Nomination

If you’ve bought life insurance and think nothing else needs to be done, think again.

The second part is to make a nomination where you can specify who will receive the proceeds and in what percentage.

Nominations can be made on life insurance policies with a death benefit. Take note that nominations can only be done on private individual policies and not on company/group insurance – they’re not owned by you.

There are 2 types of nominations: revocable and irrevocable (trust). Most choose the former as the nomination can be changed easily in the future.

Although it isn’t compulsory, it’ll be useful.

This is because by nominating, the insurance company can pay out directly to the beneficiaries when there’s an eligible claim. This effectively bypasses the usual probate process, saving time and money.

But here’s a trick question: do you want to nominate all your insurance policies?

The answer: it depends.

If your proceeds are large and all your policies are nominated, it’ll mean that your beneficiaries will receive the proceeds all at once.

Will they be able to handle such amounts?

There are many cases where the beneficiaries mishandle monies, and in the end, it got them into further trouble.

So if your proceeds aren’t that much (which you should have it reviewed), then it wouldn’t matter all too much.

But if it amounts to a bigger sum, you can make nominations on a few policies just for liquidity purposes. The rest can still be specified in a Will to pay out on a staggered or monthly basis.

To make a nomination, you can download the relevant forms from the insurance company, fill it out properly and sign in the presence of 2 witnesses. Or you can approach your financial consultant to help you with it.

3) Writing a Will

Even when you’ve done the CPF and insurance policy nominations, some assets will still be left out.

Examples:

Money in the bank account

Investments over several platforms

Properties (depending on the ownership type)

etc

If you don’t make a Will, all these will still be distributed according to the intestate law or the Muslim law.

Other than the usual benefits of writing a Will, you can also use it to appoint a guardian to take care of young children and create a testamentary trust to stagger payouts.

Just know that getting a professional to write a Will only costs a few hundred dollars.

The obvious advantage is convenience but more importantly, the Will is drafted to be able to stand in court if challenged.

Other Points to Take Note Of

Apart from the 3 basic tools mentioned above, there are other aspects you should know also.

Firstly, setting up trusts can give you greater control.

Although the Will covers most needs, the trust will bring estate planning to the highest level.

These benefits include:

can be created when you’re living

provide for a special needs child

utmost confidentiality

delaying gifts to beneficiaries

etc

While higher net-worth individuals derive more value from it, there are affordable trusts out there that can suit the needs of the masses.

Secondly, a distant cousin to estate planning is advance care planning.

Have you thought of what happens when you’re neither “dead” nor “alive”? In other words, mentally incapacitated.

You can’t do anything about your finances. And estate planning doesn’t kick in.

That’s when advance care planning comes in. It also involves different tools such as the Lasting Power of Attorney and the Advance Medical Directive.

These are important because it will specify what happens next when certain situations come up.

For example, when an Advance Medical Directive is done up, you specify that you don’t wish to be on life support to artificially prolong your life.

And for the last point, you need to have wealth.

You see, if you don’t have any wealth (your liabilities are higher than assets), there’s nothing to distribute even if you’ve done estate planning properly. Even if you’re mentally incapacitated, there may not be money to even pay for your medical expenses.

That’s why, financial planning (wealth accumulation and insurance protection), estate planning and advance care planning, all have a part to play in the bigger picture.

If one is missing, your financial plan is not wearing its full suit of armour. And when a battle comes, damages will be done.

What’s Next?

Estate planning is often in the back seat.

But at times, you have to bring it to the forefront.

That means either to set up the tools or to review them.

So take small steps by looking at the 3 basic ones first – CPF Nomination, Insurance Policy Nomination, and Writing a Will.

And then explore other areas when you’re ready.

About the Author:

Abram Lim runs SmartWealth which covers topics on personal finance – insurance, savings, investments, retirement planning, etc. It strives to produce research-backed articles so that readers can make better financial decisions with objectivity.

You live in a leasehold HDB flat, and you don’t possess millions of dollars in assets. By all accounts, you don’t really have much in terms of fortune—the type that is possessed by the crazy-rich scions of wealthy families and the kind that is romanticised in movies and TV shows. So why exactly should you have an estate plan when it looks like it’s going to be a walk in the park disposing of your assets anyway when the time finally comes for you to bite the dust?

There are several important benefits to having an estate plan in Singapore. In this short guide, we’ll quickly go through some of them.

Estate Planning Will Allow You to Dispose of Your Assets According to Your Wishes

The quick answer to the question of why estate planning is important is quite simple: it is a legal and effective method of making arrangements to manage your estate and financial affairs when you pass on. If you don’t have a will, a trust, or a lasting power of attorney, your assets will be distributed according to Singapore’s intestacy laws, supplanting your actual wishes on how you may have wanted them disposed of.

Imagine the amount of frustration and heartache your loved ones may have to go through when it is the state that gets to have the final say about what to do with the assets you leave behind. Designating your beneficiaries and appointing “attorneys” who can act on your behalf can save your family members the time, money, and aggravation while ensuring that your estate is distributed exactly in the manner that you desire.

An Estate Plan Takes Care of Your Dependents

We’ve already established that estate planning benefits not only the rich; it also benefits just about every other person of legal age in Singapore. However, it’s most especially advantageous to those with dependants, like children, elderly parents, or family members with disabilities.

This is the most important element of estate planning: designating your heirs no matter how much or how little you might have. You get to have a say what happens to your savings, investments, and real properties should something happen to you. You’re able to make sure that your loved ones are taken care of and that they will benefit from the wealth you’ve accumulated specifically for the purpose of providing for them in the first place.

Estate planning will also allow you to determine what happens to your CPF savings after your death. Because CPF savings—like the balances you might leave behind in your Ordinary, Medisave and Special or Retirement Accounts—are not considered part of your estate, it is important for you to make a CPF nomination. Otherwise, your CPF savings will be transferred to the Public Trustee’s Office (PTO), which will then distribute your assets to your family depending on how they see fit. This will be done according to the Intestate Succession Act Singapore citizens abide by.

Creating an Estate Plan Also Helps You Prepare for Your Own Needs

It’s true that an estate plan allows you to elect your heirs when you pass away, but did you know that estate planning can also help you prepare for your own needs in the event that you lose your mental capacity or become unable to make decisions for yourself?

Estate planning can help you appoint people you trust to act on your behalf through a legal document called a Lasting Power of Attorney (LPA). Doing so will allow you to safeguard your interests and give you peace of mind, knowing that your loved ones can make decisions for you should you ever lose your ability to make financial and legal decisions while you are still alive.

Take note that members of your family are not automatically given the right to legally act on your behalf, a fact that can hinder their ability to look after your needs. Only an LPA can make sure that they will be able to manage your estate legally and make arrangements for your everyday care.

Estate Planning Will Prevent Conflicts from Erupting within Your Family

What’s worse than dying and not having a say in whether or not the people you love will benefit from the estate you leave behind? It’s probably dying and having members of your family fight over your money and properties. It’s the kind of drama that you’ve probably seen somewhere on television before, one that can get really ugly and leave you rolling over in your grave.

Creating an estate plan allows you to preemptively terminate such conflicts. By designating who is legally responsible for your assets when you become mentally incapcitated, or by deciding how much each of your heirs will get when you pass away, there will be no room for strife to occur. You’ll also be able to prevent any relatives you might hate with a passion from even attempting to get a share of the pie, which is probably one of the most desireable benefits of protecting your assets with an estate plan.

Estate planning is not just the domain of the rich and the powerful in Singapore. Anyone with any amount of assets will benefit from the protection that a well-thought-out and well-executed estate plan brings. It can be a complex and challenging process, but it’s a necessary one that will make your family more ready to face the uncertainties of a future without you.

It’s a misconception in Singapore that it’s necessary to hire a lawyer to draft a will. Nothing could be further from the truth. Anybody can draft a will for you. In fact, if necessary, you can even write your own will, and it can be a perfectly valid will after you pass on.

While drafting wills does tend to lie within the domain of most estate-planning lawyers, many wills-drafting companies have also sprung up to service these needs. These companies usually don’t have any lawyers or even anyone legally trained but they survive by keeping themselves up to date on the existing law and marketing themselves heavily.

However, just because you can write your own will without having to spend a single cent doesn’t necessarily mean you should DIY. While it’s not impossible for the determined layman to pick up, there are a number of statutes and laws to get your head around if you want to make sure your will is drafted correctly.

You might want to take a look at this will-drafting guide if you’d like to draft your own will.

At the very least, you should be conversant with the Wills Act (Chapter 352) before embarking on writing your own will.

Advantages and Disadvantages of Drafting your own Will

Advantages

There’ll be zero costs as you’ll be drafting the will yourself. All you need is a pen (or more likely, a word processor).

There’s the added benefit of learning and picking up a new skillset.

Anytime you need to update your will, you won’t have to make an appointment with a lawyer or will-drafting company. You can just do it yourself.

Disadvantages

Exclusions will not be caught. It’s relatively easy to miss out on certain beneficiaries in a will. Someone who drafts your will, be it a lawyer or someone from a will-drafting company, will usually review your list of beneficiaries and ask you in-depth questions to make sure your will is an accurate representation of how you want your assets to be distributed in the event you pass on.

There’s a higher propensity for error. It’s more difficult for someone without legal training and experience in wills and probate law to be able to perfectly draft a will. There are numerous grey areas in the law that a layman might completely miss out on or misinterpret.

Advantages and Disadvantages of Paying someone to Draft your Will

Advantages

It’s relatively affordable to hire someone to draft a will for you nowadays. Simple wills tend to start from around $180. Complex wills can be more expensive but if you have a lot of assets in different countries, you probably won’t want to be drafting your own will as well.

Hiring someone to draft your will ensures peace of mind, particularly if you’ve hired a lawyer to write your will. There’ll be less chance that a beneficiary will contest probate in the event of your passing and you’ll feel more assured that there won’t be errors in the will.

Most estate-planning lawyers in Singapore can advise you on the whole estate-planning process, as opposed to merely the drafting of the will. Your lawyer can also assist you with getting a Lasting Power of Attorney and help your executors with extracting the Grant of Probate upon your passing.

Disadvantages

You’ll have to incur costs to get peace of mind. While the price of having a will drafted is relatively cheap, you do still have to pay for it.

Conclusion:

There’s no real right or wrong answer here. If you’re willing to spend the time and effort to learn the relevant laws and statutes surrounding wills, it can be a fruitful exercise to write your own will.

However, if you’re not willing (or unable) to spend the time to pick up will-drafting, it’s probably in your best interest to go to a professional will drafter, preferably a lawyer. The last thing anyone needs is a will riddled with errors. A DIY will that’s poorly drafted can save you money in the short term but create a mess for your heirs when you’re gone.

Author Profile:

Shen is a writer for Singapore Probate, a website where Singaporeans can learn more about estate-planning matters in Singapore.

While there has been an increase in the number of younger people making wills in Singapore [1], there still seems to be a lingering taboo over the creation of something Singaporeans perceive to be morbid.

Unfortunately, as the saying goes, nothing is sure in life except death and taxes, and we all need to realize this fact and plan ahead for the future.

Generally, it tends to be a good idea for anyone to create a will. However, it’s even more important in certain situations, such as when you’re married with children, a single parent or blessed with multiple valuable assets.

So without further ado, here are 5 reasons why you should create your Singapore will.

1) To determine who receives your assets.

Generally, if you’re a Non-muslim in Singapore, and wish to distribute your estate in accordance with your wishes, you will have to create a will. If you don’t do so, your estate will be distributed according to the Intestate Succession Act, and this may unfortunately go against your true wishes.

You may have preferences as to where you wish your funeral to be held, the type of casket and picture you wish to be used, whether you wish to be buried in Choa Chu Kang or cremated, and how you wish for these expenses to be covered. Providing for this in your will can help save your family additional stress from trying to figure out what your preferences would be.

Altruism is another reason to draft a will in Singapore. You may be passionate about certain causes and wish to set aside a portion of your wealth for charitable organizations you wish to support. This is a fantastic way to give back to the community and to ensure a portion of your funds is used for a good cause.

Author Profile:

Shen is a writer for Singapore Probate, a website where Singaporeans can learn more about estate-planning matters in Singapore.