Making New Year’s Resolution is synonymous to crafting a new budget plan. Creating these two signifies an act of self-improvement. However, no plan is entirely foolproof!

These are just some of the reasons why I previously failed at budgeting:

I FOCUSED HEAVILY ON THE PRICE

Before purchasing a new laptop for work, I inspected some of the contenders from the well-known brands. My new laptop must not only fit my physical preferences, but also my financial limit of up to S$1,000. I searched vigilantly through the store and found a 14-inch HP laptop as well as a 14-inch Dell laptop. These two devices have the same processors and operating system. However, the main memory of the former is 8GB and the latter is 4GB. An important fact is that only the Dell laptop was within my budget.

Which one did I chose? The one with better specifications. Although it retailed for S$1,099, I still taught that it was a smarter investment.

According to a 2012 study published in the pages of the “Journal of Marketing Research”, people fail to follow their budget because they are more likely to spend more than they planned. You must not always beam too much focus on the price. Instead, compare the value (e.g., which has laptop optimal screen size and RAM) of what you are getting before committing to a sale.

MY BUDGET WAS TOO STRICT

Upon getting my first full-time job, I started to restrict myself. My goal was to make enough money to save up for my graduate studies and to help my parents in the household expenses. I did so. I gave about 10% of my salary to my parents and 50% would go to my savings account. I removed my trips to the spa and the cinema. A hefty savings greeted me at the end of every month. But, I felt burnout as there was no room for pleasure. This is when my budget failed me.

To turn things around, I started to make money on the side. I became a blogger that solicits money for endorsements. Eliminating unnecessary expenses is a good idea, but you must reward yourself (from time to time).

I FELT EXHAUSTED WHILE TRACKING MY SPENDING

You need discipline to track your own spending. I realized this firsthand. I used to compile all my receipts and banks statements. But, it got too exhausting! I started with a willpower to succeed until the constant vigilance took a toll on me.

A study supports my statement as it was found that self-control and intelligent decision making involves one’s energy supply. Once this energy runs out, you are more likely to go on a spree.

Image Credits: pixabay.com

Get things by following thru your plan. Practice is the key! Improved decision making and control will become second nature to you as time passes.

In its fundamental form, insurance is a contract that enables individuals or entities to receive financial protection against losses. It ensures the stability of families and businesses after a crisis or other unfortunate events. Simply put, insurance grants policyholders a peace of mind. Isn’t that what everybody wants – to be able to sleep at night without having to worry about what the future holds?

These are the reasons why I am drawn to getting insurance policies. I have to be completely honest. One of the major drawbacks that I dislike about insurance is its complexity. I am apprehensive about the piles of questions and bulky documents. Do not get me started about the confusing technical terms!

To my delight, I was introduced to a revolutionary insurance company that dances gracefully with the modern tides. This was none other than FWD Insurance. FWD Insurance aims to transform the way that Singaporeans experience insurance by simplifying the purchase and claims process. It helps you to skip the agent by directly working with them online.

Say goodbye to nerve-wracking call backs and time-consuming interrogations by embracing their user-friendly website!

FWD Insurance understands how valuable a working Singaporean’s time and money is. This is why the company maximizes these two commodities through providing insurance quotations under 60 seconds for car insurance and 10 seconds for travel insurance. These impressive figures are due to the fact that FWD only asks questions that are absolutely necessary.

For instance, it took me 25 seconds to be quoted with the premium of about S$174 for a DIRECT-Term Life insurance that seeks to cover 5 years of my life. I used the rest of my day to focus on other productive matters. You can do the same thing too!

The people behind FWD best explained the company’s concept: “We believe that insurance doesn’t need to be complex, sold through middlemen, or take up vast amounts of your time.” It offers competitive prices and easy-to-understand insurance.

Attractive Insurance Products

It is usual for people to feel skeptical when they encounter an insurance company for the first time. Wash away this feeling by knowing that you are supported by a company with a strong financial record. FWD is the insurance business arm of the established investment group, Pacific Century Group (PCG).

Choose from the four secure insurance products such as DIRECT-Term Life Insurance. Car, Travel and Personal Accident.

A. DIRECT-TERM LIFE INSURANCE

The DIRECT-Term Life insurance ensures that your family’s financial future is secured despite unfortunate events such as becoming diagnosed with a critical illness, becoming permanently disabled, or passing away.

These are the primary reasons why I am drawn to this policy:

I can choose the period that works for my budget and lifestyle (e.g., 5 or 20 years).

I can purchase coverage through my smartphone – without going through a middleman.

Because FWD does not pay commission to agents, my coverage of up to S$400,000 may cost less than S$1/day.

B. CAR INSURANCE

Three comprehensive plans cover vehicle repairs, third-party damages, medical expenses, and roadside assistance. These plans were crafted to suit your personal needs and budgets.

No matter what plan you avail, your repairs will be completed by the FWD workshops. You can cruise along blissfully until your car turns ten. Furthermore, your 50% NCD is guaranteed for lifetime. NCD stands for no-claim discount. Drivers who have earned their 50% NCD get to keep it for life because they believe that one accident doesn’t make you a bad driver.

On top of that, you can add amazing features which gives you coverage when you are driving in West Malaysia and certain parts of Thailand.

C. TRAVEL INSURANCE

Take for instance; to reap the rewards of her hard work, Jena scheduled a weeklong vacation to Thailand. The beautiful country has so much to offer from pristine beaches to established sports clubs. She did not forget to pack her favorite S$200 golf putter. To enjoy a fuss-free tropical getaway, she purchased FWD’s travel insurance. It was one of the best decisions she ever made as the putter got lost in the airport and fortunately, sports equipment is covered by the policy.

Aside from sports equipment, the travel insurance also includes unlimited medical evacuation. You read that right! The last thing on your mind is how much your emergency evacuation will cost. This is why FWD has thought of this for you.

You can expect the claiming process to be a breeze too. Claim with a few clicks with the “Click to Claim” feature. This means, all you have to do is snap your boarding pass and claim for flight delays via WhatsApp. This feature is available for baggage delays too. Simply take a photo of your baggage slip and send it to FWD via WhatsApp. That is convenience at its finest!

D. PERSONAL ACCIDENT INSURANCE

Personal Accident (PA) insurance provides compensation in the event of disability, injuries or death. In fact, one feature unique to FWD is that the policy also covers the most number of infectious diseases including Zika and dengue fever. Under this policy is the Guardian Angel Benefit. If both parents pass away or become permanently disabled due to an accident, FWD will provide up to S$500,000 for the surviving children.

Lastly, natural circumstances now cannot stop you from having fun as ticketed event cancellations due to haze are covered. Apparently, they are the only insurer in Singapore to offer this.

Irresistible Features and Highlights

Before you make a commitment, it is important to know what this new insurer can do. Let me start by stating the fact that there are no middlemen or agents. Since you do not have to pay for commissions, you can save more money.

FWD allows you to complete your purchases online. It is so quick and easy to complete the online quotation that even your 9-year old niece can do it for you! As soon as you make your purchase, you will get an email with the policy. You will also receive an SMS that notifies you to check your email.

Lastly, the policies are delivered with no technical terms. You will know exactly what you will get explained in plain English.

From now till 31 January 2017, you can now enjoy a 10% discount on all FWD insurance products with this promo code – FWDHi10.

For the people behind FWD, customers are at the heart of the entire process. They let you experience exceptional insurance by minimizing your effort and making products readily accessible. May they change the way you feel about insurance!

Some Chinese parents that are steeped in Confucian values often see their children as the main source of retirement funds. This can be a stressful burden to carry, especially if you are a young adult struggling with multiple financial commitments. Therefore, I have devoted a considerable amount of time learning how to grow my parents’ retirement funds and minimise household expenses. So here are 4 ways that your parents can also grow their retirement savings.

Minimise Expenses Via Various Senior Citizen Perks

Image Credit: NTUC FairPrice

For a start, I examined how my parents can reduce their household expenditure. For instance, I recently learnt that NTUC FairPrice offers 3% discount to Pioneer Generation members every Monday. If your parents are not Pioneer Generation members, fret not as those over 60 years old enjoy a 2% discount every Tuesday as well. Similarly, if your parents are over 60 years old, they can also apply for senior citizen concession travel cards. This will entitle them to significant discounts on public transport compared to a usual adult fare card. These are all schemes that my mother can tap on from next year onwards.

For Singaporeans aged over 65, do not overlook the outstanding benefits that come with the Pioneer Generation Package. Amongst the various benefits, it provides subsidised medical and dental services at CHAS participating clinics. These subsidies should help to alleviate healthcare costs. If your parents are not aware of these schemes, you may like to inform and even assist them in the application of these concession cards. A little savings here and there will ultimately add up and go a long way to reduce the household’s daily expenses.

Grow Their Retirement Funds By Leaving Monies in their CPF Accounts

Ask any Singaporean or Permanent Resident and they will tell you that age 55 is a significant milestone in their lives. It is not so much about celebrating yet another year in their lives, but rather, it marks the day where they can dip their hands into the pot of gold that they have painstakingly built up during their working years. Yes, I am referring to the CPF. At age 55, CPF members can withdraw:

up to $5,000, or any balance in their Ordinary and Special Account savings above the Full Retirement Sum[1] (‘FRS’), whichever is higher; and

any Retirement Account savings (excludes any top-up monies, government grants, and interest earned) above the Basic Retirement Sum (‘BRS’) if accompanied by a sufficient property charge or For more information, please refer to CPF’s website.

The temptation is indeed great, but do pause for a second and have your parents assess whether they truly need the money at that juncture.

If your parents are over age 55, choosing to leave their monies in CPF ensures that:

They enjoy an additional 1% interest on the first $30,000 in their combined CPF balances. This is on top of the prevailing Retirement Account interest rate of 4% and the additional 1% interest on the first $60,000 of combined CPF balances applicable to all CPF members. This easily beats any existing interest rate offered by commercial banks. Moreover, the principal and interest are guaranteed by the government, a rock solid triple AAA rated institution.

Even if they do not withdraw any amount at 55 years old, they can still do so anytime later. Therefore, there is no hurry to decide on the withdrawal of excess funds.

Furthermore, your parents also have the option to start their CPF LIFE payouts later, up to age 70[2]. For each year deferred, their CPF LIFE monthly payouts may increase up to 7%,guaranteeing them a larger monthly payout thereafter. Therefore, if your parents are gainfully employed at that juncture, it may be a superior proposition to leave their monies with the CPF.

A good example would be my father- in-law. He turned 55 recently but chose not to withdraw the excess sum after setting aside the FRS. He realised that he would earn an interest rate that is higher than if he were to leave the excess sum under the fixed deposit schemes offered by commercial banks. This is a very prudent decision that will add to his retirement funds.

Grow Their Retirement Funds With Silver Housing Bonus

Some retiring parents face the problem of being cash-poor but asset-rich. They have insufficient retirement funds but may own a property that has appreciated substantially in capital value. The government has introduced the Silver Housing Bonus to incentivise this group of people to unlock the value of their property and to ensure members have a lifelong income. It was introduced to help lower-income elderly households supplement their retirement funds when they “right-size” their flats. Eligible households can receive up to $20,000 cash bonus when the net sales proceeds are used to top up the CPF Retirement Account.

This policy is an attractive option for parents whose children have all left the nest and gone on to set up their respective homes. The need for a big house no longer exists. Therefore, it may be a practical option to downgrade to a smaller house in order to receive the $20,000 cash bonus from Silver Housing Bonus, as well as save on utilities, maintenance and conservancy fees at the same time.

For those who are not keen to “right-size” their flats out of sentimental value, there is another way to unlock the value of their property. By participating in the Lease Buyback Scheme, your parents can receive a stream of income to add to their retirement funds while continuing to stay in the property.

Claim Tax Relief Via The Retirement Sum Topping-Up Scheme (‘RSTU’)

For young adults who have been giving their parents a monthly cash stipend, do consider utilising the CPF Retirement Sum Topping-Up Scheme (‘RSTU’) instead. That is because you may be eligible to receive tax relief and reduce your income tax expense. Do note that the amount of tax relief that you enjoy is the amount of cash that you have contributed to your parents’ Special Accounts or Retirement Accounts (for parents above 55 year old), capped at S$7,000 per annum. This tax relief is applicable only if your recipient’s Retirement Account has not exceeded the current FRS. Cash top-ups beyond the current Full Retirement Sum will not be eligible for tax relief.

Therefore, by depositing cash into your parents’ CPF accounts via the RSTU, you fulfill your duty as a filial child and also receive tax relief! That is killing 2 birds with one stone.

In all honesty, I confess that this is a difficult suggestion to broach. Most parents of that generation still prefer to see cold hard cash as part of their retirement funds. To bridge this gap, you may try to argue that:

If they have no urgent need for the monthly stipend that you are giving, contributing directly into their CPF accounts earns higher interest rates than what commercial banks give.

They can still withdraw up to S$5,000 from their CPF accounts from age 55.

They will be getting higher lifelong monthly income once they start their CPF LIFE payouts.

While the aforementioned all appear to be very objective advantages, my parents remain unconvinced till this day. That is because emotions often play a stronger role in their perspectives of money. For instance, my father sleeps more soundly if his pillow, rather than his CPF, is padded with his retirement funds. But I will continue to nag and hopefully my parents will switch sides one day. Talk about role reversal!

Conclusion

Despite the various ways to grow the retirement funds and minimise household expenses, you may have come to notice that my family and my wife’s family are at different ends of the spectrum. My father-in-law uses his financial literacy to take advantage of the various schemes available in CPF to grow the household’s retirement funds. On the other hand, I am doing my utmost to help my parents play “catch-up” in terms of retirement readiness. But as they say, better late than never.

Singaporeans are fixated with buying property – and they don’t just stop at one.

In a report published in June 2016, Maybank Kim Eng’s research team found that approximately 1.1 million households in Singapore own the homes they occupy, but there are another 200,000 housing units are currently held as investments. This demand, coupled with land scarcity, means that property in Singapore doesn’t come cheap.

There is however, a more affordable option for those looking to invest in property: real estate investment trusts (REITs). REITs – Singapore REITs (S-REITs) in particular – have been making headlines recently for offering handsome dividends, made even more attractive by a persistent low interest rate environment. If you are a dividend investor, you may want to learn more about this asset class.

How Have Singapore REITs Fared?

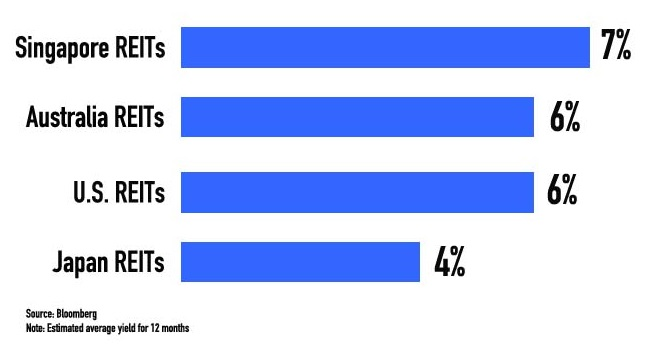

According to a Bloomberg report in October 2016, the 7% yield offered by S-REITs exceeded those listed in Australia, the US and Japan. That’s been the driving force behind an approximately 9% increase in the FTSE Straits Times Real Estate Investment Trust index this year as yield-hungry investors flock to the offerings amid record-low interest rates.

Findings by SGX My Gateway published on 11 September 2016 also showed that the sector logged an indicative average dividend yield of 6.7% p.a. thus far, compared to that of the Straits Times Index (3.9% p.a.) and MSCI World REIT Index (3.9%p.a.).

Compared to fixed deposit rates? The difference is even wider. In September 2016, the 12-month fixed deposit rate – or the average rate compiled from that quoted by 10 leading banks and finance companies – was 0.35% p.a.

What is a REIT Anyway?

A REIT is a trust that owns and operates income generating real estate. The rental income or interest payment that is earned by the REIT is passed on to investors in the form of dividends.

Here are more facts about REITs and S-REITs:

There’s a reason why S-REITs pay handsome dividends. They are required to distribute at least 90% of their taxable income each year in order to enjoy tax exempt status by IRAS, subject to certain conditions.

Investing in one REIT gives you exposure to not just one, but a portfolio of properties, and at a fraction of the price that it would cost you to buy a single property.

The portfolio of properties are not limited to those in Singapore. Some REITs have international properties in their portfolio.

REITs are more liquid compared to property as they can be bought and sold on stock exchanges throughout the day just like any other stock.

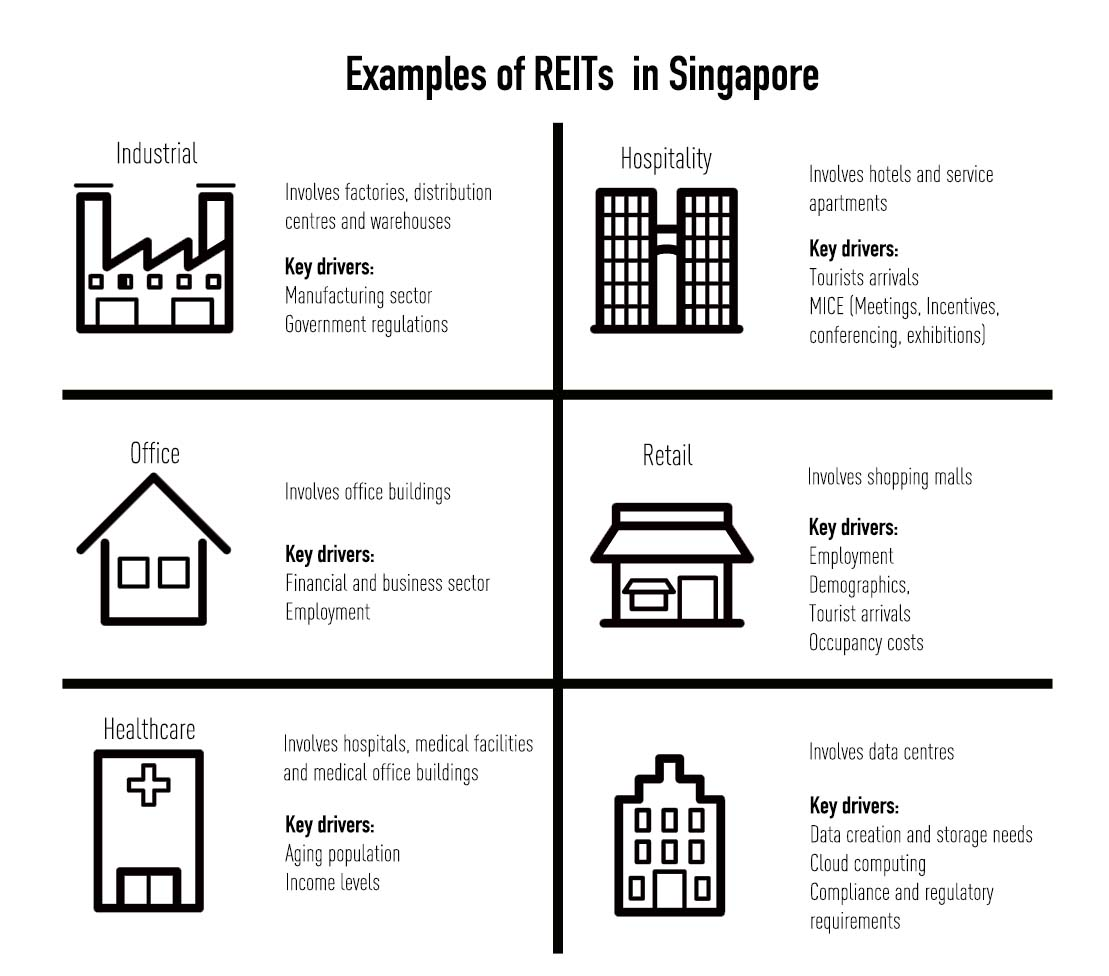

What S-REITs are Out There?

There are different types of S-REITs to choose from, and they are affected by different factors.

Maybank Kim Eng’s research team believes that industrial REITs, like Ascendas REIT and Mapletree Industrial Trust, could benefit from public spending’s focus on boosting innovation and productivity. Business parks, science parks and high-spec industrial space will be in demand. So if you are wondering what type of REITs to watch out for, you could consider finding out more about industrial REITs and whether they fit the objectives of your portfolio.

Disclaimer: This message is for general knowledge or information only. It is not an offer or invitation to buy or sell securities, futures or other products or services. Our products or services vary in different jurisdictions, subject to their respective terms and conditions and the licences our affiliates and us hold. This message is not an advice or recommendation for any financial planning, investment, legal, tax or other purposes and, accordingly, no responsibility or liability is assumed by us or our affiliates, whether directly or indirectly, from any person taking or not taking action

There is a new trend circulating the insurance market. This trend is none other than women’s insurance. Have you heard of this?

I cannot deny the fact that women are more prone to certain diseases due to the workings of the female body. Health issues such as pregnancy complications and ovarian cysts are peculiar to women. Some of these health conditions are not covered by life or health insurance due to its exclusivity. This is why women face encouragement to add special riders. But, this scenario is a thing of the past! More and more insurers are offering women-centered maternity and critical illness plans.

Parents who are experiencing the miracle of childbirth for the first time can be overtly “kancheong” (tensed). Who can blame them? Maternity is a vulnerable period that you must not take lightly. To safeguard yourself and your child, you may purchase maternity insurance policies. Some of them are in the form of bundled plans to cover the child’s needs beyond the early stages. Consider signing up for the “PINKLIFE” by Great Eastern Life Assurance.

PINKLIFE covers allows the policyholder to feel safe while she is pregnant. Women (between ages 17 to 40) have the option to upgrade their plans to include coverage for pregnancy-related conditions such as stillbirth or miscarriage due to accident. The newborn will also be covered for premature birth requiring ICU care and congenital conditions (e.g., Down’s Syndrome). This plan stands out from the rest because is protects the policyholder from 37 critical illnesses too.

Image Credits: pixabay.com

Aside from maternity bundled plans, insurance policies for women occur as critical illness insurance. Critical illness (CI) insurance usually pay a lump sum when an individual is diagnosed with a disease covered in the terms. It is important to note that most policies depend heavily on the policyholder’s age. Insurers will charge you with a higher premium if you belong to an older age group. This is because the risk to certain diseases increase as age does. So, examine the point of coverage. Is their an age allowance? How about a “stage” allowance (e.g., the coverage takes place only at the early stages of breast cancer)?

As this CI policy is targeted at women, you can commonly find that some of them offer free health checkups such as mammogram. Speaking of free health checkups – I introduce you to the AIA Glow of Life. It is a CI that is especially made for women. You may enjoy a complimentary medical checkup every two years starting from your 3rd year with the policy. It gives you payouts for a wide range of illnesses including breast cancer, osteoporosis, and rheumatoid arthritis.

What’s more? Policyholders can expect to gain from a 100% reimbursement for a reconstructive surgery due to an accident.

While some insurers offer standalone women-centered plans, others do not. Please make sure to read the fine print to understand what you are covered for! Feel free to contact a financial adviser for an appropriate consultation.